- Previously we revealed FuelCell lost two large project awards yet not only failed to disclose the fact to investors, but continued to represent the projects as active

- Through a FOIA request we obtained records which show a continued lack of transparency

- Documents show FuelCell had known for 15 months that LIPA had no intention of signing contracts due to new regulations and projections of reduced demand growth in the region

- Yet FuelCell portrayed the awards as ongoing while it sold over $180m worth of stock in six separate issuances

- FCEL’s enterprise value of $7.2bn or 80x 2021E revenue assumes pristine management credibility and execution. We believe investors should discount current backlog and future project assumptions.

FuelCell Energy (NASDAQ: FCEL) lost two large power project awards in 2019 with the Long Island Power Authority (LIPA) but never disclosed this to investors. Despite learning of LIPA’s decision, management continued to cite the awards in filings and conference calls as significant business that would soon enter official backlog. After we published evidence of the award losses, FuelCell responded by claiming our report was “misleading” but failed to mention a single inaccuracy. And only after our report did FuelCell begin disclosing the possibility of the project cancellations.

We have new evidence which proves that management was aware of the LIPA award losses while it sold millions of shares to investors. We also believe current disclosures lack full transparency and omit material information. In light of this, we believe investors should discount the value of FuelCell’s backlog in addition to current and future project awards.

FOIA Request Reveals New Concerns

The Brookhaven Rail Terminal (LIPA 2) and Clare Rose (LIPA 3) projects were awarded to FuelCell in July 2017. The wins were significant with 32.4 MW of rated capacity and $636m of future revenues, compared to FuelCell’s current operating portfolio of 32.6 MW and trailing revenue of only $71m – these awards were a significant part of FuelCell’s bull case, providing evidence of demand for the company’s technology and ability to execute.

We published evidence that LIPA cancelled the awards due to the impact of the recently enacted New York Climate Leadership and Community Protection Act (CLCPA), which made natural gas-powered fuel cells ineligible for renewable energy credits without which the projects became economically unattractive for LIPA. However, in reality the full picture was worse.

We filed a Freedom of Information Law (state and local government version of the FOIA) request, asking for records related to the cancellations. The documents reveal new information and additional inconsistencies.

The files contain three emails (Jul19, Oct19, Mar20) sent by officials at the Public Service Enterprise Group (PSEG, the private entity implementing LIPA’s operations) to FuelCell’s SVP of Sales. They memorialize several meetings and communications between LIPA, PSEG and FuelCell officials between July 17, 2019 and March 3, 2020.

