- Cielo claims to have funding through Joint Ventures with a related party known as Renewable U Energy (RUEI). RUEI’s founders concurrently ran Cielo Investor Relations in exchange for millions in Cielo equity

- We uncover evidence that RUEI is financially weak – its currently struggling to raise a meager $1.5m, strongly indicating the $150m necessary for the first JV facility is out of reach

- Cielo’s inability to attract funding and a credible partner (RUEI’s ex-CEO previously managed car dealerships) suggests it’s unlikely to hit commercialization or profitability

- Cielo has struggled to desulfurize its fuel to industry standards, offering excuses for years. We spoke to an expert who calls this puzzling since desulfurization is an off-the-shelf technology.

- A $1.5m fuel sale appeared to substantiate Cielo’s commercial potential. However, we find the buyer received compensation worth $3m three days post announcement, indicating a mock transaction in our view

- Cielo’s attempts to imply third-party validation and financial strength include the announcement of a nonsensical $14m zero-interest, unsecured loan for land. We suspect the financing was dilutive equity disguised as attractive debt

- We spoke to Cielo’s COO and RUEI’s CEO and neither were able to explain the bizarre “loan” terms

- CEO Donald Allan’s previous public energy companies ended poorly for shareholders – forced to delist, surrender assets, or liquidate to satisfy creditors

- Recent stock strength, fueled by a Canadian money-manager whose analysis contains key errors, contributes to the illusion that Cielo is near commercialization. Expect shares to return to pre-hype levels 90% lower

Cielo Waste Solutions (CSE:CMC) (“the Company”) is a $600m Vancouver-based producer of renewable diesel. CMC shares are up 1000% since the beginning of February 2021 on the belief that Cielo is on the cusp of profitable commercial scale production. Since Cielo’s founding in 2011, CEO Donald Allan has promoted a technology supposedly capable of converting municipal solid waste into renewable diesel at a lower cost and higher price point compared to traditional biodiesel processes.

Cielo’s valuation is predicated on its access to non-dilutive funding through a series of Joint Ventures with an obscure entity known as Renewable U Energy Inc. (RUEI). Cielo claims RUEI has access to ~$800m of investor capital for nine planned facilities, resolving a significant financing overhang.

However, we uncover evidence suggesting RUEI does not have ANY funding lined up, nor is it likely to anytime soon. Undisclosed to Cielo shareholders, RUEI is soliciting individual investors for cash as it only has ~$300k – not even enough to fund its own working capital needs. Meanwhile, Cielo claims Renewable is paying for ongoing engineering work at the first JV site, estimated to cost at least $150m, and that construction will begin this quarter [8:00].

Moreover, RUEI is a blatant example of related party conflict of interest. Between September 2019 and March 2021, at the same time Cielo was signing the joint venture agreements, RUEI CEO Lionel Robins ran Cielo investor relations and its President Raphael Bohlmann provided public relations services. Further corrupting incentives, Robins and Bohlmann own a branding agency which received millions in Cielo equity.

In our view, RUEI is essentially a vehicle used to promote the commercial production story being told to support Cielo’s stock. While the rally has allowed Cielo to pay down $3.8m of debt via warrant exercises and add roughly $15m of cash, with over 650m shares fully diluted these numbers don’t move the needle. We find no evidence suggesting Cielo’s long history of delays is coming to an end and we expect shares to trade back to pre-February levels.

Contrary to Consensus, RUEI Is Struggling to Fund Trivial Expenses Let Alone The $800m Needed for Cielo’s Facilities

The belief that Renewable U Energy has an arranged group of lenders adds to the perception that Cielo is near commercialization. We have evidence indicating otherwise.

