- FCEL appears to have lost two of its largest generation contract awards valued at approximately $636mn of future revenue and equivalent to ~100% of its current operating portfolio

- The losses are undisclosed. Instead management has represented that the awards are nearing power purchase agreements

- In our view this is likely a breach of disclosure requirements governing material information, potentially jeopardizing last week’s stock offering

- Even without this evidence, we find FCEL’s premium valuation impossible to justify in the context of its struggling business and debt heavy balance sheet

- We value FCEL no higher than 1.7x EV/Sales on 2022E numbers or $0.70/share

FuelCell Energy (NASDAQ: FCEL) is a manufacturer of stationary fuel cell power plants for distributed power generation. FCEL’s weak fundamental picture has been well documented by analysts on the sell-side and Seeking Alpha. This report focuses on previously uncovered evidence which indicates FCEL lost two large project awards this year but failed to make appropriate disclosures to investors. This is concerning in a general sense given what it signals about management’s transparency, but more immediately we question how such non-disclosures affect last week’s 50mn share follow-on offering.

Loss of Significant Contract Awards Undisclosed

FuelCell Energy won three significant contracts awards from PSEG Long Island in 2017 with 39.8 megawatts (MW) of capacity worth up to $800mn of future revenue potential over the life of the projects under PSEG’s Fuel Cell Resource Feed-in Tariff (FIT IV) program. These wins were and are extremely significant to FCEL. To provide context, its backlog of contracted projects at the time was 107MW and worth $437mn. The company’s current backlog is valued at $1.1bn with total project capacity of 40.6MW.

Figure 1. FCEL disclosed backlog and awards as of 3Q 2019

Source: Company filing

The three PSEG contracts are referred to as LIPA1 (Yaphank, 7.4MW), LIPA 2 (Brookhaven Rail Terminal, 18.5MW) and LIPA 3 (Yaphank Industrial Park, 13.9MW).

Since 2017 FCEL has touted these wins as validation of the company’s carbonate fuel cell technology and management’s ability to execute in the clean energy sector. FCEL secured a power purchase agreement (PPA) for LIPA 1 in 1Q19 and the project moved into the company’s official backlog. However, we found that LIPA 2 and LIPA 3, which represented approximately $636mn in future revenue and are equivalent to 80% of current backlog and 100% of current operating assets, were cancelled earlier this year. FCEL has not only failed to disclose this, it has for months represented that the contracts were simply going through the approval process.

New York Climate Regulations Adopted in 2020 Exclude FuelCell

In July 2019, New York state enacted the Climate Leadership and Community Protection Act (CLCPA), an ambitious and comprehensive set of clean energy legislation. The act modified what NY considered eligible “renewable energy systems” for its clean energy procurement initiatives. Prior to CLCPA, all fuel cell technologies were considered “renewable energy” regardless of how they were powered. FCEL won the three LIPA projects under this structure.

The CLCPA changed procurement guidelines by among other things excluding fuel cells powered by fossil fuel resources – including natural gas which powers FCEL’s carbonate fuel cells. From the bill text:

..”renewable energy systems” means systems that generate electricity or thermal energy through use of the following technologies: solar thermal, photovoltaics, on land and offshore wind, hydroelectric, geothermal electric, geothermal ground source heat, tidal energy, wave energy, ocean thermal, and fuel cells which do not utilize a fossil fuel resource in the process of generating electricity.

