- Cannabis industry software provider Akerna has a history of producing glitch-plagued, poor quality software.

- Government documents reveal a reduction and probable cancellation of Akerna’s Washington contract, one of only three the company currently has, casting management guidance into doubt.

- After a run of acquisitions combined with Akerna’s unprofitable underlying business, the company is quickly depleting its cash necessitating a raise in the near term.

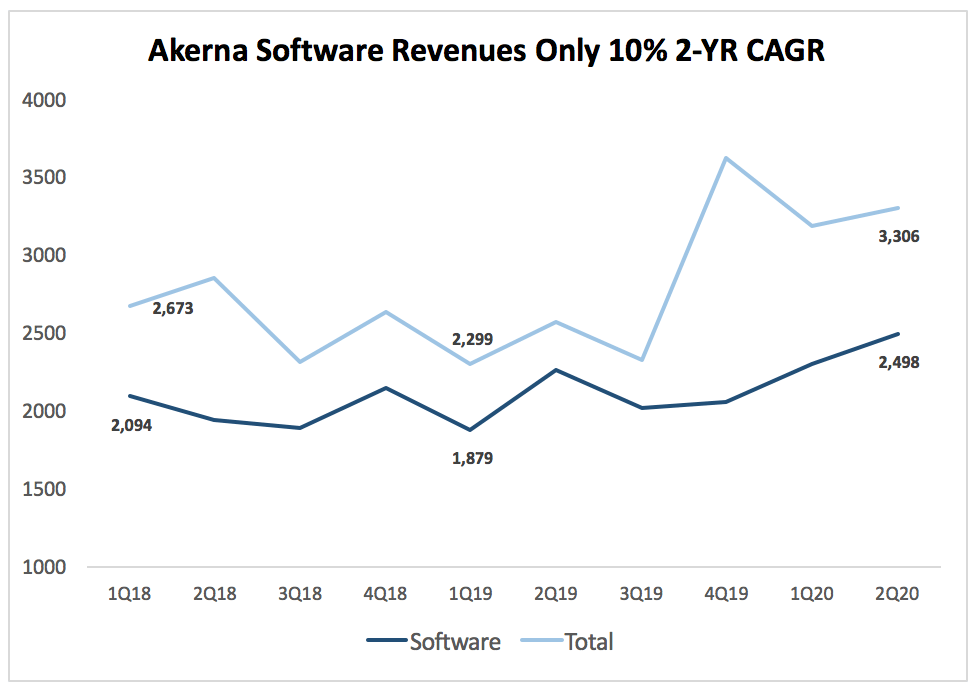

- KERN is trading at 5-times expected CY 2020 sales but software revenues – Akerna’s growth driver – have grown only at ~10% CAGR since 2017.

- We believe KERN is overvalued and vulnerable to a sharp sell-off given the headline risk.

Background

Akerna Corp (NASDAQ: KERN) is a cannabis industry software provider operating in three main areas: government regulatory software, commercial software and consulting services. The government product, known as Leaf Data Systems (39% of FY19 revenues), enables state regulators to ensure cannabis vendor supply chain compliance. Akerna competes for state contracts, and any wins naturally encourage state commercial vendors to use KERN’s inventory tracking software, thus enabling the company to “upsell” its enterprise resource planning (ERP) software known as MJ Platform (37% of FY19 sales). As such, Akerna’s business is highly reliant on these government contracts. Three companies have signed exclusive contracts with twenty-six states for these “seed-to-sale” tracing systems: Tiger Global-backed Franwell’s Metrc (13 states), Helix TCS’ BioTrackTHC (10), and Akerna’s MJ Freeway (3). Arcview Market Research estimates US cannabis businesses will spend $521m on software and IT services in 2020.