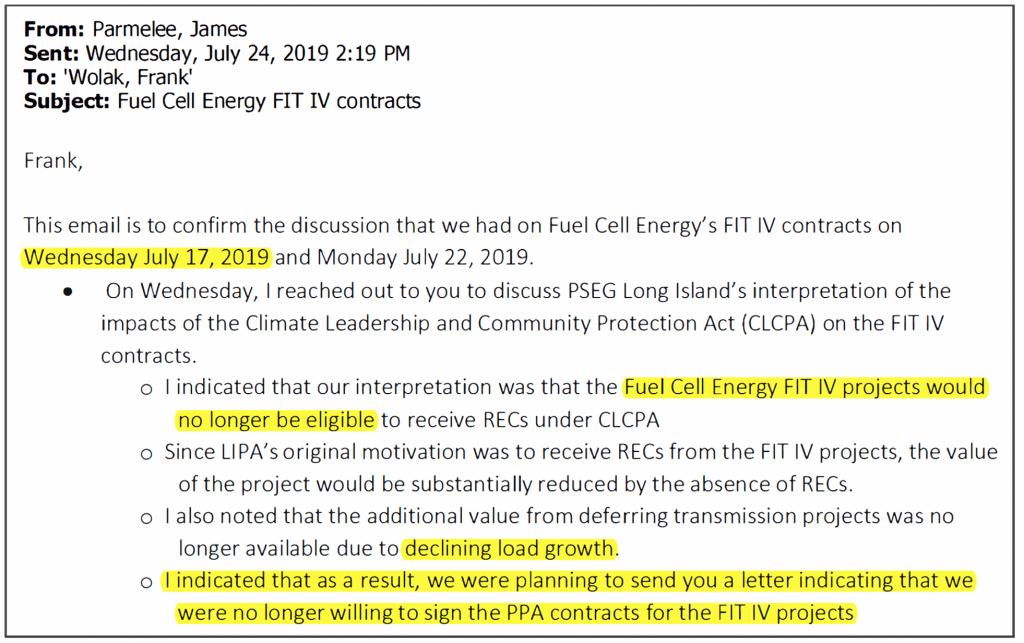

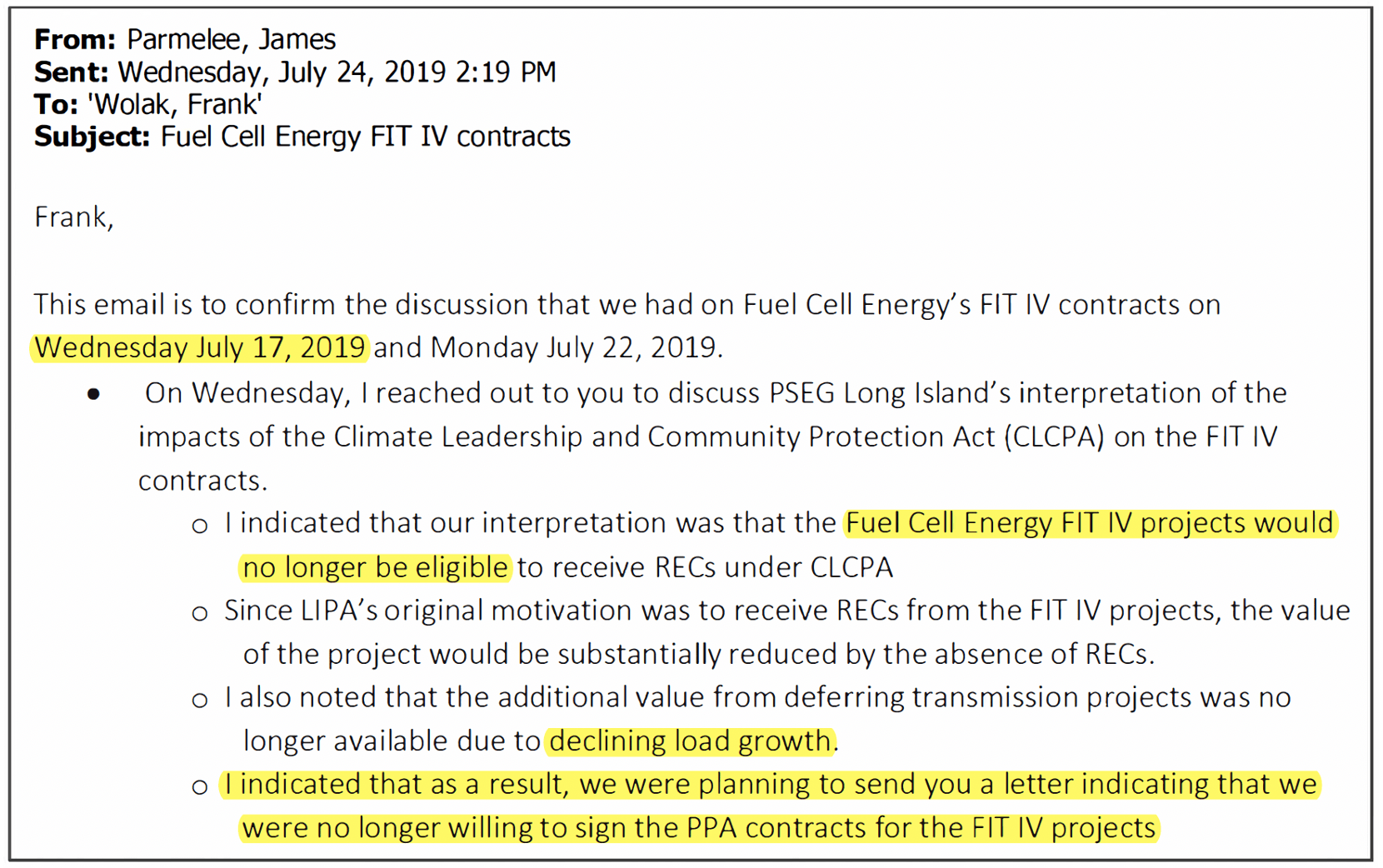

Exhibit 1. Excerpt of email from PSEG Director of Contracts to FuelCell’s SVP of Sales

Source: LIPA, our highlights

The most relevant information is summarized below:

- On July 17, 2019 LIPA first notified FuelCell that the new CLCPA would negate energy credits for the LIPA 2 and LIPA 3 projects.