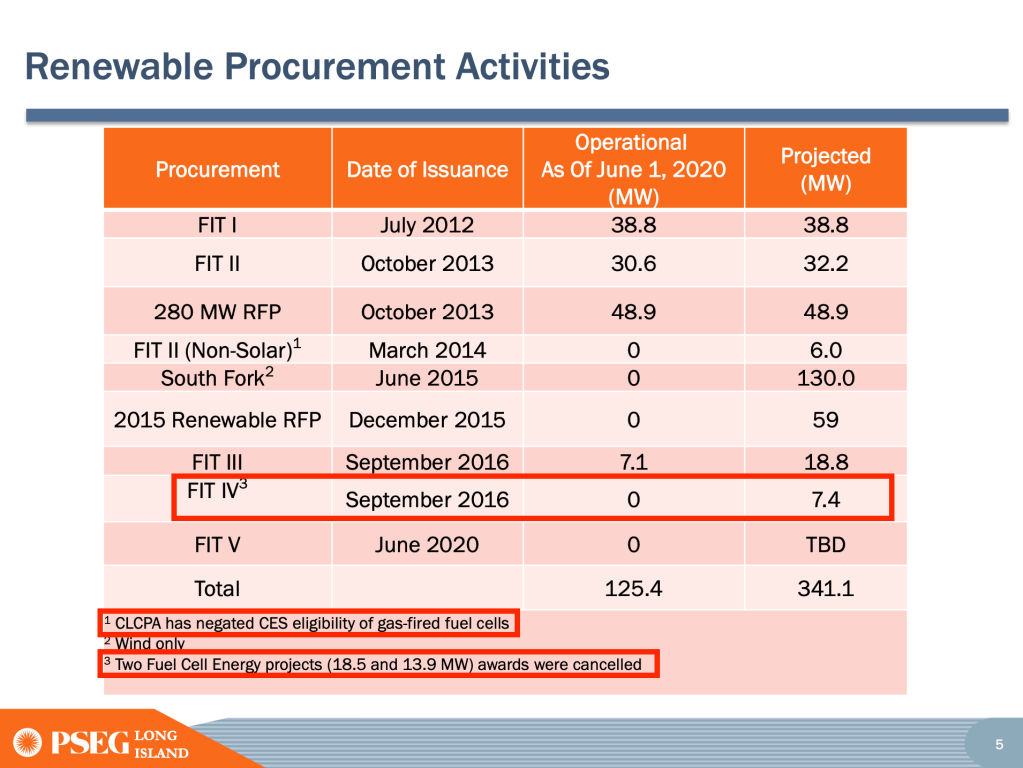

Below is a slide from PSEG’s annual report on resource planning and renewable energy published in July 2019. Under the FIT IV procurement program, all 39.8MW of the three LIPA projects is listed, even though a footnote mentions that CLCPA may change the eligibility of gas-fired fuel cells:

Figure 2: PSEG Long Island slide from 2019

Source: lipower.org

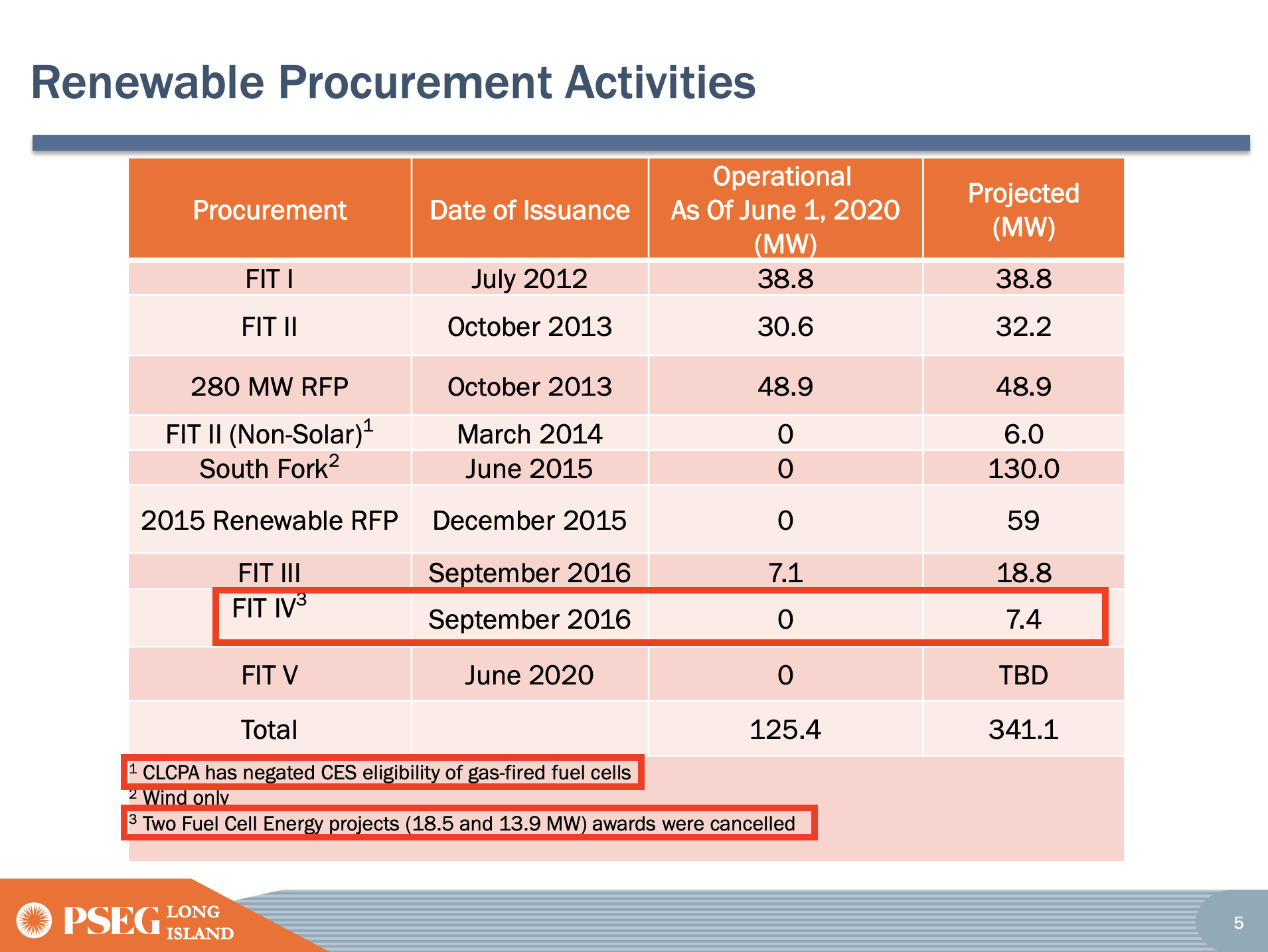

Note the change in the same slide one year later from July 2020 below. Only the LIPA 1 (7.4MW Yaphank) project of FIT IV procurement remains. From the footnotes: “CLCPA has negated eligibility of gas-fired fuel cells” and “Two Fuel Cell Energy projects (18.5MW and 13.9MW) awards were cancelled”.

Figure 3: PSEG Long Island slide from 2020

Source: lipower.org

FuelCell Fails to Disclose Award Cancellations, Paints Them as Active

FCEL would have been aware of the relevant sections in CLCPA during 2019 when the act was being considered. We know that FCEL submitted comments to the New York Public Service Commission in October 2019 in an attempt to save the LIPA projects.

FCEL has never mentioned the CLCPA in any of its filings. Before the act became official regulation on January 1 of this year, management repeatedly failed to disclose the potential effect of any changes due to CLCPA on the LIPA awards. And after the act’s effective date, when asked for updates (over three years now without signed PPAs) management told analysts and investors the projects were simply in the approval process. Below are comments from FuelCell’s CEO and CFO on quarterly earnings calls. Note that all occurred after CLCPA became effective:

Q4 2019 earnings call – Jan 22, 2020

CEO Jason Few:

The one thing that you noticed or noted in the backlog is we’ve made a decision that we’re going to talk about backlog for projects that we have signed PPAs. The other two LIPA projects as PPAs aren’t signed, they are still in ISO. So, those are things that we continue to work on but great progress to-date on Yaphank.

Q1 2020 earnings call – Mar 16, 2020

Analyst:

Okay, that’s helpful. And then, speaking of the LIPA projects; can you just give us an update if there is one on the two other projects that I don’t think have signed PPAs but you have been awarded in the past?

CEO Jason Few:

Yes. As you know, we’ve — those two products do not have signed PPAs yet. We continue to work with LIPA to try to advance those projects but have not signed PPAs as of yet.

Q3 2020 earnings call – Sep 10, 2020

Analyst:

Got it and then on the two LIPA projects you are still working on. I mean, I would assume those are still progressing. Any thoughts on timing or is it still more just going to get through the process, interconnect, etcetera?

CFO Michael Bishop:

Yeah, Eric it’s more get through the process, our Yaphank project we are well into that process for that project and expect that — and we’re making good progress there. But we’re going through interconnects and all the things that you have to do and those things take time.

As a result of the non-disclosure and disinformation, sell-side analysts consider LIPA 2 and 3 still in play as evidenced by the most recent notes from Craig Hallum and Cowen from September 10.

Failure to Disclose Material Info May Force Re-pricing of Last Week’s Secondary

If what we have identified is in fact the loss of major contract awards which FCEL has not disclosed for the past nine months, that in itself is concerning for what it signals about management transparency. But equally important for shareholders is what the implications are for last week’s 50mn share follow-on offering run by J.P Morgan, Barclays, Canaccord Genuity and Loop Capital. Neither the LIPA contract cancellations nor CLCPA were mentioned in the prospectus.

In our view the non-disclosures could force a cancellation or re-pricing of last week’s secondary. Buyers of the offering are relying on information provided by management, including commentary from quarterly conference calls. Investors currently believe the LIPA projects are going through the approval process.

An example of an equity offering amended due to undisclosed material information can be found in Namaste Technologies (OTC: NXTTF). Namaste engaged in a $45mn offering on September 26, 2018. On October 4, 2018, Citron Research research published a report alleging among other things an undisclosed related party transaction. Namaste denied the allegations, but nonetheless amended the deal terms by increasing the number of warrants by 50%, lowering their exercise price by 10% and extending their expiration by one year.

The non-disclosure of what we believe is material and highly significant information frankly surprised us – the information is easy to find and clear-cut. Also surprising was a lack of discussion from the sell-side throughout 2019 and 2020 regarding implications of CLCPA on FCEL’s business. We sent multiple emails to FCEL investor relations with our findings, including the PSEG slide from 2020 and asked for comment. We also asked for the actual status of the LIPA awards. We have yet to hear back.

