- Recently announced Phase 3 lung cancer data is likely weaker than claimed given lack of standard disclosure and a history of poor trial conduct

- Expect a denial at the upcoming FDA decision for chemotherapy-induced neutropenia, BYSI’s only other late-stage effort

- We identify inaccurate data reporting and contradictory management statements regarding critical trial issues. Both strongly suggest BYSI is incapable of producing an adequate NDA

- We estimate only 10% of enrollment in BeyondSpring’s mid and late-stage trials is based in US. Majority of sites and subjects are in China and Eastern Europe where trial conduct is questionable

- BeyondSpring’s chemotherapy-induced neutropenia US NDA is based on a Phase 3 trial that only included patients from China and Ukraine. We find it hard to imagine how such data will satisfy the FDA

- Two leading oncologists express skepticism regarding Plinabulin’s efficacy and approvability in neutropenia and lung cancer

- Base case: Lung cancer data is less than claimed and FDA denial in neutropenia. Shares are worth $5/share (cash plus protein degrader platform value)

BeyondSpring (NASDAQ: BYSI) (“the Company”) is a $1.2B Cayman Island-based biotechnology company developing a drug known as Plinabulin for chemotherapy-induced neutropenia (CIN) and non-small cell lung cancer (NSCLC). The company has completed Phase 3 registrational trials in both indications, filing for approval in CIN in March and announcing top-line NSCLC results in August. BYSI shares are up 200% since August 4 after the company published data from the Phase 3 NSCLC trial.

In this report we present major issues which cast doubt on the validity of BeyondSpring’s clinical trial data and the approvability of Plinabulin in either disease. These include inadequate control of clinical trials, misrepresentation and poor disclosure of results, and management misstatements.

Two important near-term catalysts are approaching: an FDA decision on the CIN application by November 30, and a presentation of a more complete NSCLC data set at the European Society for Medical Oncology (ESMO) meeting September 16-20. In the context of the issues we present, both events put the stock at high risk of retracement.

The trials supporting BeyondSpring’s New Drug Application (NDA) for CIN underwent multiple abrupt changes in protocol and endpoints. Moreover, the trials included very few patients from the US, and the Phase 3 registrational trial on which the NDA is based contained no US participants. We think the combined issues preclude approval.

Shares are more immediately at risk when the company presents Phase 3 NSCLC data at ESMO. Considering Plinabulin’s failure in a NSCLC trial in 2011, and the issues presented in this report, we believe the data will disappoint. The initial disclosure in August omitted key information, suggesting the company was painting over underwhelming data.

Since its incorporation in 2014, BeyondSpring has “kicked the can down the road” somewhat successfully, conducting mid- and late-stage trials that would take several years. Now that the trials are complete and an NDA has been submitted, BeyondSpring has little room to maneuver. We think Plinabulin will prove worthless, putting fair value of BYSI shares at approximately $5 which includes current cash of $75m ($2/share) and a 60% stake in Seed Therapeutics, a discovery stage protein degradation subsidiary which we generously value at $120m ($3/share).

NSCLC: Limited Disclosure, Contradictory Management Statements

Non-Small Cell Lung Cancer Phase 3 Trial

BeyondSpring’s Phase 3 trial in NSCLC (NCT02504489), known as DUBLIN-3, was a single-blind study comparing a combination of plinabulin and the chemotherapy drug docetaxel against docetaxel monotherapy in second-line, or “2L”, patients (those who failed first-line therapy). The primary endpoint was length of overall survival (OS). Secondary endpoints included tumor response rates (ORR), progression free survival (PFS), and neutropenia occurrence. On August 4, BeyondSpring announced the trial met the primary and several secondary endpoints.

While the stock reacted positively on the announcement, BYSI did not disclose several key data points which in our view suggests the data is not as strong as it appears. The most important omission was disclosure of mean and log-rank OS significance rather than median OS. Median is the standard descriptive statistic in oncology trials as it mitigates the effects of outliers. Moreover, no actual values were disclosed. BeyondSpring only shared the statistical significance of mean and log-rank OS which at p=0.03 and p=0.04 just sneak under the defined p=0.046 significance limit.

