- CorMedix’s only clinical drug candidate, Neutrolin, targets an indication with numerous treatment options that are at least as effective and less costly.

- Neutrolin has been on the market in Europe and Middle East since 2013 yet has generated less than $1.4mn in cumulative sales.

- Competition from a newly developed, more convenient and likely cheaper preventative solution has recently been approved in the US.

- CorMedix faces a steep regulatory hurdle attempting to convince FDA to allow an NDA filing based on one instead of two Phase 3 trials.

- Even if Neutrolin is approved, we believe realistic market assumptions imply a valuation below $1/share.

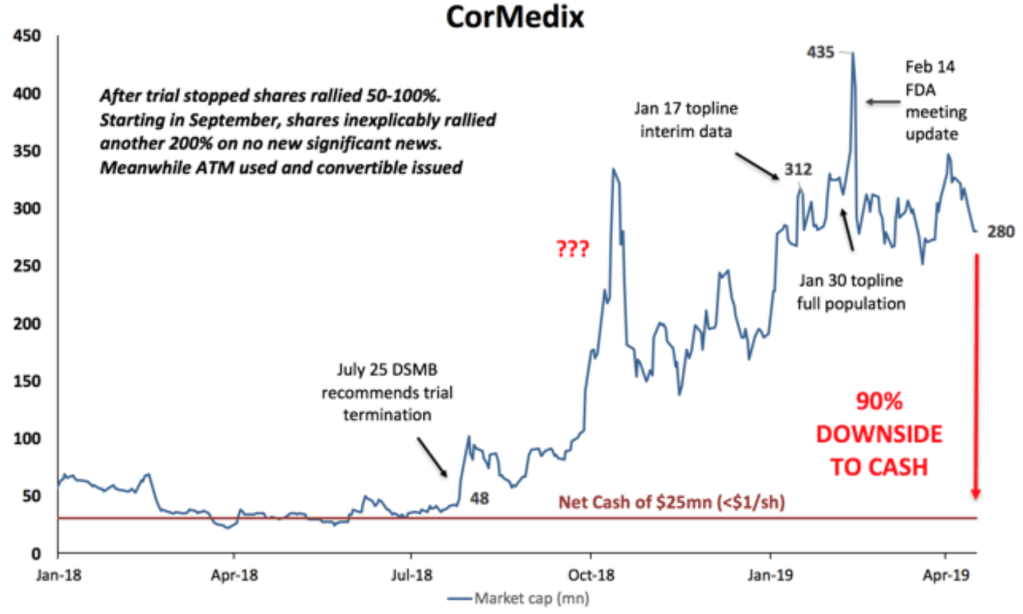

We believe CorMedix (CRMD) represents the classic case of an extremely overvalued small-cap biotech due to a large and enthusiastic retail shareholder base greatly overestimating a market opportunity. At the same time, in the next several months a critically important binary event is due – the FDA will decide if CorMedix can file an NDA based on one rather than two Phase 3 trials. If the agency denies this request, we think the downside could be massive with shares trading down to cash levels in the $1 to 2 range or 75-90% from current levels. However, even if the FDA decides in favor of the company, we still believe the stock is dangerously overvalued since the actual market for its product is much smaller than what CorMedix has been suggesting to investors.

Background: Catheter Related Infections and Neutrolin

CorMedix, incorporated in 2006, is a pharmaceutical company developing therapeutic products primarily using taurolidine, an anti-microbial first synthesized by Geistlich Pharma in 1972 and studied as an anti-infective in the decades since. The company’s lead product is Neutrolin for the treatment of catheter-related blood stream infections (CRBSI).

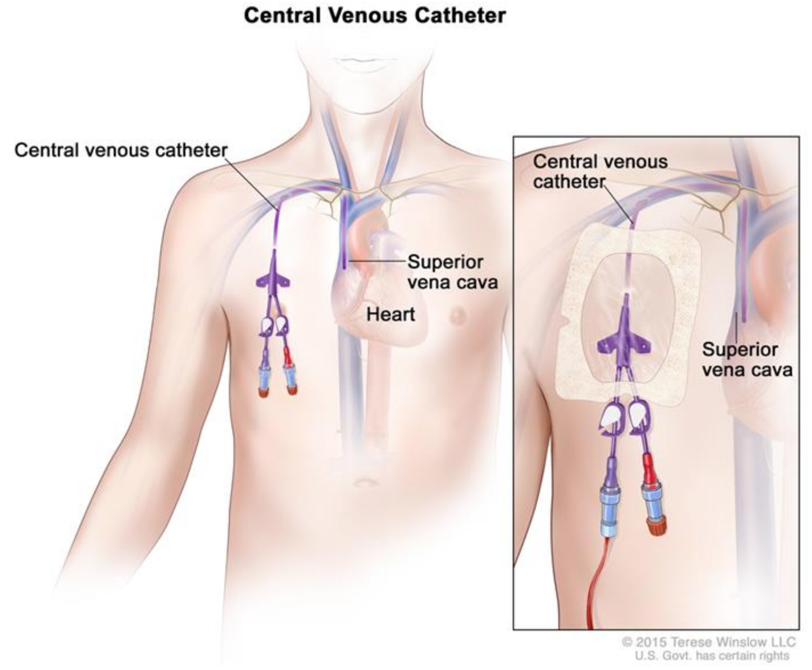

Central venous catheters (“CVC”) can provide infection-causing pathogens an entry point into the body (Figure 1). Antimicrobial lock therapies (“ALT”), usually containing an antimicrobial and an anticoagulant, were developed in the 1980s to treat CRBSI. When a catheter is not in use, ALT is injected into the catheter lumen and allowed to dwell, hopefully eliminating infection-causing pathogens.