FuelCell Was Already Fundamentally Challenged

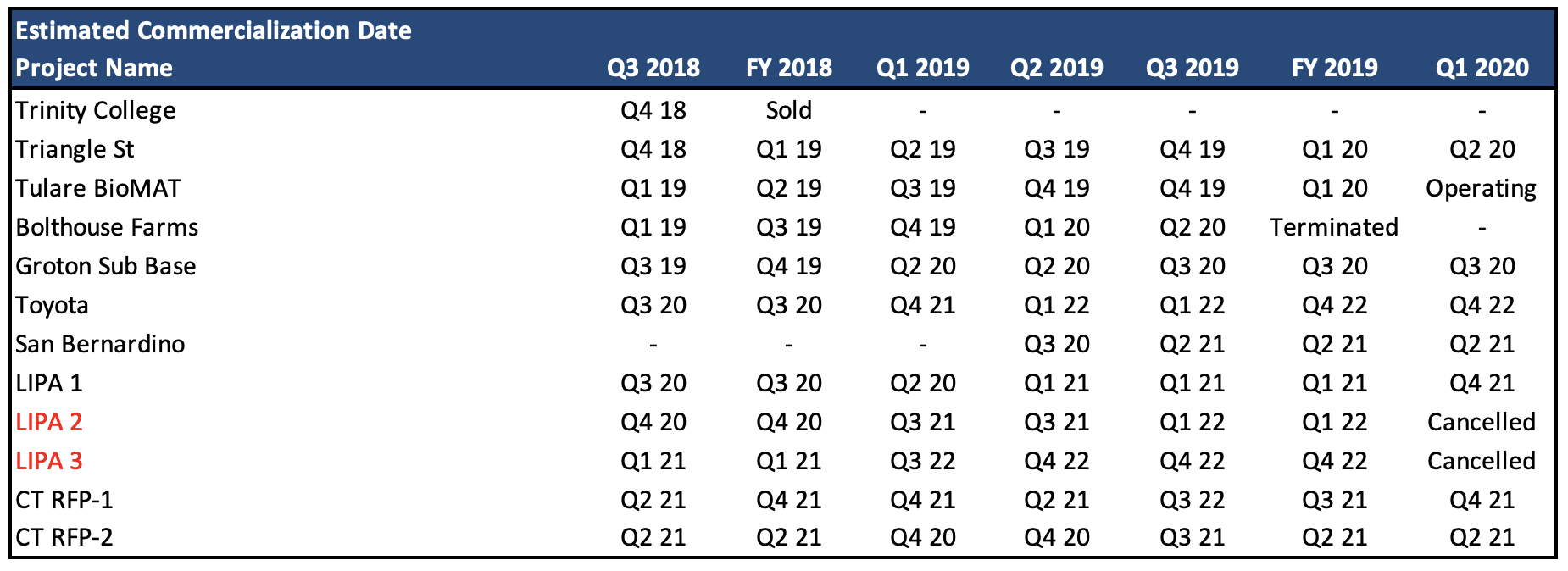

FCEL has guided to EBITDA positive by 2022 which is reflected in the consensus estimate of $8.7mn. From what we’ve seen, investors have anchored on this target – it’s the most often discussed big picture item on conference calls and in analyst notes. We’d advise caution here in light of what we suspect on the LIPA projects as well as an established history of project delays (Figure 4). For instance, while FCEL managed to complete the PPA for LIPA 1, its operation date has been pushed back several times, most recently from 1Q21 to 4Q21.

Figure 4. History of Project Delays

Source: Management comments, company filings (*cancellations based on our findings)

In addition, the disclosure issues perhaps shed new color on FCEL’s troubled relationship with South Korea-based POSCO. Once considered a huge opportunity for FCEL in one of the largest fuel cell markets in the world, the relationship was essentially terminated this year and has devolved into lawsuits and both parties requesting arbitration. FCEL is now starting from square one in Asia, a critical clean energy opportunity and in our view a market in which the stock is pricing-in some degree of success.

Overvalued Even Before Potential Disclosure Issues

FuelCell trades at a significant premium to Bloom Energy (NYSE: BE) – roughly 2.5x better on an EV/Revenue basis. This despite Bloom showing better margins, profitability and growth (Figure 5). Considering FCEL’s troubled fundamental picture – massive continual dilution, large amount of onerous debt, history of project delays, contractual disputes in Asia, thin margins resulting in consistent losses – the story of such a company trading at a premium valuation is absurd in our opinion. In our view, based on its known fundamental picture, FCEL should trade at a ~30% discount to BE or 1.7x EV/Sales multiple on 2022E sales, equating to $0.70/share or 70% lower from current levels.

Figure 5. FuelCell Compared to Bloom Energy

However, if what we have found is in fact the cancellation of two large contract awards and the failure of management to communicate this properly to investors, we believe the issues for FCEL will start at the re-pricing of last week’s secondary and go beyond there. FuelCell management should be transparent with investors and disclose the full status of the LIPA projects.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}