- LIPA also said due to declining load growth in the region, the projects provided less value than when originally planned.

- As a result of both of these developments, LIPA was “no longer willing to sign the contracts.”

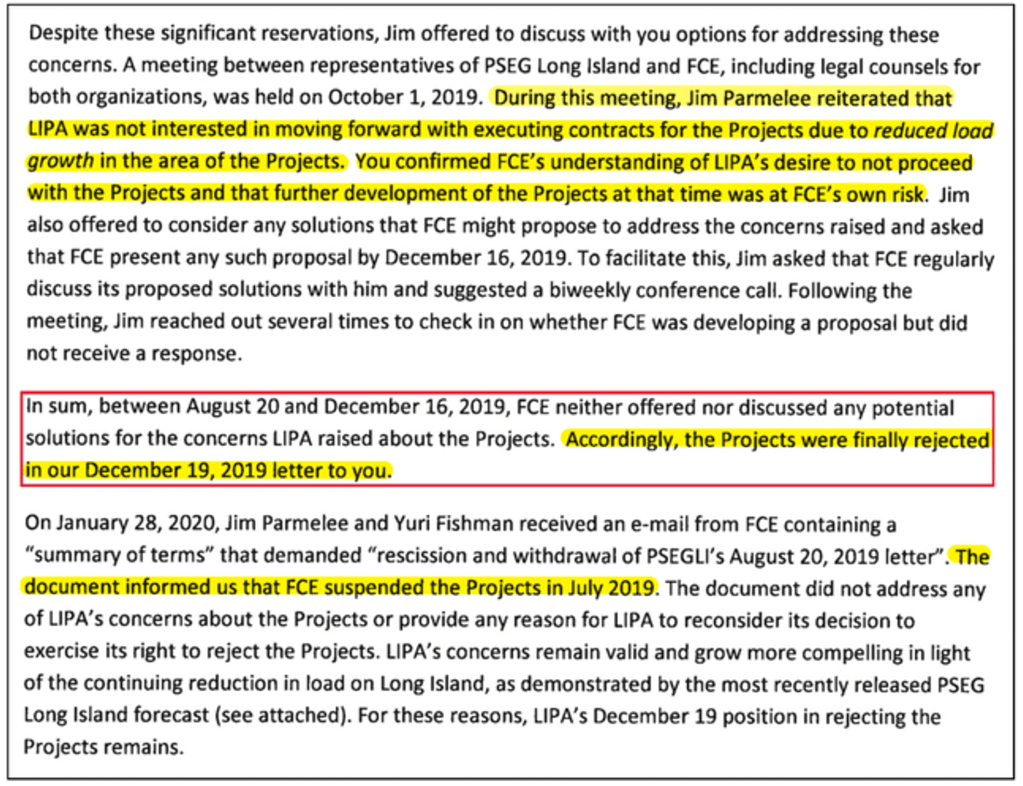

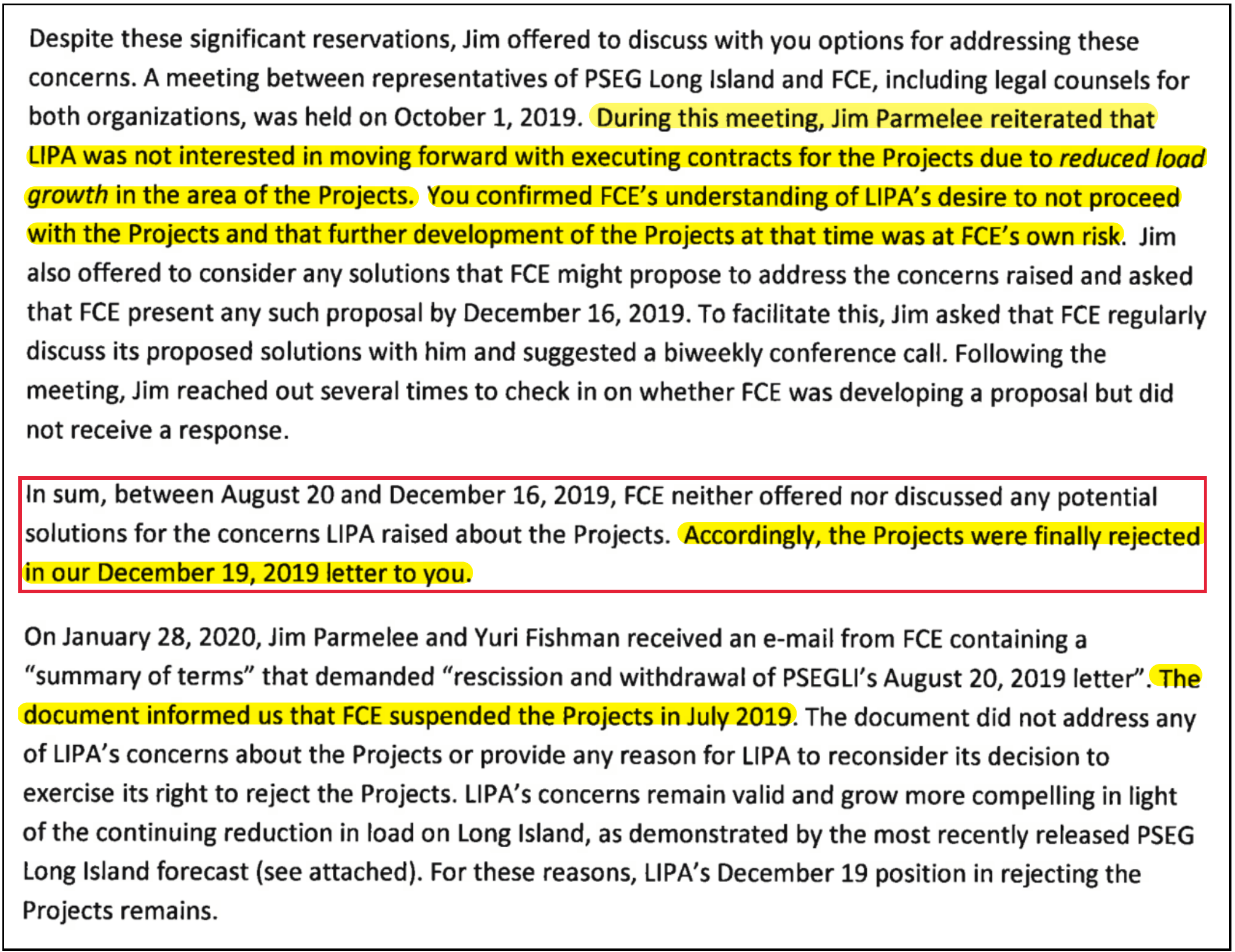

- On October 1, 2019 LIPA officials agreed to consider FuelCell’s proposals to enhance the value of the projects with a target date in December 2019 for submission. LIPA suggested frequent communication between the two parties, to further chances of success.

- Despite these offers, there’s no evidence that FuelCell made contact with LIPA or submitted proposals.

- Due to the CLCPA, reduced load growth and FuelCell’s failure to address any of LIPA’s concerns, LIPA officially cancelled the projects in a December 19, 2019 letter to FuelCell (see email in Exhibit 2).

- FuelCell responded in a January 28, 2020 email claiming that it had suspended the projects in July 2019.

Exhibit 2. Excerpt of March 3, 2020 email from PSEG Director of Contract Management to FCEL SVP of Sales

Source: LIPA, our highlights

We now know FuelCell first became aware that LIPA was unwilling to sign PPA contracts on July 17, 2019. Despite this, for the next 15 months until our report was published, management continued to represent the projects as active and going through standard processes – for example, in the third quarter 2019 10-Q [Pg.51], and during the fourth quarter 2019 and third quarter 2020 earnings calls:

The one thing that you noticed or noted in the backlog is we’ve made a decision that we’re going to talk about backlog for projects that we have signed PPAs. The other two LIPA projects as PPAs aren’t signed, they are still in ISO. So, those are things that we continue to work on but great progress to-date on Yaphank.