Figure 1.

Source: cancer.gov

Neutrolin is an ALT consisting of taurolidine, the anticoagulant heparin, and sodium citrate as a pH buffer. Current standard of care focuses on preventing catheter occlusion using saline flushes or heparin locks. ALT is generally only recommended as a preventative therapy in specific cases based on patient condition and infection history.

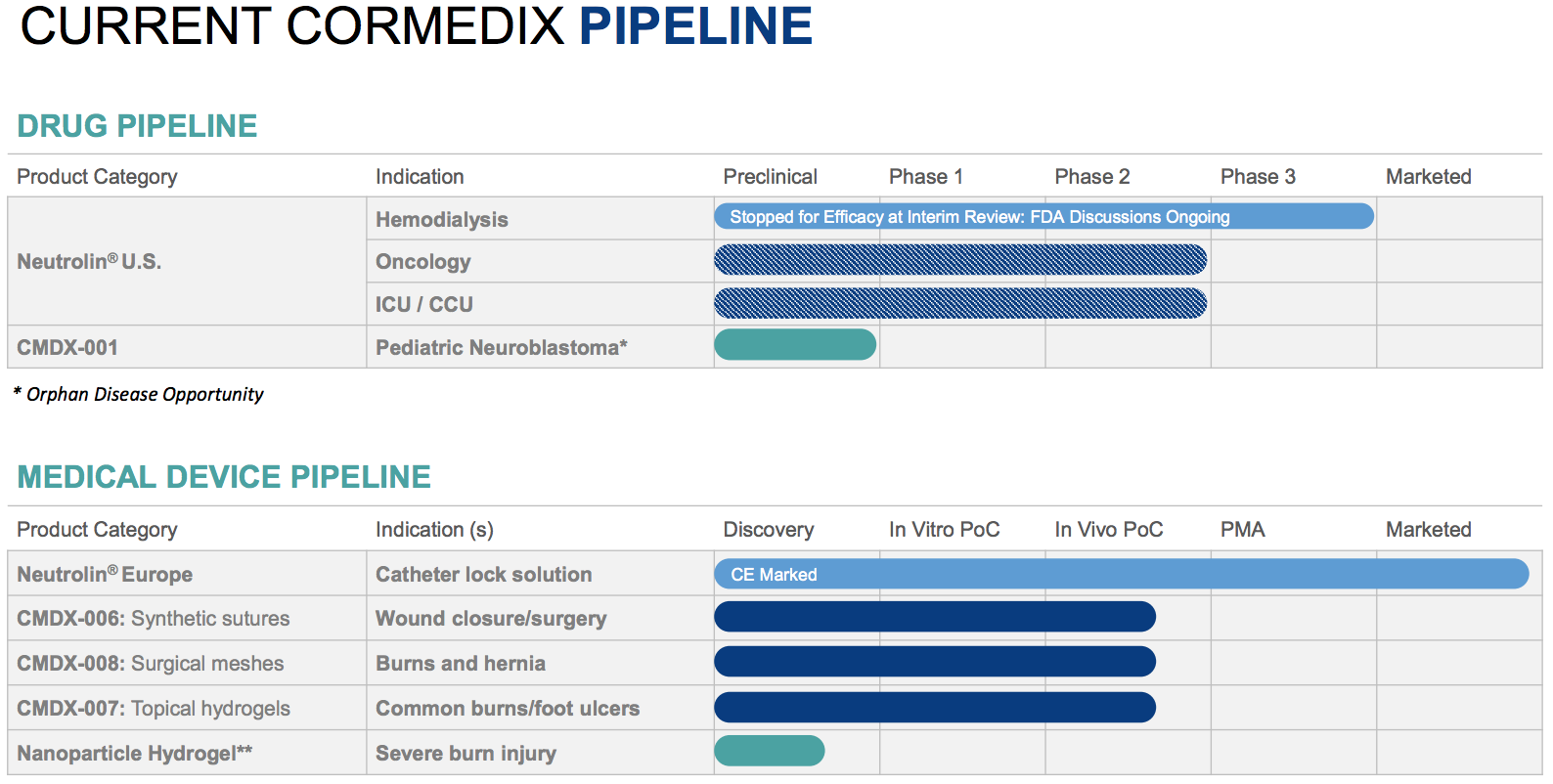

Neutrolin is currently for sale in Europe/Middle East and in Phase 3 development in the US. It is the only drug or device candidate CorMedix has in clinical development (Figure 2). The company lists several other applications for taurolidine, but all are pre-clinical. In fact, the company hasn’t had anything other than Neutrolin in the clinic since 2011.

Figure 2. CorMedix has nothing else in clinic

Source: Company presentation

Commercial Failure in Europe and Middle East

Initially, CorMedix attempted to develop Neutrolin as a medical device in the US since the regulatory hurdles for devices are significantly lower and less costly relative to those for drugs. However, in 2011 the FDA classified Neutrolin as a drug, later informing the company that two Phase 3 trials would be required for approval as is standard for new molecular entities. With only $2mn on its balance sheet at the end of 2012, CorMedix decided to look for partnering opportunities in the US and focus on commercializing Neutrolin in Europe where it was approved as a device. Management estimated Neutrolin’s market opportunity at $500mn, evenly split between the US and Europe.