Undisclosed Probable Contract Cancellation

Akerna currently has active contracts with regulators in only three states – Pennsylvania, Washington and Utah. A document from the Washington State Liquor and Cannabis Board indicates that after years of delays and quality issues, the state could be ready to end its relationship with Akerna and find a new software provider. The internal Jan 8th, 2020 memo from the Office of the Washington State Chief Information Officer disclosed that Akerna’s Washington State contract scope was reduced last month to prevent it from improving, after 6 months of effort, critically flawed software from a repeatedly corrupted July 2019 software update. Akerna will pay a non-accrued for, nor disclosed, $267K penalty due to repeated timeline and operational failures. The memo hints that the state will soon begin the process of switching software providers:

“As it operates today, the system has only been partially implemented with known defects that are being addressed via workarounds. At this point, the vendor, licensees, stakeholders and WSLCB are all in agreement that the risk of further disruptions to the market caused by the software outweigh any potential benefit. “

An industry insider we spoke with expects an RFP for a replacement vendor will be issued in the March/April timeframe and that this was “single worst software vendor I’ve seen in 30 years in software”.

Akerna has a history of producing glitch-prone software – Nevada cancelled its contract with MJ Freeway in 2017 due system crashes and security breaches. Soon after the software was implemented in Washington regulators experienced problems with Leaf Data, and Akerna repeatedly failed to remedy the issues. These recurrent problems disrupted sales, frustrating commercial licensees (high numbers of customer complaints can be found in media reports, we’ve aggregated samples here). The exasperation of the regulators is evident in the document:

“From the beginning, the project struggled with vendor management, scope management, quality management, stakeholder management and organizational change management. WSLCB developed several iterations of mitigations and remediations of project issues. While those areas under control of WSLCB made steady progress, the project was not able to overcome release quality issues, which was the responsibility of the vendor.”

The Washington contract was ~10% of KERN’s FY19 revenues. However, this doesn’t account for the state’s commercial vendors who were compelled to purchase MJ Platform and Akerna’s consulting services. The commercial and consulting businesses generated 37% and 22% of FY19 revenues respectively. And while Akerna doesn’t provide state level detail for the MJ Platform or consulting businesses, given that only three states use Leaf Data, Akerna’s commercial business in Washington is likely significant. If we conservatively assume that Washington accounts for 5-10% of commercial sales, the state could account for > 15% of total revenues.

Washington would be the second contract cancellation out of four state wins. Akerna has already been facing competitive pressure in Washington from Dauntless, which apparently handles 30-40% of Washington’s retail pot transactions.

Akerna’s Largest Contract Likely Also At Risk

Akerna won a $10.4m Pennsylvania seed-to-sale contract in mid-2017 (we estimate 30% of FY19 sales). Leaf Data software has had similar problems to those seen in Nevada and Washington, crashing in October 2017, August 2018 and September 2019 resulting in significant downtime for businesses and patients.

“The chronically glitchy computer system that forms the backbone of Pennsylvania’s medical marijuana program crashed Thursday morning, causing several dispensaries to halt sales and turn away patients.”

“Medical marijuana patients across the state couldn’t buy medicines Tuesday due to an update in a tracking software system that’s supposed to track sales, not prevent them.”

The initial term for the Pennsylvania agreement is for five years beginning in April 2017. However, the state can terminate the contract at any time with only a 30 day advance notice. The contract gives Akerna exclusivity in the commercial market, requiring commercial operators to use Akerna’s ERP offering. Given the numerous issues in Pennsylvania and the complaints from vendors, it wouldn’t be surprising if the state sought a different provider.

Recent Utah Contract Won by Severely Underbidding

With its history of quality issues, Akerna appears to win contracts mainly by underbidding competitors, creating legitimate concerns around its ability to achieve profitability. According to the Philadelphia Inquirer, Akerna won the Pennsylvania contract solely on price:

“MJ Freeway was awarded the $10.4 million contract, though it scored lower on technical merits than its rivals. Despite at least two “catastrophic hacks,” data breaches, and other glitches, MJ Freeway won because it undercut the competition by several million dollars, bid documents show.”