Previously BeyondSpring guided for median overall survival. Excerpt from the 2019 20-F [Pg.68]:

“If p-value for the median overall survival at the second interim analysis is less or equal to 0.012, the trial may stop early. If p-value for the median overall survival at the second interim analysis is greater than 0.012, the study will continue and final results of the trial at a death event of 439 patients are expected to be available in 2020. If p-value for median overall survival for the final results is less than or equal to 0.05, the study can be claimed successful.”

The 2020 20-F removed “median overall survival” from the same DUBLIN-3 section [Pg.86], a subtle change that went unnoticed until now:

“We reached the second pre-specified interim analysis at a death event of approximately 293 patients in the first quarter of 2020, and based on benefit and risk ratio, DSMB advised the study to continue to the final analysis. Final top-line results of the trial at a death event of 439 patients are expected to be available in mid-year of 2021. If p-value for overall survival for the final results is less than or equal to 0.046, the study can be considered successful.”

BeyondSpring also did not disclose the hazard ratio (HR), a standard measure of risk differentiation between trial arms. The press release and presentation slides in the accompanying conference call did not include the HR. During the August 4 data discussion conference call, when asked to provide color on the HR, Chief Medical Officer Ramon Mohanlal only said it was “within expectations”. In an SEC filing the next day, the same slide deck included an HR of 0.82.

August 4 Conference Call Slide:

August 5 SEC Filing:

In context of the data disclosed, the 0.82 HR is a hint that the overall data is not clinically meaningful. The American Society of Clinical Oncology (ASCO) defines a clinically meaningful HR goal below 0.8 in NSCLC trials.

A mean OS that barely met statistical significance and flip-flopping disclosure of an HR worse than the ASCO defined level suggests median OS is clinically insignificant.

CEO’s Conflicting Statement: Patient Demographics

During the conference call [27:00], CEO Lan Huang said approximately 20% of patients were from US, implying 80% were from Australia and China.

Analyst: “What percentage of patients were enrolled in North America?”

Huang: “What’s the percentage of patients?”

Analyst: “Yes please.”

Huang: “It’s around 20%.”

Yet the risks section of the 2020 20-F filed in April [Pg.13] states that 13% of patients are from the US/Australia and 87% are from China. If the filing is accurate, no more than 13% of patients are from the US.

The target trial population makeup has shifted negatively over time. At trial initiation in late 2015, BeyondSpring targeted enrollment at 80% in China and 20% in US and Australia [Pg.21]. Recruitment began in the US but was suspended for several months before restarting in June 2016 [Pg.99]. This 80/20 mix remained the target until 2020 when it changed to an 85/15 split [Pg.13] and then by 2021 to 87/13.

If BeyondSpring files for approval in the US, the fact that 87% of trial participants were from China will be a difficult hurdle. We spoke to experts who highlighted the risk of patient imbalances in BYSI’s trials. Among the concerns is that race and ethnicity can be a significant factor in how drugs affect patients. CEO Huang claims BYSI has received reassurance that the imbalance is acceptable if pharmacokinetic data among Asian and Western patients is consistent. The company claims it has generated this data but has yet to disclose anything.

DUBLIN-3 Does Not Represent Current Standard of Care

Only 15% of participants in the trial received prior checkpoint inhibitor therapy, which is current first-line standard of care. So, DUBLIN-3’s patient pool is unrepresentative of 2L/3L NSCLC patients. The severe lack of PD-1 experienced patients is unexplained since DUBLIN-3 was initiated in June 2016, just months before the first checkpoint inhibitor, Keytruda, was approved as first-line treatment for patients with high PD-L1 expression. Moreover, approximately 65% of enrollment occurred after ASCO updated guidelines in 2017 to make Keytruda and other PD-1 inhibitors first-line therapy and second-line therapy in patients who progressed after chemotherapy.

Chemotherapy-Induced Neutropenia: Poorly Managed Clinical Trials, Disclosure Issues

PROTECTIVE-1 Phase 2

BeyondSpring initiated two Phase 2/3 clinical trials for CIN in 2017: Study 105 (PROTECTIVE-1) and Study 106 (PROTECTIVE-2). The Phase 3 portion of Study 106 forms the basis of the company’s NDA with the other trials being supportive. We identify concerns with all of them.