In 2013, CorMedix began selling Neutrolin in Germany for hemodialysis patients with CVCs. By 2016 it was also registered for sale in France, Austria, Italy, Malta, Saudi Arabia, Bahrain, Qatar, Kuwait, United Arab Emirates, and The Netherlands. CorMedix eventually received additional approval for the oncology, intensive care, and parenteral nutrition indications.

Despite an abysmal launch ($52k sales in first full two quarters), management remained outwardly optimistic and continued to sell investors on the idea that there was a substantial European market for Neutrolin:

…with the current cash, we believe we’ll be able to get to profitability based on European operations…

– CFO Steven Lefkowitz, April 2014

The response, which is seen in the number of patients being placed on Neutrolin is encouraging. I will say we are continuing to gain traction in the hemodialysis market place… hemodialysis is less than 50% of the total market. So, the label expansion opens us a larger opportunity for CorMedix…

– CEO Randy Milby, May 2014

We are not satisfied with our sales revenue and commercial progress in Germany. What we’ve done is we’re making some changes in our personnel on the ground and the other aspect of this — I just want reiterate for everyone on the call, you recall that right now the label that we have is for hemodialysis only. So this label expansion which allows us to go into the oncology ICU, CCU total parenteral nutrition will give us a lot more rep when we call on positions in Germany.

– Milby, Nov 2014

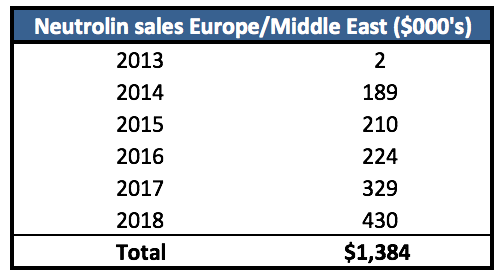

After a first full year of sales of only $189k, perhaps management realized Neutrolin’s market opportunity was tiny. In 2015, Evercore was hired to explore strategic alternatives (i.e. find a buyer). Throughout this process it couldn’t have helped that sales in Europe and the new territory of the Middle East continued to be anemic – 2015 revenues totaled only $210k – so it wasn’t surprising when Evercore was unable to find a buyer or even a partnership. Sales have only marginally improved since: last year revenues totaled less than $430k – five years after being on the market.

Figure 3. Neutrolin revenues: “disappointing” would be understatement

Source: Filings

Nearly Identical Product Also a Dud

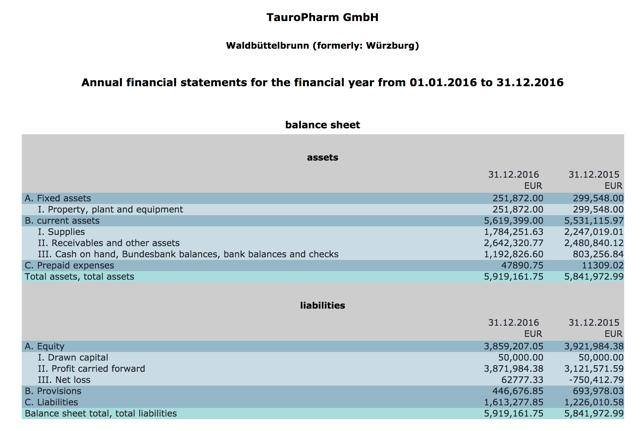

Over the years CorMedix blamed numerous factors for the weak sales: personnel, lack of a partnership, narrow label, and competition. CorMedix has several competitors in Europe, but the one most often cited by the company is TauroPharm GmbH which markets several different versions of taurolidine-based locks. TauroLock-Hep 100 and 500 are essentially the same product as Neutrolin with slightly different quantities of Heparin. In fact, the products are so similar that beginning in 2014 CorMedix filed numerous patent infringement claims against TauroPharm, although none have resulted in any action taken against the company with the last complaint dismissed in December 2018.

TauroPharm is private so revenue figures are not disclosed but Seeking Alpha contributor The Pump Stopper pulled available German corporate records through 2013 which suggested a business generating $1-2mn in revenues. We looked at the years since and not surprisingly the business appears to be of roughly the same size, having only generated cumulative (not annual) earnings of only $4mn (Figure 4) through 2016. Consider that TauroPharm had been in business for 12 years, marketing its near copy of Neutrolin under a wide label (dialysis, oncology, intensive care, and parenteral nutrition) and was in 28 countries as of 2015.

Figure 4. TauroPharm balance sheet

Source: German corporate records

Despite what is likely a low single-digit million revenue per year business, when questioned on the size of TauroPharm sales, CorMedix management has allowed rumors to persist of a substantially larger business generating upwards of $40mn annually which would be even higher if not for TauroPharm artificially depressing prices.

As recently as January, management was still blaming competition for weak sales in Europe. During the January 14 topline data investor call, in response to a question on why US demand should be different from Europe/Middle East, Consultant Advisor CMO Paul Chew responded:

There is no [approved] product in the US, unlike Europe where there are many products of various kinds.”

However, if the European opportunity for CRBSI prophylactic locks was so attractive, why hasn’t a larger pharmaceutical already bought TauroPharm or entered the market themselves? 3M (NYSE:MMM) markets disinfectant catheter caps and dressings, but they have yet to offer an antimicrobial catheter lock. Why is that? We suspect it’s because they and others view the market as unattractive.

Neutrolin Will Also Fail in US

We have no reason to believe the US market will be significantly different from Europe. The issue of CRBSI and its effects on morbidity and health care costs have been widely recognized and studied among health experts here, and antimicrobial catheter locks have been used for decades. Taurolidine locks have been studied since the 1990s. Studies have consistently shown that ALTs reduce infection risk by upwards of 70 to 90%.