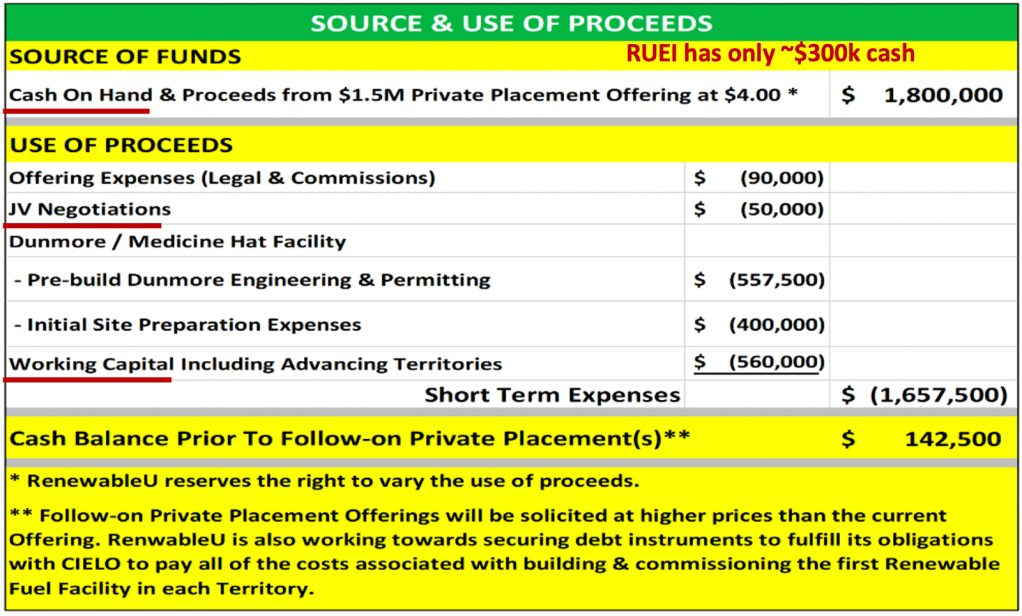

We contacted RUEI’s CEO Ryan Jackson and asked about the possibility of investing in the Joint Ventures. We were surprised to learn that in April, RUEI quietly began an attempt to raise $1.5m. Jackson said there was a “small amount of room left”, sending us an investor term sheet and slide deck. Over the phoneJackson said RUEI wasn’t marketing the deal widely, only sharing it through “word of mouth” to “friends and family”.

Source: Renewable CEO email

Source: Private RUEI offering document

While Cielo claims progress on the first JV facility (located in Medicine Hat, Alberta) is moving quickly with construction beginning this quarter, the offering deck paints a very different picture. Use of proceeds include JV negotiations, initial site preparation and working capital. Note Cielo and RUEI announced this JV in February 2019 – so it’s troubling that “JV negotiations” remain incomplete.

Source: Private RUEI offering document

Moreover, it’s worrisome that RUEI is raising such a small amount relative to estimated capital expenditures of $150m for the Medicine Hat facility (let alone ~$800m for all JV locations) and that it’s targeting such small investors with a flexible minimum buy-in of only $25k.

We think it’s clear that RUEI has made little meaningful progress finding capital for the JVs, the first of which was signed two and a half years ago. Because if RUEI had, its CEO wouldn’t be answering emails and offering to set up phone calls with random investors, struggling to cobble together $1.5m.

Joint Ventures Paint False Picture of Strength

In 2018 Cielo announced the first Joint Venture with Renewable, an entity specifically incorporated to act as Cielo’s counterparty. The terms appear extremely attractive for an unproven, highly speculative company like Cielo. RUEI will supposedly fund 100% of the capital expenditures for a share of the profits in nine production facilities expected to each cost $90m on average [Pg. 17].

The JV agreements created the perception that funding for Cielo’s facilities is resolved – normally a large overhang for emerging clean energy producers. Additionally, the JVs appear to provide third-party validation for CMC’s production technology and commercial potential.

