- Mondee, an airfare consolidator, trades at sector leading multiples despite mediocre growth, extreme leverage, and rising default risk.

- Recent loan amendment indicates Mondee’s lenders are losing patience after missed payments and financial covenant breaches.

- The amendment requires Mondee to find new lenders for $155m in loans (23% effective rate) in 4 months to avoid triggering default. New debt would likely be on worse terms.

- Principal on Mondee’s loans and puttable preferred equity is growing as 20% of interest and 100% of dividends are paid-in-kind.

- Net Debt to 2023 adj. EBITDA is 10x; Interest plus dividends of $45m in 2023 is almost 3x estimated organic revenue of $16m.

- Mondee announced a $40m buyback in October with less than $49m in unrestricted cash and -$21m in free cash flow thru 3Q23. What management didn’t announce is they lack lender permission to conduct such a buyback.

- Insiders sold 5.3m shares at $10 in June, weeks before agreeing to sell a subsidiary that led to a $30m cut in revenue guidance.

- Stock is a ticking time bomb at 24x EV/’23E adj. EBITDA, higher than ABNB. OTA sector average 10x would value Mondee shares at $0.

- High probability of near-term common equity wipeout with rising default risk on growing debt balance.

Disclosure: We are short Mondee. Please see full disclaimer at bottom of report.

November 30, 2023 — While Mondee (July 2022 de-SPAC with 97% redemptions) positions itself as a “travel technology company and modern travel marketplace” advertising involvement with buzzy concepts like A.I., it’s essentially an airfare consolidator – it buys discounted airfare directly from airlines and re-sells it at a markup. Approximately 80% of the business is low margin airfare wholesaling, with the balance in higher margin bookings for hotels, cruises, and car rentals.

Mondee differs from traditional direct-to-consumer OTAs like EXPE and BKNG in that it’s primarily a business-to-business intermediary. Most of Mondee’s sales are to travel agents and corporate travel managers rather than end consumers, a distinction the company touts as a closed, higher margin ecosystem. In the end, however, Mondee is an intermediary between intermediaries, generating margins mainly on airfare resales evidenced by take rates below large cap OTAs.

Unfortunately for common equity holders, high interest debt and preferred equity, both growing in size with 20% of interest and 100% of dividends paid-in-kind, overwhelm Mondee’s marginally profitable business (2023 guidance is 9% adj. EBITDA). We think positive adj. EBITDA and headline growth cover an undifferentiated, wholesaler intermediary business that’s horribly managed and dangerously over-leveraged. Time is short on the charade pricing such a company at the highest multiples in travel services, in our view.

We think the market missed a recent loan amendment that shows Mondee has exhausted lender patience after missed payments, covenant breaches, and a crackpot stock buyback announcement. We think risk of default or a recapitalization in which common equity is wiped out is high. Our price target is $0.

Ominous Start: Troubled SPAC, Almost Total Redemptions

Mondee’s July 2022 reverse merger transaction with SPAC sponsor ITHAX suffered almost total redemptions and the sudden, unexplained resignation of lead advisor Deutsche Bank. After serving as lead placement agent since 2021, Deutsche Bank resigned abruptly without explanation in June 2022, waiving $3.5m in fees only a month before the official de-SPAC. Even Mondee thought it was strange [Pg. 105]:

“We believe that such a resignation and fee waiver for services already rendered is unusual. While Deutsche Bank did not provide any additional detail in its resignation letters either to ITHAX or to the Securities and Exchange Commission, such resignation may be an indication by Deutsche Bank that it does not want to be associated with the disclosure in this proxy statement/prospectus or the underlying business analysis related to the transaction.”

Shareholders in the SPAC similarly wanted little involvement in a public Mondee redeeming 97% of 24.8m shares. The near total redemptions put Mondee below Nasdaq share count and market value requirements, resulting in a notice of delisting (Mondee eventually found a buyer to put them just over the minimums).

The mass exit isn’t surprising considering the current situation at Mondee.