So why haven’t they become standard of care? We believe it’s primarily due to the medical community’s preference for good hygienic fundamentals and catheter technique, leaving antibiotics and antimicrobials as an option in case all else fails or as treatment option after infection is diagnosed. CDC guidelines only recommend lock prophylaxis for especially vulnerable patients with a history of infection despite optimal maximal adherence to aseptic technique. The following sentence best summarizes the general outlook of health agencies on catheter lock therapy:

Although most studies indicate a beneficial effect of the antimicrobial flush or lock solution in terms of prevention of catheter-related infection, this must be balanced by the potential for side effects, toxicity, allergic reactions, or emergence of resistance associated with the antimicrobial agent.

– CDC Guidelines for the Prevention of Catheter Related Infections, 2011

The added cost of ALT is also a factor since solid aseptic practice such as washing hands and skin antisepsis is essentially cost-free. In a critique of a study (Winnicki, Herkner, Lorenz, et al., 2018) promoting taurolidine-based catheter locks, Labriola and Jadoul highlighted the fact that strong catheter care protocols can achieve infection rates as low as those shown in the treatment arms of ALT studies:

In conclusion, strict respect for hygiene protocols for catheter care is the cornerstone for the prevention of CRBSI. Given the available evidence, the optimal composition of catheter lock solutions remains a matter of debate.

– Labriola, 2018

If the market opportunity was attractive in the US, surely at least one of the approved European locks would’ve begun development here. There’s also Zuragen manufactured by US-based AAT. Zuragen is an non-antibiotic antimicrobial lock that completed a Phase 3 vs. heparin in 2010, reducing infections rates by 69% and outperforming control on maintaining catheter patency (flow). Due to a conflict with the FDA on how AAT calculated CRBSIs, the compound was shelved. Given that AAT has been dormant due to lack of funding, Zuragen could probably be acquired for very little, so again if the US market was promising, why hasn’t anyone shown interest in developing Zuragen or any of the currently marketed European ALTs?

Saved by 2015 Biotech Rally

While Neutrolin was floundering in Europe, CorMedix was engaged in what turned out to be a fruitless evaluation of strategic alternatives. Then the huge US biotech sector rally of 2015 happened. CorMedix, which had never filed a 10-K listing more than $5mn in cash, was able to raise $42mn via a combination of warrant exercises and it’s at-the-market sales program. This unexpected cash infusion allowed CorMedix to begin enrolling the first-ever randomized trial for Neutrolin, a Phase 3 named LOCK-IT 100 in hemodialysis patients in late 2015.

Subject enrollment was targeted at approximately 630 patients with an interim safety analysis after 81 CRBSI events which management estimated would occur roughly seven months after enrollment started with the whole trial taking one year to complete. Delays hampered LOCK-IT 100 almost from its beginning. Management cited reasons including underperforming clinical sites, and patients being excluded due to recent antibiotic use. In 2017, CorMedix disclosed a very significant issue – CRBSI events were occurring at a much lower rate than expected.

The company and the FDA agreed to several changes in the trial design with the goal of enhancing CRBSI detection: the use of a committee to assess suspected CRBSIs, only one positive blood culture necessary instead of two, and closer evaluation of cases presenting outside of dialysis centers. The agency also allowed an interim analysis triggered by the first 28 events.

In July 2018 CorMedix announced a DSMB conducted the interim analysis and recommended trial termination due to efficacy. As a result, CorMedix said it would request a meeting with FDA and seek permission to file an NDA based on LOCK-IT 100 (recall FDA was requiring two Phase 3 trials).

Rebuffed by FDA

CEO Khoso Baluch was notably optimistic going into the meeting in the 3Q18 earnings release:

…we are simultaneously preparing to file an NDA with the Food and Drug Administration for Neutrolin in anticipation of receiving a favorable response from the FDA at our upcoming meeting to discuss Neutrolin’s development path.”

The company met with the FDA in the week or so prior to when it published its topline data press release on January 30. On February 14 CorMedix issued a press release on the meeting outcome, and Baluch’s tone shifted:

We believe our meeting with the FDA was very productive and we look forward to continuing discussions with them on whether LOCK-IT-100 is adequate to support the NDA submission. We understand FDA’s desire to assess the full data set. We will continue to pursue our goal of filing the NDA based on the single study, and appreciate the guidance received from the FDA.”

It’s surprising to us that CorMedix believed FDA would even consider allowing them to file before seeing the full data set. It’s also puzzling that management would submit a meeting request and prepare its case for Neutrolin based on data it supposedly didn’t have. Management repeatedly mentioned that it remained blinded to the data until just before it issued an interim data press release on January 17, yet it requested an FDA meeting and prepared the meeting package before mid-November. Here’s Baluch during the Q3 earnings call:

It was very important for us in this situation that we focused the company’s effort on creating a high quality and comprehensive submission to ensure that the company is presenting robust data and the most persuasive arguments to commercialize Neutrolin in the U.S. expeditiously.

If it remained blinded to the data, the only information management had was that the DSMB recommended trial termination due to efficacy and there were no safety concerns that led them to recommend trial stoppage. How could they adequately prepare a case with only this information? The company claims that independent consultants put together the data package, but if so we find it hard to imagine how management would prepare for such a meeting.