Bulls Assume Joint Ventures Have Investor Backing

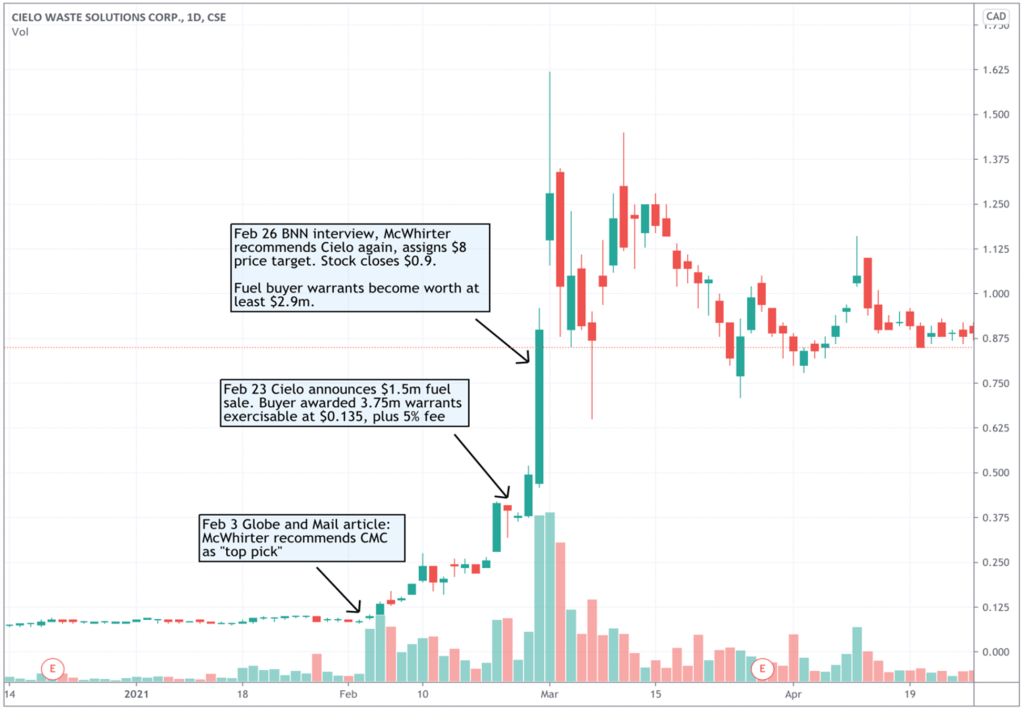

Cielo has implied RUEI had funding commitments as long as it met fuel production volume and sulfur content targets. Investor confidence in Cielo’s progress towards this milestone was likely fueled by the Company’s most prominent bull, Canadian money-manager Robert McWhirter of Selective Asset Management. McWhirter’s recommendations have led to large moves in the stock:

- February 3rd Globe and Mail article, McWhirter recommends CMC as a top pick when the stock was below $0.10, marking the start of a 400% rally in 3 weeks.

- February 26 BNN Bloomberg interview, McWhirter assigns a “conservative” $8 price target. Shares rally from $0.50 to $1 by the next day’s close.

At $8, the company would be worth an approximate $5bn, roughly equivalent to Chesapeake Energy (NASDAQ:CHK) or twice as much as Renewable Energy Group (NASDAQ:REGI), a company with an effective production capacity equal to 70 Cielo plants generating over $2bn in revenue last year [Pg.2].

In the BNN interview, McWhirter highlights the opportunity: as long as Cielo can desulfurize its fuel to industry standards, lenders are ready to fund facilities producing 10,000 liters/hour costing $50m each.

Other vocal bulls also assume Cielo has secured funding. See the blog ESG Fire at 40, which contains interviews with Cielo management and McWhirter. The risk of funding is hardly mentioned, only the revenue and earnings potential. The outlook is similar in a popular Cielo retail investor chat room where Renewable is assumed to have lenders waiting.

Source: Discord Cielo chat

McWhirter’s Analysis is Based on Faulty Assumptions

We note McWhirter’s analysis contain basic errors, the most obvious of which is his belief that $50m will fund a 10,000 liter/hour facility. Cielo claims each 4,000 liters/hour module or “plant” will cost $50m (one facility is made up of multiple plants) [Pg. 8]. McWhirter is confusing the cost of a plant with the cost of a facility.

Source: Cielo April investor presentation

McWhirter makes the same mistake in a March 6 interview: “Cielo has joint venture partners ready to build 5 facilities at $50m each and $250m total… Cielo has 2 outside financiers who want to build 5 plants.” While the point is moot since we believe the JVs are unfunded as discussed below, these basic errors should cast doubt on McWhirter’s recommendations.

Renewable U’s CEO: Cielo Far from Meeting Production Target

When asked why RUEI doesn’t have signed financing deals, Jackson noted the agreement with Cielo is contingent on its current facility achieving 30 days of continuous flow at 500 liters/hour of production (including desulfurization) but he’s only seen “5 or 6 days” of 500 liters/hour of continuous flow at Aldersyde – without desulfurization. In other words, Cielo is less than 20% of the way to meeting the target.