Initially, BeyondSpring positioned Plinabulin as an alternative to CIN standard of care Neulasta. Study 105 Phase 2 (NCT04345900) was designed to test if Plinabulin was non-inferior to Neulasta in preventing CIN in patients undergoing intermediate-risk chemotherapy. The trial was initially double-blinded but was changed to open-label after the first six patients to “facilitate pharmacokinetic and pharmacodynamic sampling”.

In December 2017, BYSI issued a press release announcing the trial met its “primary objective” – selecting a Phase 3 dose. No information was provided on the primary efficacy endpoint, non-inferiority to Neulasta in days of severe neutropenia (DSN), or any other data related to efficacy or safety. Top-line data was released at the ASCO-SITC conference in late January 2018.

In the press release, the number of patients in the 20mg and 5mg Plinabulin arms don’t match.

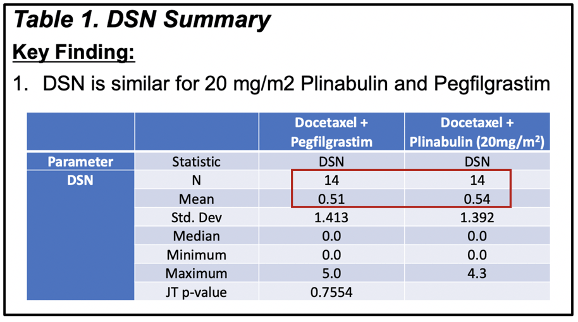

BeyondSpring’s poster at the 2018 ASCO meeting in June was also inconsistent. Here the 10mg and 20mg arm contain 13 and 14 patients, respectively.

The efficacy figures also changed in the poster. The DSN for the 20mg Plinabulin and Neulasta arms are much closer at 0.51 and 0.54, compared to 0.38 and 0.14 presented at ASCO-SITC (shown above).

BeyondSpring claimed it used “an FDA-accepted method for small-sample-size extrapolation” to calculate DSN without providing detail. In any case this doesn’t explain why the 20mg arm added a patient.

The efficacy figures changed in a poster presented at the 2018 American Society of Hematology (ASH) meeting in December 2018. DSN for the 20mg Plinabulin and Neulasta arms now both 0.5, compared to 0.54 and 0.51 when the data was presented at ASCO.

Perhaps BeyondSpring was simply rounding both figures down. However, when the data was first presented at ASCO-SITC, the company called DSN differences of 0.03 evidence of dose-response.

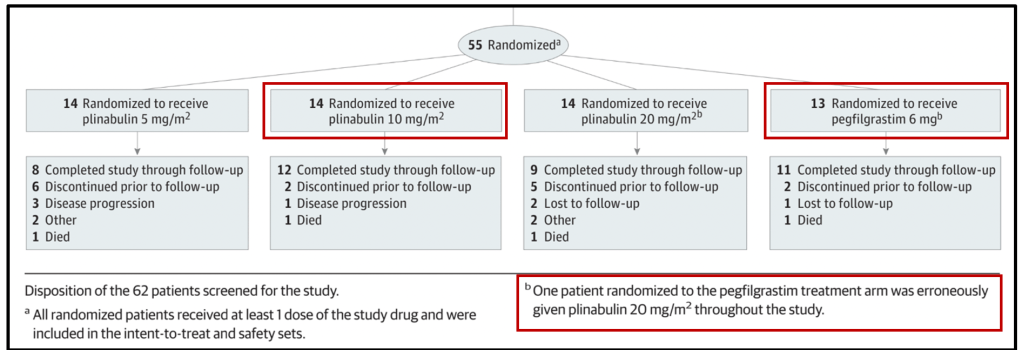

Trial data changed again in a paper published by Study 105 investigators in the September 2020 issue of JAMA Oncology. The paper noted 13 of 42 (30%) patients in the Plinabulin arms discontinued treatment prior to study follow-up vs 15% of patients in the Neulasta and “one patient randomized to the Neulasta treatment arm was erroneously given 20mg/m2 Plinabulin throughout the trial.”

Here the docetaxel + pegfilgrastim control arm contains 13 subjects, and all Plinabulin arms contain 14.

And DSN for the 20mg and 5mg Plinabulin arms have been changed again. Now 5mg Plinabulin appears to be most efficacious, negating the dose-response claim.

Returning to the ASH poster, BeyondSpring stated “Plinabulin did not cause hypertension”.