Ugly Balance Sheet: High Interest Debt and Preferred Equity Growing in Size

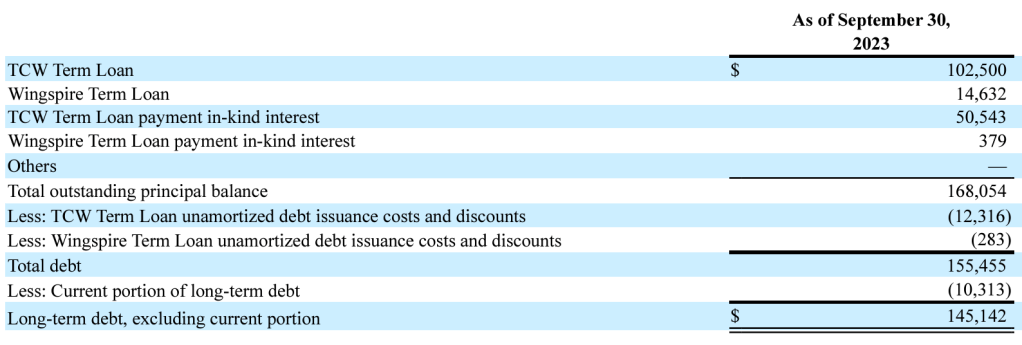

Mondee’s debt consists of $155m in term loans at SOFR + 8.5% (23% effective rate through 3Q23) maturing at the end of 2024. There’s also $102m in preferred equity accruing paid-in-kind dividends at SOFR + 7.0-8.5%, increasing to SOFR + 10.5-12% next year. The current SOFR is 5.3%. Holders of the preferreds have put rights in 2028, or in 2026 if Mondee doesn’t generate $50m of adj. EBITDA in 2025 (consensus estimate is $40m).

The loans were granted by asset manager TCW between December 2019 and February 2020, just before travel imploded. Mondee has had difficulties servicing the loans ever since, missing payments in June and September 2022 [Pg. 74] and breaching financial covenants.

Put simply – we don’t think Mondee’s business can support anywhere near this amount of debt. Combined interest and dividends this year will total approximately $45m (18% of principal). Compare this to adj. EBITDA guidance of $20m, -$13m in cash flow from operations through 3Q23, and only $40m in unrestricted cash at Q3.

We estimate 20% of $33m term loan interest expense this year will be paid-in-kind. All of the ~12% dividend on the preferred equity is also PIK. The pile of commitments senior to common equity is growing.

October Loan Amendment Suggests Lenders Accelerating External Refinancing or Default

Mondee’s balance sheet situation would be dire even if the loans weren’t maturing next year – the loans turn into current debt beginning on January 1. But judging by a recently filed loan amendment, we believe lenders TCW and Wingspire (which joined as a party in 2023), have lost patience and are accelerating either a third-party refinancing or default.

Filed on October 17, loan Amendment No. 11 requires Mondee to meet refinancing milestones including retaining a financial advisor by October 31 and consummating an external refinancing before March 15, 2024. Mondee didn’t announce the amendment and we think most investors missed a filing which in our view has existential implications for the stock.

Lender stipulated refinancing milestones for Mondee, any of which are missed is an event of default [Pg. 52]:

- Retain financial advisor or debt placement agent by October 31

- Deliver plan for refinancing by November 30

- Deliver one or more indications of interest or term sheets with respect to such plans by December 31

- Deliver binding proposal or commitment letter by January 31

- Consummate refinancing by March 15

It’s hard to imagine how Mondee’s balance sheet isn’t even more bleak next year. Assuming Mondee finds an interested lender, we think any refinancing will likely be more punitive than the current 22% effective rate and/or require further incentives unfriendly to equity.

The amendment also reduces lender commitments, excuses financial covenants, and adds a penalty fee:

- Monthly fee of 0.5% on any outstanding amount left on the term loans after March 15, which would take the effective interest rate to nearly 30% [Pg. 79].

- Lender commitment on $15m line of credit withdrawn (modified to uncommitted and discretionary), but the 1% commitment fee is maintained [Pg. 8].

- Mondee must maintain at least $15m of cash net of excess payables [Pg. 130].

- Adds $1.7m general amendment fee [Pg. 78].

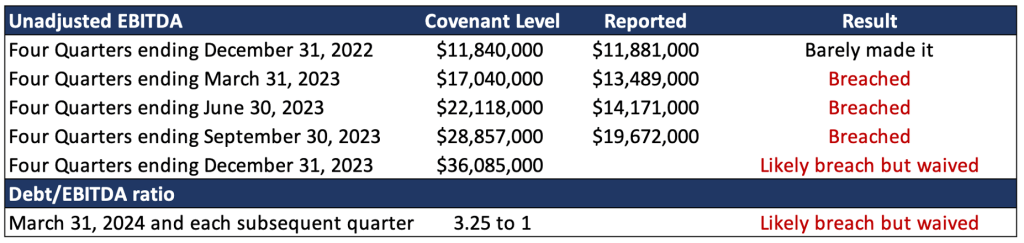

- Financial covenants will no longer be measured [Pg. 129].