Jackson said Cielo claims it can do 1,000 liters/hour but he hasn’t seen it. Cielo has a long history of overpromising and underdelivering (Appendix). In June 2014 Allan claimed Cielo would be commercial by that Fall, with a 700 liters/hour plant running later in the year, and 12 plants generating $130m EBITDA within 2 years – seven years later Cielo has only recorded $1.5m in sales in a deal likely the result of significant inducement (see below). And last June, Allan claimed Cielo was at 1,000 liters/hour and by end of year would hit 2,000 liters/hour [3:40].

The announcements of the JVs added to the perception that Cielo was progressing by conferring outside, institutional credibility. However, with a fee of only $250k for each location – convertible into shares at $0.25 – there was never much at risk for RUEI. And unfortunately, insiders at RUEI were incentivized to promote the commercialization story as two of its founders are closely related to Cielo.

Renewable U: Brazen Example of Related Party Conflict of Interest

RUEI was founded by Lionel Robins, Raphael Bohlmann, and Eric Leslie. Robins was CEO, Bohlmann President and both sat on the board with Leslie, a money manager and associate of Don Allan who was a board member at Allan’s previous, now defunct energy company Blue Horizon.

The three are also partners in Motivate U, a management training company, and Brand U, a marketing services firm. Robins and Bohlmann are also connected through Revolution Auto Group, an Alberta-based automotive dealership group where Robins was CEO and Bohlmann was head of marketing.

Beginning in September 2019, Robins ran Cielo investor relations and Bohlmann provided public relations services to the Company. Thus, Robins and Bohlmann were promoting Cielo while they were announcing joint venture agreements from RUEI. At the same time, both were at least in part compensated with CMC shares awarded to Brand U – since April 2020, Brand U has been awarded over 4m shares of Cielo stock.

We asked Cielo for comment on the conflict of interest arising from the related party relationship. Cielo investor relations told us the conflicts will be addressed in the definitive JV agreements and that both parties will execute based on the agreement.

Last month Robins and Bohlmann resigned from RUEI (although both remain on its board) to join Cielo: Robins as COO and Bohlmann as VP of Marketing. Ryan Jackson replaced Robins as CEO of Renewable. Prior to RUEI, Jackson was head of Canadian operations at cannabis company Folium Biosciences. Coincidentally, Folium announced plans in January 2019 to build a $30m hemp extraction plant in Medicine Hat but never did, despite public reassurances in November 2019 and February 2020. Folium was also the subject of a 2020 SEC inquiry over payments to related parties.

Renewable also hired a CFO, Manager of Land and Real Estate Acquisitions, Business Development Manager and an Office Manager. Outside of Jackson, we find the work experience of Renewable’s employees (real estate appraisal, consulting, local government management) to be unconventional for a firm facilitating the raise of nearly a billion dollars.

From our conversation with Jackson, we got the impression that he and the rest of RUEI’s new staff were not fully aware of the lack of progress at Cielo. We would not be surprised to see resignations before year end.

Buyer in Highly Touted $1.5m Fuel Sale Received $3m in Compensation

The only meaningful commercial deal Cielo has managed to date occurred in February. Cielo announced a purchase commitment of 900k liters of renewable diesel for $1.5m.

The buyer was undisclosed indicating, in our view, the party is not a large energy or industrial company. We see no reason why a traditional buyer would want to remain confidential (it would be a positive for the buyer from an ESG public relations perspective), and Cielo is incentivized to disclose a valid buyer as it adds credibility.

In Cielo’s press release, the party who brokered the transaction receives warrants and a 5% broker fee. However, in an interview two weeks later, Allan essentially admits the buyer and broker are the same [6:00]:

“Why there’s warrants attached to [the fuel sale], we need to do one more step in our process, it’s the final step to put a desulfurization unit in… We actually talked [the buyer] into pre-paying the order, even though we don’t have that process in place… To de-risk it we allowed them some stock in the company.”

Cielo apparently incentivized the buyer with 3.75m 2-year warrants exercisable immediately at $0.135. CMC shares closed at $0.41 the previous day, and thus the warrants were worth over $1m. Cielo also paid the buyer a 5% broker fee which is odd for a commodity like renewable diesel, and of course because the buyer is evidently the broker. The transaction is similar to the sale of a $1.5m house in which the seller awards the buyer over $1m in cash and agent fees.

The sequence of events is noteworthy: On February 23 Cielo announces the $1.5m fuel sale. The buyer is induced with 3.75m warrants in the money by over $1m plus a fee of $75k on or about February 26. Total up front compensation to buyer is $1.1m. On February 26, Robert McWhirter recommends CMC stock in a BNN Bloomberg interview with a “conservative” $8 price target and shares close at $0.90. The buyer’s warrants are now in the money by $2.9m.