This contradicts data in the JAMA paper, which notes 7 cases of hypertension in the Plinabulin arms (vs 0 in the control).

PROTECTIVE-1 Phase 3

The Phase 3 portion of Study 105 (NCT03102606) was initiated in March 2018 with a target enrollment of 150 patients. Little information was shared until December 2018 when, without providing any supportive data, BeyondSpring announced the study met its primary endpoint of non-inferiority to Neulasta at an interim analysis. While not explicitly noting it, language in the press release hints the trial was stopped early. This appears to violate trial protocol which allows early stopping for superiority or inferiority, but not for non-inferiority [Pg.102].

During the Q2 2018 earnings call, CMO Mohanlal was asked about early stopping rules for the trial. His answer contradicts the protocol.

“Yes. The phase 3 of study 105 have built in an interim analysis, which was previously disclosed at around 100 patients, means 50 patients in each arm. That will trigger the pre-planned interim analysis, which is currently ongoing. The conditions around the pre-planned interim analysis indeed would allow for really stopping the study if you meet primary endpoint.”

For the next two years, sell-side analysts believed the trial was ongoing. On the Q2 2020 call an analyst asked for an update. CEO Huang’s response reveals the Phase 3 trial was not stopped early due to it meeting a pre-defined endpoint, but rather that Plinabulin monotherapy was no longer the goal, so there was no point in continuing.

“So, for [Study 105 Phase 3] – our interim analysis for the first 105 patients has completed, I think, last year, right, and we had a press release at the end of 2018 showing that we did beat the statistical significance for the primary endpoint ensuring the DSN non-inferiority for Plinabulin versus Neulasta alone.

So, these things we are going forward with the combination label for Neulasta and Plinabulin. So, for the PROTECTIVE-1 as a monotherapy, it’s a supportive study for this label. So – and it has also shown the first week early onset mechanism of Plinabulin in multiple cancer types. So that study is basically complete to be the supportive trial. So, we’re not doing anything for that.”

PROTECTIVE-2 Phase 2

Study 106 was a Phase 2/3 trial originally designed to show the superiority of single-agent Plinabulin to Neulasta in CIN prevention for patients using the high-risk chemotherapy, TAC. The Phase 2 portion of Study 106 was open-label (NCT04227990) and initiated enrollment in November 2017.

Enrollment began in China, but CEO Huang claimed expansion to US and Europe:

“We expect U.S. and European sites within the next several months. The Chinese regulatory agencies have been very supportive of Plinabulin for the Phase 3 program for the CIN indication and non-small cell lung cancer (NSCLC) indication, allowing for a shorter time-to-market. With this accelerated path, we expect the CFDA filings of our first NDAs for both the CIN and NSCLC indications potentially in 2018.”

Enrollment was never expanded to the US, the only other country added was Ukraine, and BYSI only completed its China CIN filing in March 2021. NSCLC has not been filed.

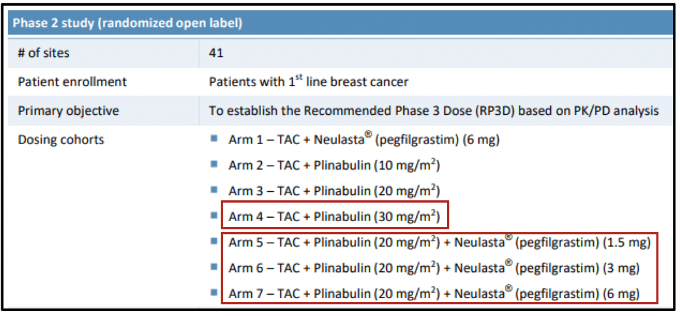

During the summer of 2018 the trial design changed. Instead of testing Plinabulin as a single-agent, Study 106 would test a combination of Plinabulin and Neulasta against Neulasta alone. Without notifying investors, BeyondSpring added four arms: 30mg Plinabulin alone, and 20mg Plinabulin combined with 5mg, 3mg and 1.5mg arms of Neulasta presumably to test if Neulasta dosing could be lowered with the addition of Plinabulin.