We think TCW/Wingspire excused the financial covenants because Mondee agreed to look for external refinancing almost immediately, improving recovery outcomes for TCW/Wingspire. Mondee was going to breach the covenants anyway, at least now they are actively looking for another lender. If Mondee is unable to refinance, TCW/Wingspire can accelerate the loans and declare them due immediately, but the timing is moved forward.

The term loans also originally specified a Fixed Charge Coverage ratio covenant beginning in 3Q23, which Mondee would have likely complied with but only because so much interest is being paid-in-kind.

Even if Mondee’s lenders were willing to continue the status quo, we don’t think Mondee’s core business can grow fast enough to service the debt in a cash flow positive scenario without considerable additional equity investment. The loan amendment adds a $15m minimum cash covenant (net of excess payables, so actually higher than $15m) which narrows Mondee’s acquisition range to small, relatively insignificant targets.

We think the austere demands from TCW and Wingspire put the stock at risk of massive downside before the March 2024 refinancing deadline.

Recently Announced Buyback: Reckless, Partially Prohibited, and Crams Down Common Equity Further

The amendment also reveals Mondee lacked lender permission for the $30m buyback program announced on September 21.

On October 17, Mondee announced it was increasing the program to $40m and issuing up to $15m in additional preferred equity (on top an existing $85m), $10m of which was funded. However, loan Amendment No. 11 (filed with the SEC on the same day) disclosed the lenders only would permit up to $5m of share buybacks if Mondee raised $5m in equity.

TCW also required Mondee to raise the equity by October 23, otherwise fees ranging from $2-$10m would be triggered [Pg. 79]. The high fees and near-term deadlines show TCW’s frustration with Mondee’s buyback announcement, in our view.

So Mondee only has permission for $5m of buybacks and, lender permitting, has to raise additional equity equal to whatever it wants to repurchase above that amount. If Mondee were to conduct $40m in common stock buybacks, it would need to raise a total of $40m in preferred equity.

The phrase “borrowing from Peter to pay Paul” comes to mind.

Mondee was only able to raise another $10m in preferred equity because it restructured existing shares. An entity known as Madave Management LLC owns $75m of the original $85m preferred shares raised in September 2022 (the $10m balance is owned by Morgan Stanley Credit). Madave bought $10m more preferreds after Mondee increased the dividend 150bps to a high of SOFR + 12% on the $10m additional as well as the $75m original shares and lowered the exercise price on 1.275m attached warrants from $11.5 to $7.5. The same deal is being offered to Morgan Stanley if it buys more than $1.3m of the new preferreds. Clearly, Mondee is not raising money from a position of strength.

Weak Organic Growth and Poor Margins. Comparison to Despegar and Large Cap OTA’s Reveals Extent of Over Valuation

Most of Mondee’s growth this year comes from four acquisitions done since January. The largest, a Brazilian travel consolidator called Orinter, did $9m adj. EBITDA and $31m revenue in 2022. Assuming 0% growth over 2022 for Orinter and the three smaller acquisitions, we estimate they accounted for $28m of the $36m increase in revenue Mondee reported through the first nine months of 2023. This implies organic growth of 6%, significantly below OTA large caps like TRIP (+23%) and EXPE (+10%).

Mondee only generated $36m of revenue growth ($8m organic) and $14m of adj. EBITDA in the first nine months of 2023 compared to $33m in interest and dividend expense.