In August 2018, Akerna announced it had won a $1.3m Leaf Data contract with Utah. The Salt Lake Tribune wrote:

“Utah is preparing to strike a deal with a Denver-based software company to build the digital backbone of the state’s emerging medical cannabis program, despite the business’ problems with outages, crashes and hacks in other states… The vendor, MJ Freeway, rose to the top largely by lowballing the competition — offering its services for less than half the price of the other finalist for Utah’s five-year contract…But the two states that have active contracts with MJ Freeway haven’t had an easy time of it.”

Akerna won the 5-year Utah contract by offering 27% the quoted $5m estimated value and less than half of competitor BioTrackTHC’s $3.5m asking price. An insider at competitor BioTrackTHC told us it will be nearly impossible for KERN to generate profit on this contract and given the disparity in bids, and we believe him. The company was likely forced to bid at a massive discount to competition due to a steady stream of negative press from the software failures in Nevada, Washington and Pennsylvania.

Near Term Capital Raise

Akerna acquired Canadian Cannabis ERP provider Ample Organics in December 2019 for $45m ($5.7m in upfront cash, $32.3m in KERN shares plus $7.6m in additional shares contingent on revenue targets). The price is a 5.2x multiple on CY20e sales of $8.7m. Interestingly, Ample Organics had laid off 16% of its workforce last summer, with the CEO noting weakness in the Canadian cannabis industry:

“There’s a lot … of turmoil happening. I think that capital is drying up in the space, and really Ample is a bellwether for everything else that’s going on in the industry”.

While Akerna is guiding towards Ample being cash flow positive in 2Q20, given the industry-wide issues highlighted by Ample’s CEO, it wouldn’t be surprising if the unit fell short of its revenue and profitability targets. The risk associated with Ample’s performance is amplified since Akerna is spending ~30% of its cash on the acquisition.

After the close of the Ample purchase and assuming a steady rate of burn of $3m a quarter, Akerna will only have around $10m in cash by end 1Q20. But this doesn’t account for the $2.4m Akerna committed to invest in solo sciences which it acquired in the fourth quarter. The deal terms specify that Akerna will contribute at least $250K per month to fund solo. Thus, Akerna may have less than two quarters of working capital by the end of March. Also note that in the 10-Q for the September quarter, Akerna stated it had signed three letters of intent for acquisitions. After the deals for solo sciences and Ample, this leaves one more acquisition in the near term. The 10-Q for the December quarter notes management believes it has enough cash to fund the business for the next year, but after the latest acquisitions, the commitment to solo sciences and another quarter of burn, we’d expect a going concern notification in the next quarterly report. In our opinion this means a CY20 raise is very likely.