Phase 3 Data: Concerning Unknowns

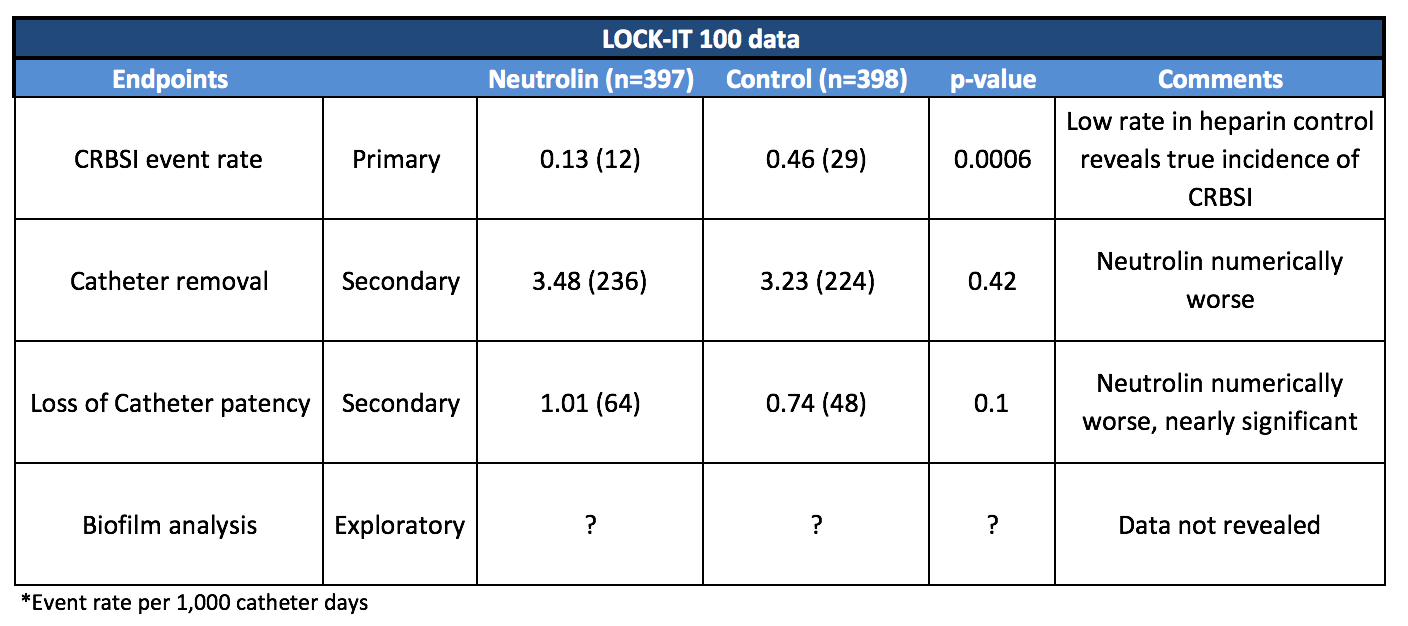

Top-line data on the interim and full populations were not disclosed until January 30, six months after the DSMB recommendation. The company said this was due to the large and complicated task of shutting down clinical sites and cleaning the data set. Below are the results:

Figure 5. LOCK-IT 100 numerically worse on secondaries, no biofilm data

Source: Corporate presentation

This is the extent of the LOCK-IT 100 data released. CorMedix hasn’t even shared patient baseline characteristics. In our view that in itself is worrying, but there are several unknowns and potential inconsistencies that should also concern investors. During the 1Q19 earnings call, Liz Masson, Head of Clinical Operations, noted that FDA wanted additional analyses on the full data including baseline characteristics (age, location of catheter, co-morbidities, etc.), any trends or contributing factors that led to CRBSI, pathogens leading to infection and adverse event detail.

If the FDA is actually considering allowing an NDA, we believe they will be extra careful in examining the data given the relatively small number of events (41) compared to the original protocol as well as the fact that CRBSI were determined by a committee and in some cases added after re-examination of patient records. The agency might want to make sure the committee was properly adjudicating CRBSI events.

The FDA will also want to examine the types of pathogens causing infections to determine efficacy more robustly. Consider that Taurolidine-based locks have shown mixed efficacy against gram-positive organisms. Since CorMedix hasn’t released anything but the most basic topline numbers, we don’t know if Neutrolin showed any efficacy against gram-positive bacterium. Or perhaps another pathogen caused the majority of infections in the Neutrolin arm. The following is from Labriola’s critique of the taurolidine study results mentioned earlier:

… in the trial by Winnicki et al. the CRB decrease was due to a significant reduction in CRB caused by Gram-negative microorganisms, as already reported, despite the fact that CRB is usually caused mostly by skin microorganisms (Staphylococcus and Streptococcus spp.). This limits the generalizability of the claimed benefit of the use of taurolidine-based regimens in hemodialysis units.”

In addition, we imagine the agency will want to know why Neutrolin was numerically worse on both secondary endpoints: removal of catheter for any reason and loss of catheter patency. Both of these measures are important not only in terms of patient safety but also from a cost-benefit perspective. (Though cost isn’t a direct concern for FDA in terms of determining regulatory path, we note that Cathflo Activase, a treatment to restore catheter patency, lists for $170/dose. Investors may dismiss this amount relative to hospital re-admission costs often cited by manufacturers of catheter locks, but given the current low rates of CRBSI occurrence in the hemodialysis population, every marginal dollar is significant.)