The shift to focus on combination therapy leads to two conclusions. First, despite BYSI’s claims, Plinabulin as a single agent is clinically inferior to Neulasta (the addition of the 30mg arm hints that results were weak at lower doses). Second, since a non-inferiority claim isn’t viable, continuing the Phase 3 portion of Study 105 was a waste of resources. Thus, BYSI violated protocol and stopped at the interim analysis

Investors were first notified of the change in an October 2018 press release announcing “positive efficacy and safety data”. BYSI only provided pooled data from the combination arms. No information has been disclosed for the three Plinabulin monotherapy arms.

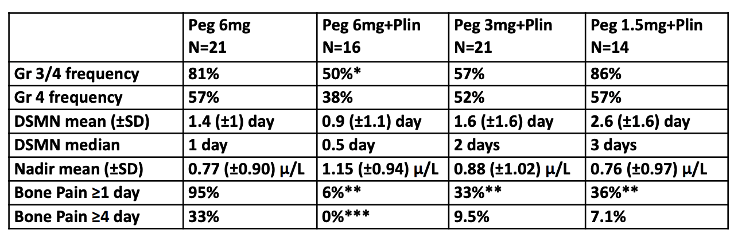

BeyondSpring presented a poster on the study at the American Society of Hematology (ASH) meeting in December 2018.

It’s clear from the data that concurrent administration of Plinabulin doesn’t allow for lower doses of Neulasta. The 3mg and 1.5mg combination arms are worse on DSN than 6mg monotherapy.

Until this point, BeyondSpring positioned Plinabulin as an alternative to standard of care G-CSF offering dosing convenience (can be dosed on the same day as chemotherapy while G-CSF must be dosed one day after) and safety benefits including reduced bone pain. Neulasta and other G-CSFs act by stimulating the bone marrow to produce neutrophils. This stimulation is thought to be the primary cause of bone pain in patients on Neulasta. Since Plinabulin does not stimulate bone marrow, it should cause less or no bone pain.

After disappointing single-agent Plinabulin results, the story shifted to the superiority of a Plinabulin and Neulasta combination. The data in the ASH poster highlights what look like benefits of the 6mg combination arm: numerical improvements in neutropenia and bone pain. However, the combination was only statistically significant in Grade 3/4 frequency – not in Grade 4 (severe neutropenia) or DSN.

Moreover, instead of disclosing severity of bone pain, the measurements are arbitrary. Also, the Phase 2 portion of Study 106 was open label and bone pain was measured using a questionnaire. Patient reported outcomes in small, open label trials are typically unreliable. And why would adding Plinabulin to Neulasta reduce bone pain? BeyondSpring theorizes the drug protects neutrophils. The bone pain theory might make sense for single-agent Plinabulin, but not in combination with Neulasta. The company has never provided a coherent explanation.

PROTECTIVE-2 Phase 3

A year after releasing the Study 106 Phase 2 top-line data, BeyondSpring announced enrollment initiation for the “global” Phase 3 (NCT03294577) in October 2019. As in the Phase 2, enrollment occurred only in China and Ukraine.

Six months later, an April 2020 press release announced BYSI was changing the primary endpoint from DSN to rate of prevention of severe neutropenia. Supporting this change, BYSI claimed 62.5% of patients on combination therapy in the Phase 2 had no severe neutropenia compared to 40.9% of patients on Neulasta (initially reported as 37.5% before BYSI issued a correction). The company said a “robust plan will be submitted to the FDA to prospectively validate this new primary endpoint against clinical outcome measures.” BeyondSpring has not disclosed the status of this plan.

In June 2020, BYSI announced “positive” interim results for the Phase 3 trial. Top-line results for the complete trial were announced in November. The Plinabulin-Neulasta combination met the primary endpoint and several secondary endpoints.

Reduction of bone pain in the study was highlighted in a 2021 ASCO poster. Note essentially all of the improvement is at Grade 1 and no Grade 3 or 4 pain was seen in the Neulasta arms. Recall BeyondSpring was selling reduced bone pain as one of the most important advantages of Plinabulin (“bone pain” is mentioned 9 times in the JAMA paper).