– CEO Jason Few, January 2020

Got it and then on the two LIPA projects you are still working on. I mean, I would assume those are still progressing. Any thoughts on timing or is it still more just going to get through the process, interconnect, etcetera?

Yeah, Eric it’s more get through the process, our Yaphank project we are well into that process for that project and expect that — and we’re making good progress there. But we’re going through interconnects and all the things that you have to do and those things take time.

– CFO Michael Bishop responding to analyst question, September 2020

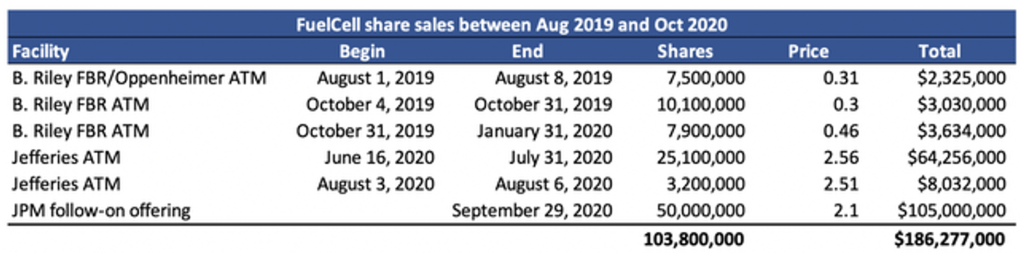

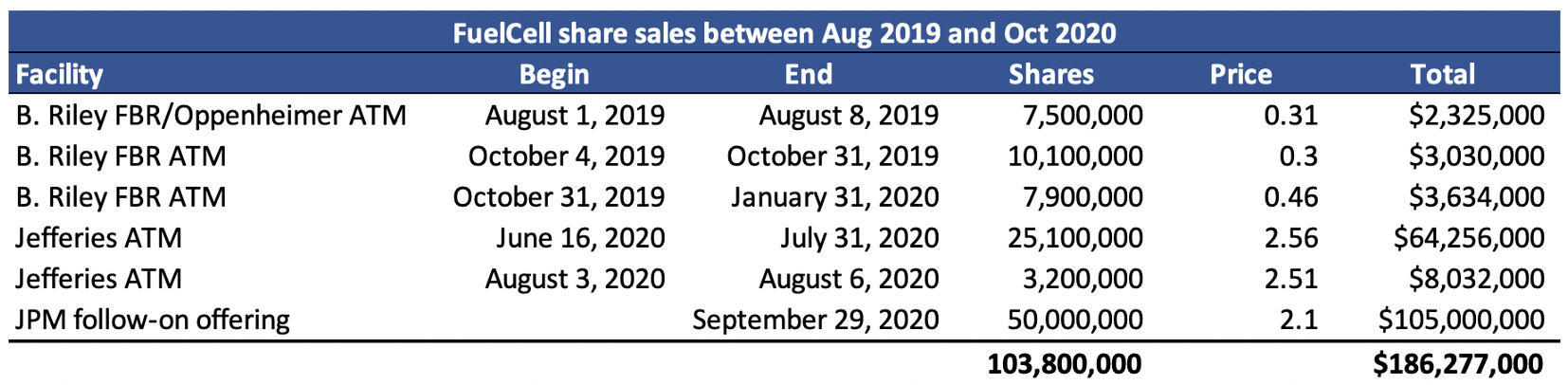

During those 15 months, FuelCell sold over 100m shares to investors via at-the-market programs and a follow-on offering.

Exhibit 3. FuelCell sold over 100m shares after learning of project cancellations

Additionally, the emails expose a continued lack of transparency regarding LIPA 2 and LIPA 3. Note that FuelCell only began disclosing the project losses after our original report. The following is the most recent disclosure included in the 2020 10-K [Pg. 68]:

“In July 2017, we were awarded three projects on Long Island totaling 39.8 MW. In December 2018, we executed a contract for one of the three awards, which is currently reflected in our backlog. The other two awards, which are not part of our backlog, do not yet have signed contracts as we have been progressing through the required interconnect process. Contrary to assertions made by Long Island Power Authority (“LIPA”), we do not believe that the New York Climate Leadership and Community Protection Act negates the two project awards for which there are not signed contacts. We believe these projects should move forward and we have continued to pursue them in good faith, including with our advancement of the interconnect process. There can be no assurance that any project awards, including these two LIPA awards for which we do not have signed contracts, will result in executed PPAs.”