Also concerning is that CorMedix hasn’t revealed any information on the study’s exploratory endpoint: biofilm analysis on the first 200 catheters removed. Biofilm refers to matrices of bacteria present on surfaces such as catheter lumens. Biofilm protects bacteria from antimicrobials and thus is a focus of infection control research. CorMedix likes to include slides in its corporate presentations claiming Neutrolin is effective in preventing it, so the lack of disclosure here is worrying.

We asked the company why they haven’t released any biofilm data and were told the analysis is ongoing. We find this excuse hard to believe since 200 catheters would’ve been removed no later than mid-2017. If this data was positive or even neutral, we suspect it would’ve been shared by now.

We also note the very low rates of infection in the control arm. Compare this to what CorMedix curiously cites as the proper benchmark of 3.5/1000 days in its latest corporate presentation dated March 2019.

Figure 6. Corporate presentations overstate infection rates

Source: Corporate presentation

CorMedix Likely Sold ATM Shares After FDA Guidance

We are skeptical of small-cap biotech management by nature, but we found the change in Baluch’s tone before and after the FDA meeting to be noteworthy. Going in he was anticipating clearance to file, but afterward, he only noted the meeting was “productive” and that he “looked forward to continuing discussions” and “appreciated the guidance”.

This vague language reminds us of how Ampio Pharmaceuticals (AMPE) communicated its interactions with the agency as it haplessly tried to convince them to allow a BLA filing. For example see the press releases here, here, and here. In reality, the discussions were far more negative than portrayed by Ampio but since the meeting minutes were never made public, many investors were caught off guard. When Ampio finally had no choice but to admit talks with the FDA failed, the stock corrected 85% in two days. We fear CorMedix might be a similar case.

We also highlight the actions CorMedix management likely took after meeting with FDA. This year through March 8, the company sold 1.8mn shares (split-adjusted) at an average price of $8.90. We believe most were sold after the meeting since the 10-day moving average didn’t hit $9 until February and recall the meeting took place before January 30. If CorMedix felt confident the agency would allow them to file based on a single trial, why were they selling so many shares after the meeting?

Tough Competition

There are many treatment options to effectively address CRBSI in hemodialysis settings including antibiotic locks, anti-infective dressings, coated catheters, etc. While there is no approved ALT, hospitals routinely produce their own lock solutions. Emergence of resistance may be a concern, but recall CDC guidelines note in certain cases they make sense. And as previously discussed, stringent catheter protocol can be just as effective as lock solutions – and less costly.

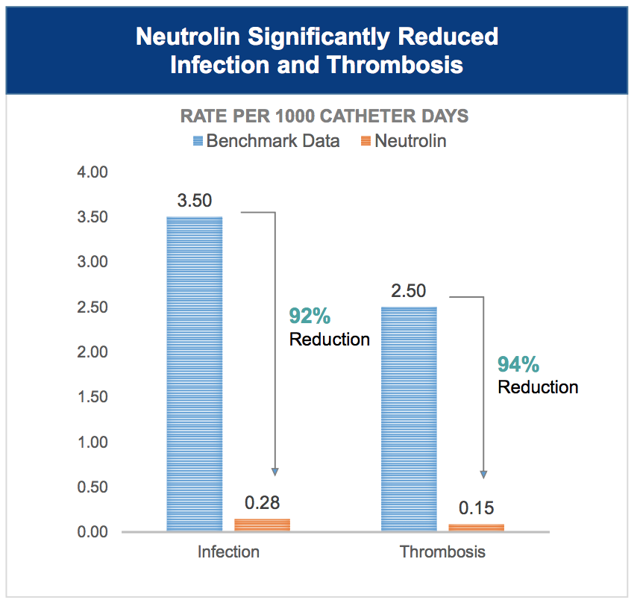

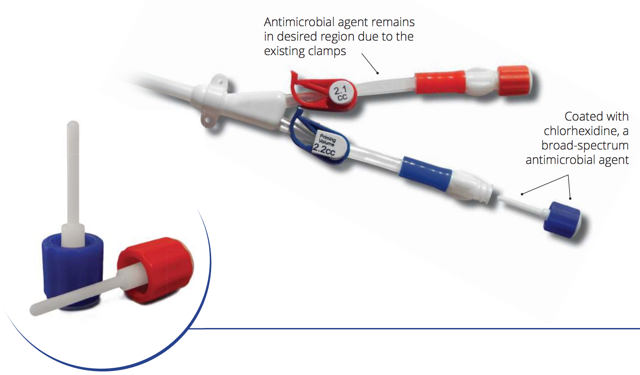

Also worrisome for CorMedix is a relatively new device called ClearGuard HD (Figure 7) which has evidently gained some traction among dialysis providers. The surfaces of conventional catheter caps are typically coated with a disinfectant such as isopropyl alcohol. Manufactured by Pursuit Vascular, ClearGuard HD caps feature rods coated with the antimicrobial chlorhexidine which is activated when inserted into liquid-filled catheter hubs. Although chlorhexidine is proven safe (it’s used in mouthwash), once released it remains in catheter hubs due to the catheter’s existing clamps thus limiting a patient’s potential exposure to active ingredient compared to catheter locks.