While apparently reading out positively, we reiterate that this trial forms the basis of BeyondSpring’s CIN NDA yet enrolled zero patients in the US. Investors may be unaware that PROTECTIVE-2 did not include US patients as until this year, BeyondSpring was guiding for US enrollment. Below is an excerpt from the 2019 20-F [Pg. 63]:

“The second trial, Study 106, is a Phase 2/3 trial of Plinabulin in combination with a myelosuppressive chemotherapeutic regimen composed of three agents, Taxotere (docetaxel), Adriamycin (doxorubicin) and Cytoxan (cyclophosphamide) in approximately 300 patients with solid tumors in the U.S., China, Russia and the Ukraine.”

The company changed the trial description in the 2020 20-F filed on April 30, 2021 [Pg. 67]. This was after enrollment was complete and the NDA was filed:

“The second trial, PROTECTIVE-2, is a Phase 2/3 trial of Plinabulin in combination with a myelosuppressive chemotherapeutic regimen composed of three agents, Taxotere (docetaxel), Adriamycin (doxorubicin) and Cytoxan (cyclophosphamide) in 336 patients with solid tumors (breast cancer) in China and the Ukraine.”

FDA regulations require NDAs based solely on foreign clinical data to demonstrate the “data are applicable to the US population and US medical practice.” We’re skeptical the trial meets this standard, in part because it contains mostly Asian patients, but also because it was in patients undergoing TAC chemotherapy which, according to oncologists we spoke with, is used infrequently in the US.

Experts Skeptical Around Efficacy and Lack of Disclosure

Two experts provided opinions on the NSCLC and CIN trials and data. Both expressed skepticism of the drug’s potential and the data disclosed thus far. We approached Expert #1 as investors conducting diligence on BYSI’s CIN trials and data. Expert #2 answered questions on an investor sponsored research call to discuss the company’s NSCLC data.

Expert #1: Medical Oncologist and Cancer Epidemiologist. As a practicing oncologist since 1986 and cancer epidemiologist for 40 years, he has extensive experience with high-risk chemotherapy treatments, is very familiar with neutropenia and has in-depth understanding of currently marketed drugs and experimental treatments.

Expert #2: Vice Chair of the Department of Hematology and Medical Oncology at a top national hospital. Thoracic medical oncologist with more than 20 years of clinical experience. Clinical investigator in NSCLC, small cell lung cancer and mesothelioma trials.

Our conversation with Expert #1 was focused on CIN. He was extremely doubtful of Plinabulin’s utility in combination with Neulasta. He also thought Plinabulin’s supposed early action in chemotherapy cycles if true was unneeded:

The bone pain they talk about is irrelevant. I’ve been using G-CSFs in at least 100 patients a year for 20 years. You take Motrin, Tylenol, whatever, it goes away.

The fact that they have Grade 3 or Grade 4 neutropenia doesn’t mean anything. What you want to know is whether it affected the patient…The greater the neutropenia isn’t what stops you, it’s the platelet count. You can always give G-CSG… This is absolutely worthless.

The first week of chemotherapy is not when you get neutropenic fever. Not at all unless they have no bone marrow. With TAC it’s going to happen in the second week, day 10-14. That’s why you give them Neulasta… If you’re worrying about early bone marrow suppression you give them [short-acting G-CSF]. If you’re worrying about delayed, you use Neulasta.

[Neutrophils below 500] does not matter. It’s when you have zero to 100 when you have problems. It’s not just the Grade 4… The risk of infection with neutrophil count at 250 or 100 is low if it’s only a day or two. It’s not clinically relevant.

Expert #1 found concerns in the design of the CIN trials and disclosure of results:

Asian women handle these drugs so differently than Caucasian. I don’t know how you can compare the Asian patient with Eastern European. Ethnicity is really important in dealing with these drugs.”

The drug may work but the trial design is so bad, that it may even be hiding an effect… The fact that it comes out of China and Ukraine, I think it’s a non-starter for the FDA.

The biggest problem I see is lack of transparency. If you don’t have all the data, if you can’t evaluate the patients being selected, if you can’t figure out why they changed what they did, it’s hard to make any decision about the results they claim they’ve had without seeing the actual physiology patient information.

Expert #2 focused on the DUBLIN-3 NSCLC data. He expressed concern about the disclosure of mean vs median, and Plinabulin’s MOA which appears conflicting:

Yeah. I mean, in terms of knowledge of the drug, I’m aware of it. I hadn’t had any clinical experience with it, personally, through any trials, but, I guess my original awareness of it was as an agent that could maybe prevent neutropenia, which was interesting based on its mechanism of action being an anti-microtubule agent. So, it was a little bit surprising that that would be some part of its therapeutic benefit in terms of the whole neutropenia aspect. And then on top of that, looking at it as an antineoplastic too.