It now appears LIPA was within its rights to cancel the awards for any reason – including projections of reduced load growth in the area. We find it concerning that this detail hasn’t been communicated to investors. Instead, in its disclosures FuelCell claims the issue is the CLCPA alone, implies it has pseudo-contractual rights and has “continued to pursue [the projects] in good faith, including with our advancement of the interconnect process.” Note that this statement itself contradicts FuelCell’s claim to LIPA that the projects have been suspended since July 2019.

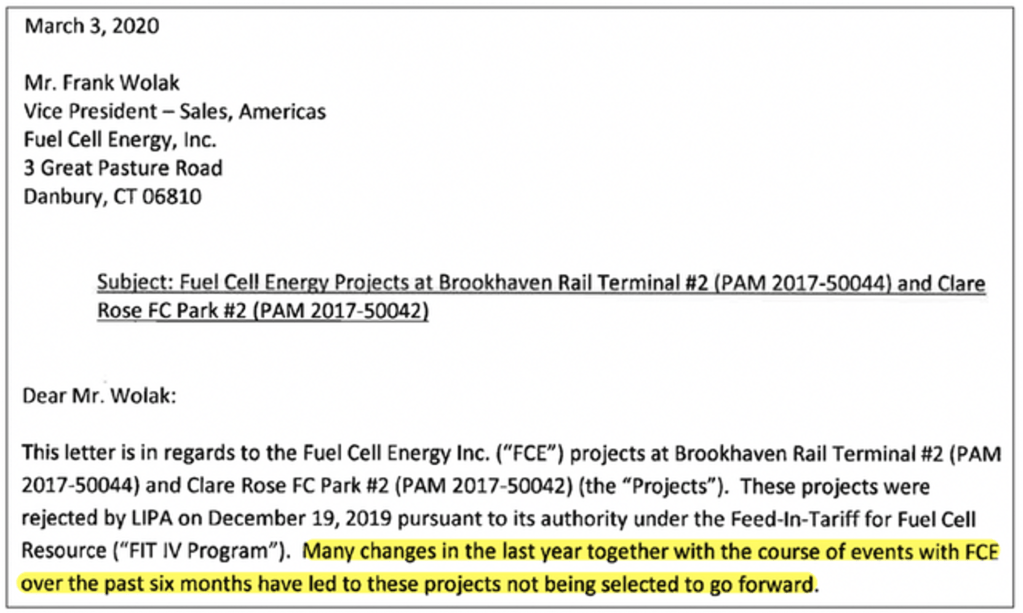

The emails also reveal potential performance and execution issues at FuelCell. LIPA generously offered to work with the company over several months to address its concerns, but it appears FuelCell made no effort. LIPA’s frustration is evident in the March 2020 email:

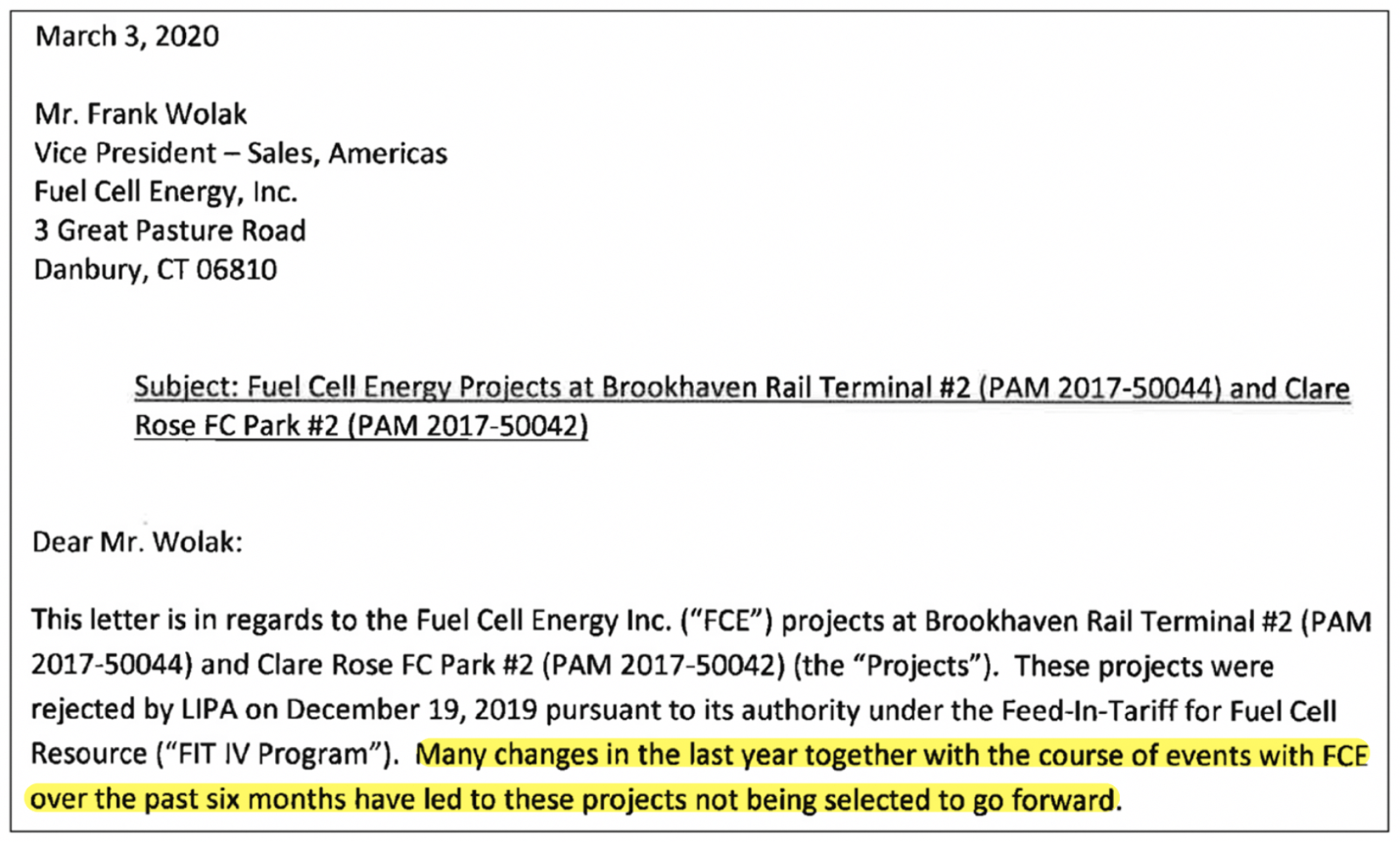

“Many changes in the last year together with the course of events with FCE over the past six months have led to these projects not being selected to go forward.”

Exhibit 4. Excerpt of email from PSEG Director of Contract Management to FCEL SVP of Sales

Source: LIPA, our highlights

Priced For Perfection

We believe these issues take on extra significance in the context of the 1200%+ rally in FuelCell shares since mid-November. Admittedly, we did not anticipate how investor enthusiasm for the ESG space would develop when we first published in October. A confluence of positive events including tax incentives and a new environmentally friendly administration and Congress, along with an exogenous and, in our opinion, reckless rally in popular retail names, has led to a complete re-pricing of the clean energy sector.

We closed our previous short last year but have re-established a position near these levels. It’s appropriately sized for the environment and we’re willing to add on strength and press on weakness assuming the fundamental picture remains as it is, which in our view means completely unsupportive of FuelCell’s current valuation. While FuelCell was able to raise cash in December (at $6.50 after breaking a lock-up agreement a month early [Pg.S-13]) and the regulatory outlook is more favorable, recall the most significant recent company specific developments have been unambiguously negative: FuelCell missed Q4 2020 revenue and earnings estimates, and lost three project awards from Connecticut, the company’s home state.