Figure 7. ClearGuard HD Caps

Source: Pursuit Vascular presentation

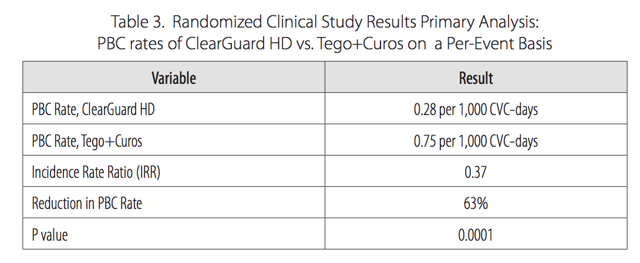

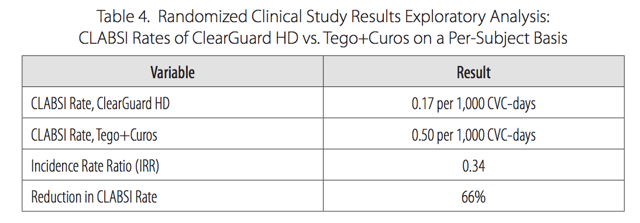

Pursuit Vascular conducted a 13-month, prospective, unblinded clinical study at 40 dialysis centers in the US comparing ClearGuard HD against current standard of care caps. Among 1,671 patients, ClearGuard HD reduced the rates of any positive blood culture and central line associated BSI by 63% and 66% respectively. Among patients who entered the study with a new CVC, infection rates were lowered by 72%. We note that both of these endpoints are more broad measures of infection than strict CRBSI. We also highlight the very low rates of infection in the control arm, equal to what was seen in LOCK-IT 100 and again far below what CorMedix claims to be benchmark rates of 3.5/1000.

Figure 8.

Source: Pursuit Vascular presentation

Figure 9.

Source: Pursuit Vascular presentation

Pursuit Vascular is private so pricing and revenue information aren’t available, but we suspect the caps are priced competitively with current caps. We found the caps used as control in Pursuit’s study (Curos and Tego) available online for around $10, though alternatives are available for half the price. The price of Neutrolin in Europe is roughly $18 per dose.

This simple cap targets the catheter entry point, clearing pathogens before they migrate into catheter lumens. It exposes patients to less potentially toxic antimicrobial solution and is likely cheaper given the relative amounts of active ingredient. We believe ClearGuard HD caps may obviate the need for prophylactic antimicrobial catheter locks such as Neutrolin.

Upcoming Binary and Valuation: Massive Downside

Recall that CorMedix is currently preparing analyses of the full data set for FDA review, as the agency decides whether or not an NDA can be filed based on a single Phase 3. During the March 14 Q4 earnings call, Baluch said the package submission will occur in “the next several weeks”. Type C meetings are scheduled within 75 days so if we estimate delivery to FDA in mid-April, a meeting should take place before the end of June after which the agency will send meeting minutes to CorMedix within 30 days. Of course, this assumes that a meeting will even be granted. It’s possible FDA simply denies the request within 21 days from receiving the company’s package. So the window to watch for developments is roughly May through July.

We believe CorMedix faces an uphill battle. We don’t believe CRBSI in hemodialysis is a significant unmet need, at least in the context of providing the impetus for FDA to ease its standards. Our reasoning is due to currently available treatments including ALT and ClearGuard HD, as well as the dramatic effect of simply instituting strong catheter protocol. Adding to the uncertainty is the lack of disclosure of the overall data – we don’t even have patient baseline characteristics from the interim analysis for instance. FDA will also question why Neutrolin was numerically worse on both secondary endpoints (nearly reaching significance in loss of catheter patency).

CorMedix bulls will point to the FDA’s recent encouragement of new anti-infective drug development and that taurolidine hasn’t shown any bacterial resistance to date. Both are true, but neither are exactly new. Recall studies have been done illustrating the efficacy of taurolidine locks since the 1990s. Also, the agency’s encouragement of anti-bacterial and anti-fungal drugs isn’t a completely new development. The Generating Antibiotic Incentives Now Act (“GAIN”) was passed in 2012, years before the FDA told CorMedix it would need two Phase 3 trials in order to file an NDA.

Bulls may also cite that FDA is letting CorMedix request consideration for approval under the LPAD (Limited Population Pathway for Antibacterial and Antifungal Drugs) pathway. However, we find it unlikely that Neutrolin for the prevention of CRBSI would qualify for LPAD. The pathway is meant for novel antimicrobials that target specific pathogens resistant to current therapies in a limited population. Limited in this context refers to a population refractory to current standard of care and/or with very limited or no effective therapies. Consider the labels of two drugs approved under LPAD, Arikayce, and ZEMDRI:

Arikayce for the treatment of lung disease caused by a group of bacteria, Mycobacterium avium complex in a limited population of patients with the disease who do not respond to conventional treatment (refractory disease).

ZEMDRI for adults with complicated urinary tract infections, including pyelonephritis, caused by certain Enterobacteriaceae in patients who have limited or no alternative treatment options.

CorMedix is positioning Neutrolin as the future standard of care catheter lock. What would be the “limited population”? Hemodialysis patients with CVCs? That seems inconsistent with the spirit of the regulation. Also, while no resistance to taurolidine has been detected, it hasn’t shown any particularly unique effectiveness over bacteria or fungi resistant to current therapies. The company includes a slide on its corporate presentations implying effectiveness against Candida auris, but no in vivo data has been presented to date.

In any case, LPAD is of little relevance to Neutrolin’s current regulatory situation. Requests for LPAD are filed in conjunction with an NDA. To our understanding, the pathway is not a tool that lowers the requirements necessary to file an acceptable NDA.

It’s also noteworthy that both Arikayce and ZEMDRI completed at least two randomized controlled trials. Arikayce was evaluated in a Phase 2 and a Phase 3 with an open-label extension study. Plazomicin was evaluated in six Phase 1, one Phase 2, and two Phase 3 studies. And unlike Neutrolin, both drugs were awarded Breakthrough Therapy Designation. Meanwhile, Neutrolin has only completed one randomized trial. In our view, the FDA was already lenient when it allowed CorMedix to go straight into Phase 3 – is it likely FDA further lowers its standards below what was expected of two BTD/LPAD drugs?