Despite Cielo’s portrayal of the sale as validation from a customer, this was a near riskless transaction for Cielo’s counterparty which inside of three days became extraordinarily profitable.

Bizarre Zero-Interest Loan Provides Appearance of Third-Party Validation

In December 2020, Cielo announced it was seeking $12-15m in debt. Although Allan claimed to have term sheets from lenders, no updates were provided until March when Cielo announced a binding letter of intent on $10m of debt (later increased to $14m). The funds would be used to purchase a site for the company’s first, wholly owned facility.

The terms were peculiar: 12-month maturity, zero-interest, unsecured and convertible at $1.02. Cielo paid transactional fees of 7% and third-party commission fee of 8%.

Why would a lender offer Cielo, who had less than $5m in cash and was unlikely to begin generating free cash flow within a year, with $14m in unsecured, zero interest financing, most of it used to purchase land which could easily serve as collateral? Where is the upside for this supposed arms-length lender? Additionally, the conversion option isn’t appealing considering the stock was trading at $0.08 a few weeks earlier and arguably no meaningful developments had occurred in the interim.

We brought these concerns to Lionel Robins and Ryan Jackson. Both were at a loss to explain the terms. Robins nonsensically said Allan wanted to find mezzanine debt and that the conversion option was attractive if the stock went higher. Jackson said he wasn’t involved.

On May 3, Cielo announced the closing of $10m of the convertible debt, with all lenders electing to convert their holdings into shares at the previously announced price of $1.02.

As is common with Cielo, what should be straightforward is problematic. Cielo called the deal “non-brokered” even though it’s paying $1.5m in fees and the lenders were apparently so bullish they opted to convert into shares at a ~15% premium to market, a preposterous idea considering the circumstances. We were unable to locate Cielo’s counterparty, First Choice Financial (FCF), online unless it’s a one person insurance/wealth management firm or a company that provides trucking loans.

This supposed zero-interest unsecured debt created the appearance of third-party validation. We believe it was actually an equity offering rather than debt. The deal was announced two months ago – we await the filing as it wouldn’t surprise us if the deal closed when the stock was trading above $1.02 or if the lenders were members of management or Allan himself.

Besides the unsavory details, the deal again presents Cielo’s underlying contradiction – if the Company and its well-financed partners will soon produce hundreds of millions of gallons of highly profitable fuel, why is it necessary for Cielo to engage other investors under such oddball terms?

Cielo Struggles with Desulfurization – Reality or Excuse?

Cielo announced last month that it “resolved the desulfurization issue”, supposedly the final piece before the JV partners release funds according to McWhirter and other bulls. We have doubts given Cielo’s history of delays.

We spoke with an industry expert with 35 years of experience in petroleum, biodiesel and renewable diesel. He’s held senior roles including Chief Technology Officer of a publicly traded biofuel company and has advised DOE, USDA and EPA on biomass and renewable fuel technologies.

We asked if it was common for renewable diesel producers to struggle with desulfurization, as Cielo has. He said it was strange Cielo would attempt to develop a new technology on its own as desulfurization is available in several off-the-shelf options.

“You’re asking a very good question. Normally desulfurization of a bio-crude or petroleum crude is not a core technology. In other words, Exxon has, you know, high sulfur oil going to a refinery. They use an amine. In other words, an amine system for bulk haul. So, it’s not a core technology, you buy it off the shelves… So why did you not just use a bolt on amine system to reduce sulfur for rather than, you know, spend time? Because usually sulfur removal is not a core process. It’s an ancillary process.”

Cielo itself called desulfurization “proven processes” in 2017. Yet almost four years later and desulfurization remains an issue – another sign of underlying problems and that the commercialization story presented by Cielo is not what it seems, in our view.

CEO Don Allan’s Previous Ventures Defunct

Don Allan has a long history of peddling failed technologies in the energy sector. He was CEO of Peace River Oil (PRO) in 2004, a company which claimed to have a technologically advanced crude upgrading process. Peace River was forced to liquidate assets to satisfy creditors [Pg. 32].