Well, I mean, it’s pretty standard to report medians in large, randomized trials like this. So obviously with the median sort of lessening the impact of outliers. So, yeah, I mean, there’s a question mark there. Although I think it’s there, but then it gets lessened by these, I think, the secondary endpoints. Response rate improving, PFS, like to see the actual numbers and then the two-, three- and four-year OS rates. They definitely are, I think, strengthen the findings here, but you’d have questions about the population in terms of receipt of immunotherapy, especially…

So, I think that the other question, like I said when we started out, is how does this agent have anti-tumor efficacy and prevent neutropenia at the same time? Yeah. Is it the prevention in the neutropenia that leads to improved outcomes? Or so, I think, that also leads to some of the questions about this drug kind of doing both things, which we’ve never really had sort of other examples of this to add cytotoxic activity, but also prevent bone marrow suppression.

Expert #2 noted that imbalances in prior immunotherapy treatment between arms could be skewing data:

That would be a concern. If there was an imbalance. If it wasn’t an imbalance, then it would be less of a concern. I mean, this would still be representative of activity. So, I still think if there wasn’t one group that… If the Plinabulin group did not have greater immunotherapy usage, then that would be… I still feel like the results would be applicable even if the majority did not have immunotherapy. So, right, like that would be a question.

And in fact, that there could have even been an imbalance in the post study treatments, in which certain people may have gotten immunotherapy after the trial that might’ve led to, again, some of those longer-term survival numbers being imbalanced as well.

Expert #2 was concerned with the HR value of 0.82 and geographic imbalances:

I mean, it makes you wonder. That just the numbers aren’t going to be, associated with that, aren’t going to be as impressive. Right. Still not a deal breaker, but usually an effective therapy is, in a randomized trial like this, you’re going to see an HR lower than that.

I don’t know about the stats analysis. I don’t have the background to say that, but if it’s enough to make you question the validity of the results, then it won’t get approved. Right. I guess that could be the difference between… Even though like, again, just going back to [ramucirumab trial], it was a well-done trial in terms of its randomization and follow up, and that did lead to approval even with a marginal benefit. So, the results need to be… So obviously they felt that the results were valid based on everything that was presented. So, you got to come to the table with all of that or… Right. There’s going to be a greater likelihood to say go back to the drawing board and try again. But I mean, those, like I said, those outliers could, they would be the ones who would be driving a mean type of value and not so much a median.

I mean, there’s still definitely significant uncertainty. Like I said, the primarily Asian population and the timeframe that it took to report from completion of accrual to this. Again, the mean business, hazard ratio that was put out there and then recalled or something. Those make you raise your eyebrow.

Implication: Stock at Risk Ahead of Near-Term Catalysts

In summary, we believe BeyondSpring’s clinical trials are inadequate to support approval in both CIN and NSCLC (may be why no US-based hedge funds own shares in any notable size). The company’s CIN trials are marked by numerous serious issues including endpoints and blinding that change mid-trial, a major protocol violation, and conflicting data reporting. Moreover, we estimate only around 10% of patients were recruited from the US in the CIN trials, and zero in the registrational trial. It’s reasonable to assume the FDA will find the application difficult if not impossible.

While the stock reacted positively to the Phase 3 NSCLC data announced last month, the trial is stained by similar issues in our view. Management misstatements, an apparent change in the primary endpoint measure, and a lack of US enrollment strongly suggest that BeyondSpring does not have data to support approval. We think this will likely be evident when the company discloses the complete data at the ESMO conference this month.

We believe BeyondSpring shares are substantially overvalued and recommend it as a short idea. As with all short positions, sizing is key but especially so for BYSI given the volatility and the upcoming catalysts. Investors should consider adding short exposure at current levels before ESMO, or after the data release as a sell-the-news trade. And we are highly convicted that the FDA will not approve the CIN NDA on or before the November 30 PDUFA date. If both of our views play out, we think the stock could trade below $10 by the end of the year.

Note: We emailed our allegations and questions to BeyondSpring IR. The company has not responded at the time of publishing.