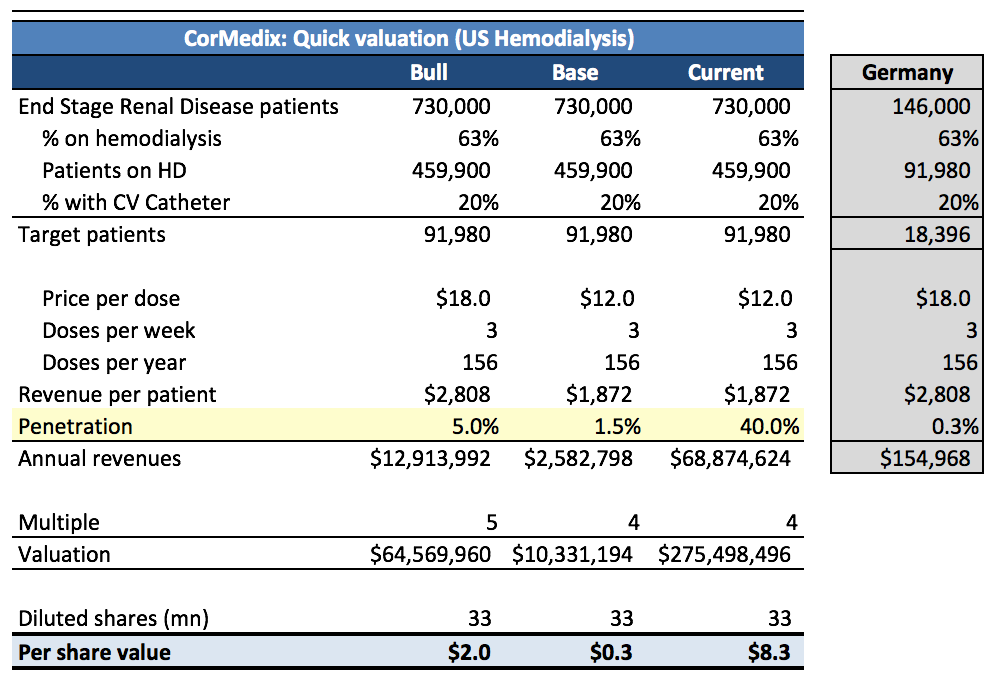

Figure 10. CorMedix Dangerously Overvalued

If we are correct and FDA denies CorMedix’s request, the company would have to run another trial which would take another 2-3 years to complete and obviously require significant additional financing and thus dilution. We estimate the company has around $25mn in net cash (our net cash estimate includes the just announced NOL sale of $5mn). With 33mn fully diluted shares outstanding, shares could trade down to $1.

If we are incorrect and FDA grants the company’s request, we still believe CorMedix is extremely overvalued. We performed a sanity check valuation (Figure 11) based on the aggressive assumptions that Neutrolin is approved in the US and performs >15x better than it has in Europe, based on an estimated penetration rate for Germany. We also applied an optimistic price and revenue multiple. Even with these very bullish assumptions, our quick calculation results in a value of only $2/share.

Apply more realistic assumptions ($12/dose, 2% penetration, 4x multiple) and the value is below $0.40/share. Moreover, the current share price of $8.40 implies a market penetration rate of roughly 40%. To top it off, we haven’t even considered the inevitable dilution since CorMedix would need cash to market Neutrolin.

Figure 11. Valuation

Source: United States Renal System Data; Dialysis care in Germany

Ownership and Analyst Coverage

Institutional ownership is roughly 15% of diluted shares. Most of this is Elliot Management who own around 3mn shares or 10%. Next are Vanguard and BlackRock at around 2% each but neither of these managers are stock pickers and likely own shares for index tracking purposes. The rest of the owners hold relative odd lots. Elliot has been in the stock since the 2010 IPO. We’re not sure why they’ve stuck with it for so long, but the position makes up less than 0.1% of their AUM. Only two sell-side firms cover CorMedix: H.C. Wainwright and ROTH Capital.

Investors should wonder why institutional ownership is so low and why more analysts don’t cover the company. Neutrolin has been on the market and post-marketing efficacy data has been available for years. It’s been nine months since the Phase 3 termination news. The story is old and well known yet the “smart money” remains uninterested.

Avoid The Stock or Establish Short

Despite the upcoming binary and risks we have discussed, the company’s valuation is near all-time highs as shares have rallied while management has tripled the diluted share count in the last two years. If the company has to run another Phase 3, shares could correct up to 90%. And while we don’t think it’s probable, even if the FDA permits CorMedix to file based on a single Phase 3, the current market capitalization of $280mn is difficult to justify given Neutrolin’s horrid sales in Europe and the competitive alternatives to lower CRBSI rates in the US.

We would become less bearish on the stock if Neutrolin was eventually approved for hemodialysis and achieved market penetration rates above what we expect (Figure 11). Approvals in other indications such as oncology and total parental nutrition with correspondingly strong commercial traction would also make us reconsider our view.

We strongly recommend investor caution at these levels or initiating a short position (Interactive Brokers currently shows 150k shares available to short at borrow rates around 26%). Due to the outsized risks to the downside we have discussed and the limited upside, we think establishing a short position at current levels offers attractive risk/reward.

{kind=link}

{kind=link}