Valuation Appears High Given Level of Organic Growth

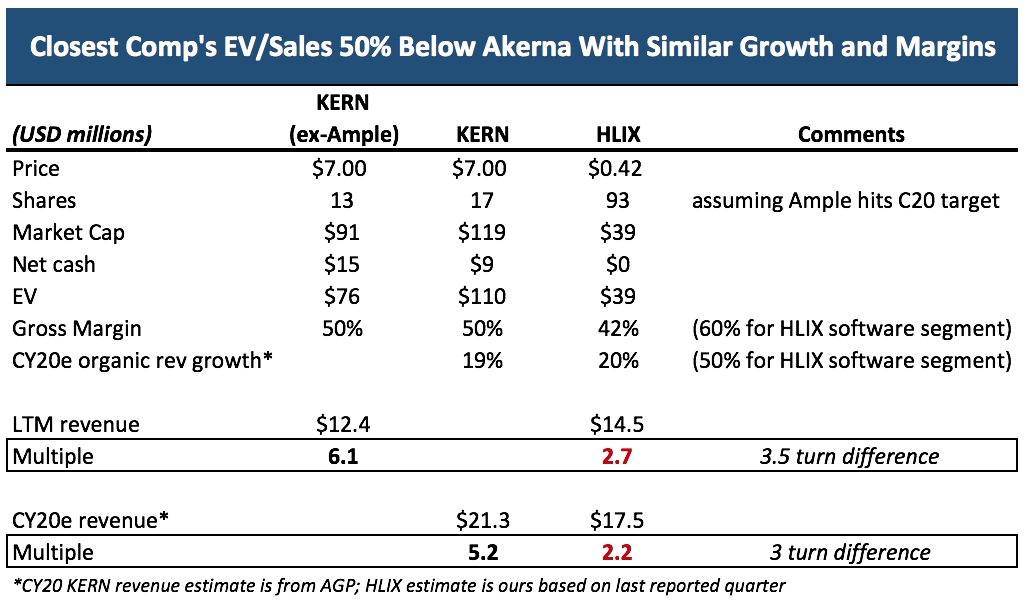

At a stock price of $7, Akerna is trading at 6x EV/LTM sales and 5x C2020 consensus sales. Publicly traded comparables are difficult to find, but HELIX TCS (OTC: OTCQB:HLIX) which acquired Akerna’s direct competitor BioTrackTHC in 2018 appears to be the closest. Helix has two segments: software and physical security/guarding which account for roughly 65% and 35% of revenues respectively. Growth in the lower margin legacy security business is flat, while the higher margin software business grew over 50% y-o-y in 2019. Helix is trading at ~3x EV/LTM sales, has slightly lower blended gross margins than Akerna, but a larger compliance software footprint with 10 state governments using BioTrackTHC seed-to-sale software and potentially similar or higher organic growth (HLIX hasn’t provided revenue guidance yet but revenues have been growing ~20%).

As of December, Akerna is guiding $27.5m in CY20 sales of which $8.7m is Ample Organics. So management is targeting $18.8m ex-Ample which implies ~50% organic growth. This seems rather aggressive as software revenues – Akerna’s stated growth driver – have only grown at ~10% CAGR since 2017.

Source: Company Financials

On February 12, Akerna reported earnings for the December quarter. Overall revenues, helped by a 202% y-o-y increase in the lower margin consulting business, were in-line with expectations. However, a jump in expenses caused a larger than expected loss and stagnant bookings disappointed investors. The analyst at Alliance Global Partners (AGP), the only sell-side firm publishing research on KERN, expressed his concern on the call:

“The bookings on an annualized basis is about $400,000, just taking the number you gave times 12. And that’s similar to last quarter, and I think, excluding Ample Organics, I think you’ve discussed MJ Platforms would — you thought would grow significantly, I believe, in the March quarter than even more in the June quarter. Is it still reasonable to assume that March quarter will be much stronger than December, given the bookings were similar? And this last quarter, we didn’t see quite a pop in MJ Platform sequentially?

Due to the slower growth in software, AGP took their CY20 revenue target down 22%, from $27m to $21.3m which implies only 19% organic revenue growth ex-Ample. HLIX has a similar growth rate (and higher in software) yet its stock is trading at a revenue multiple less than half of KERN’s.

Source: Company financials

AGP assumes KERN will be cash flow positive in 2022 and that the company has enough cash to get there. However, we believe AGP is underestimating Akerna’s cash needs and the probability of a cash raise in 2020. Using AGP’s own estimated CY20 quarterly loss figures (totaling $12.7m), and allowing for some non-cash expenses, Akerna will have negative working capital by Q420. And all of this highlights how crucial it is that Ample Organics meets its 2020 guidance. Any disappointment from Ample will further stress an already thin balance sheet, opening up scenarios with significantly more downside.

Avoid Shares or Establish Short

We have outlined two highly probably near-term risks: Washington contract cancellation representing ~15% FY19 sales (likely correlated with a significant amount of commercial contract revenues) and a near-term capital raise. Either alone would significantly impact Akerna’s share price. Add these to the increasing uncertainty of Akerna’s largest government contract (Pennsylvania at > 30% FY 19 sales), stagnant sequential bookings during a critical growth phase in the cannabis ERP software market, and legitimate concerns involving the profitability of new contracts (Utah for example) and recent acquisitions of solo sciences and Ample Organics.

We believe shares are vulnerable here given these issues and a valuation that implies a much higher level of growth and profitability. We recommend avoiding the stock or establishing an opportunistic short. Factors limiting upside include 5.8m warrants exercisable at $11.50 and ~3m shares currently restricted by a lock-up agreement expiring in June 2020.