In 2005 Allan became CEO of Blue Horizon Industries Inc, a roll-up of energy, mining and biodiesel projects (including some of PRO’s assets). In 2011 subsidiary Blue Horizon Bio-Diesel was sold via reverse merger to Cielo Gold Corp which later changed its name to Cielo Waste Solutions. Parent Blue Horizon was so troubled it surrendered assets and was delisted in 2013.

Expect Stock to Return to Pre-Hype Levels

We think RUEI has failed to attract JV investors or credible partners because the likelihood of Cielo ever achieving profitable commercial scale is extremely low. Cielo has never attracted larger energy company offtake or municipal feedstock supplier partners who would lend credibility to the company and its process.

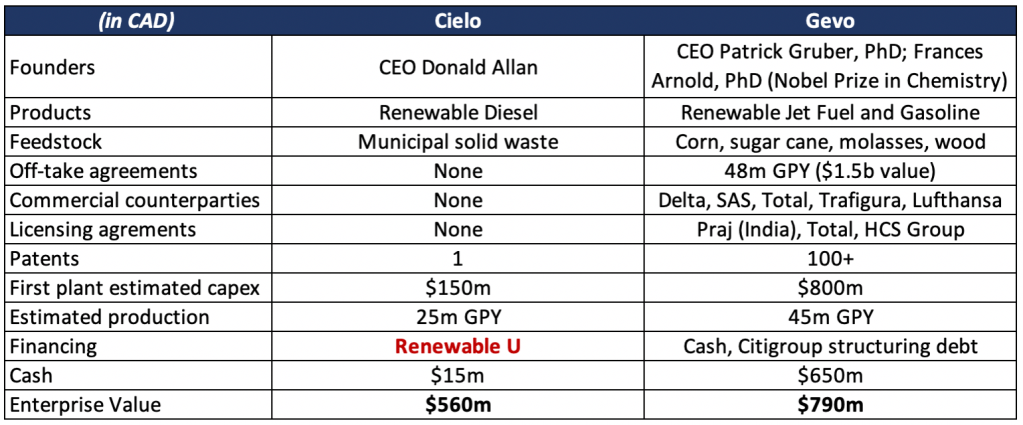

See competitors like private California-based Fulcrum Bioenergy which like Cielo converts municipal solid waste. Fulcrum has offtake deals with Cathay Pacific, United Airlines, BP and Marathon, and feedstock supply arrangements with Waste Management. Or look at Gevo, a renewable diesel producer based in Colorado. Cielo bulls are fond of making comparisons to Gevo because the economics appear tilted in Cielo’s favor as McWhirter observes:

“The biggest difference is that Cielo’s capex is estimated to be 1/10th that of GEVO’s $700 million USD for their planned South Dakota plant to produce the SAME volume!”

True if you trust Cielo’s estimates – but we’re skeptical considering the years of delays and the inconsistencies discussed. Moreover, like Fulcrum, Gevo has signed offtake partnerships with companies like Delta, Lufthansa, Total and SAS. We might be biased, but counterparties like Delta are not and only seek attractive partnerships.

Investors should ask why Cielo has only signed one agreement for rail tie feedstock and no fuel offtake agreements. What does this say about Cielo and its process? Cielo claims it has an offtake agreement for all of its fuel produced in North America [Pg.19]. However, the deal with Elbow River Marketing appears to be for marketing services, not a traditional offtake agreement in which a counterparty agrees to purchase fuel. We tried to contact Elbow River, but the listed phone doesn’t work.

We are short CMC as we believe Cielo’s current valuation significantly overprices the probability of successful near to medium-term commercialization. Risks to the upside include progress towards continuous flow production and desulfurization faster than we expect – but we are extremely convicted in our view. Besides Cielo’s established history of delays and disappointment, we find compelling evidence in RUEI’s distressed financial state, currently forced to solicit small investors for capital. It’s implausible that RUEI is in this circumstance yet somehow has access to nearly a billion dollars to fund construction of Cielo facilities.

The stock is extremely vulnerable here in our view, up 1000% in three months on a questionable fuel sale, a suspicious financing, a money manager’s sloppy recommendations and Donald Allan’s optimism. Much of the blame can also be placed at RUEI, where the conflicts of interest are some of the worst we’ve ever seen. The RUEI JVs appeared to validate Cielo’s potential, but are in reality paper-thin and unfunded.

Appendix: Selection of Cielo Delays

Source: Links