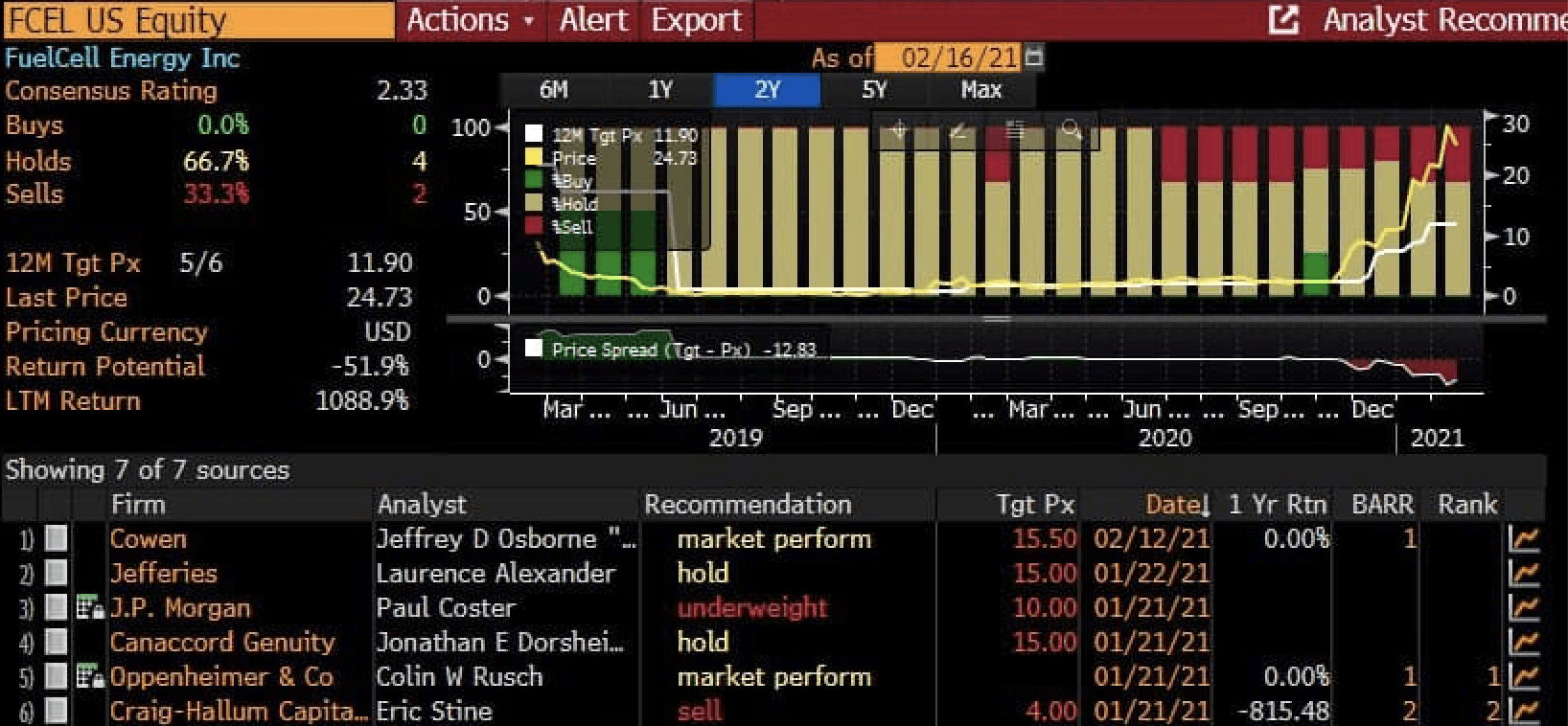

Yet FuelCell trades with an enterprise value of roughly $7.2bn or an 80x multiple on 2021E revenue. Even the sell-side, which in our view was already optimistic, has pulled back with several analysts recently downgrading the stock. None of the six covering analysts rate it a Buy and the most sanguine has a price target 35% below current prices.

Exhibit 5. Analyst recommendations on FCEL

Consider that most of these analyst targets are based on 10-to-20-year models with very favorable assumptions: projections of persistent revenue growth, eventual breakeven and margin expansion, consistent returns on capex and low cost of capital over the long term. All would require exceptional execution. In light of what our FOIA uncovered, including a continued lack of transparency and potential execution issues, we suggest investors reconsider the valuation here.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}