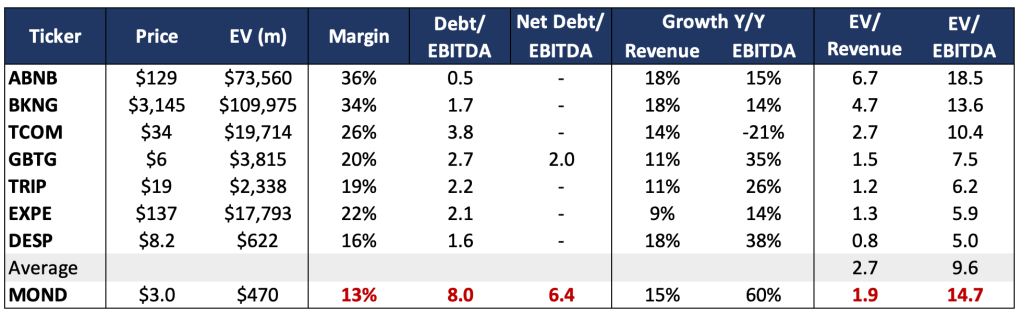

TRIP and EXPE trade at 6x 2024 adj. EBITDA vs 15x at Mondee. A 6x multiple would leave Mondee common equity at $0. We think it’s absurd that Mondee trades at such a high multiple even though interest expense plus preferred dividends are approximately 225% of EBITDA.

Mondee’s own SPAC valuation methodology put a 7.2x EV multiple on 2023 adj. EBITDA [Pg. 12]. This during the relative optimism of late 2021 when travel was first rebounding, and SPACs weren’t yet considered investment bank enrichment schemes. A 7.2x multiple on $20m 2023 adj. EBITDA would value common and preferred equity at $0 and impair the loans.

We think Latin American OTA Despegar (NYSE:DESP) is a good comp, with similar enterprise values and Mondee’s growing exposure to LATAM (three of four acquisitions this year based in LATAM).

Despegar is less levered and it’s online travel business is higher margin and roughly 3x the size of Mondee’s – yet Mondee trades at considerably higher multiples.

At Despegar’s multiples, Mondee common equity would be valued at $0. Even at a slight premium to Despegar (perhaps to account for a LATAM macro discount), Mondee common equity would be valued at $0.

At the same time, margins are weak and declining. In its 2Q report, Mondee cut adj. EBITDA guidance by 35% to $25-30m from $40-45m blaming “one-time costs” in developing it’s “A.I. Travel Marketplace”. In Q3 Mondee cut the outlook further to $20m. Implied margins of 9% in 2023 narrowed from 10% in 2022 and are significantly below Despegar (14%).

Sequence of Events Surrounding Business Divestiture Calls into Question Management Transparency

Mondee also cut revenue guidance in Q3 to $217m (down from $245-250m), blaming the sale of a subsidiary called LBF travel which did $33m in revenue in 2022.

The 3Q23 10-Q revealed Mondee entered into a letter of intent in July to sell LBF [Pg. 27]. We think the timing of the sale, a large insider secondary offering, and contradictory changes to guidance suggests a lack of operational control and poor management transparency:

- June 7: Secondary of 5.3m shares at $10. Nearly all shares are owned by insiders, employees or former employees, pre-SPAC shareholders, affiliates of SPAC sponsor ITHAX, and PIPE investors [Pg. S-109].

- July: Mondee enters letter of intent to sell LBF.

- August: Mondee raises 2023 revenue guidance by $5m to $245-250m but cuts adj. EBITDA to $25-30m from $40-45m saying “one-time marketing and personnel costs of approximately $20 million are estimated to be required over the remaining year in order to maximize and accelerate the adoption of this revolutionary platform.”

- September 29: LBF sale closes.

- October: Mondee announces increase to stock buyback program.

- November: revenue guidance cut to $217m, blamed on LBF sale. Adj. EBITDA cut to $20m, even though LBF was generating adj. EBITDA losses. CEO says some of the $20m in on-time marketing costs will be spent in 2024.

Management has not responded to a request for comment on the timing of the 5.3m June secondary just before agreeing to sell LBF which resulted in a cut to revenue guidance which was disclosed 4 months later, but not before a now puzzling intermittent raise in revenue guidance.

Mondee Operates in Archaic, Highly Competitive Space. Platforms Suffer from Bugs and Security Issues

Mondee is one of the largest airfare consolidators in North America, growing through 18 acquisitions of consolidators and wholesalers since its founding in 2011. The highly competitive consolidator space includes Picasso Travel, Centrav, GTT, Sky Bird, and Downtown Travel, all advertising superior technology connecting travel agents to airline inventory. Wikitravel lists over a dozen more. None of these competitors are public, which we think is a symptom of the antiquated, “mom and pop” nature of the industry which has shrunk significantly since the advent of the internet.

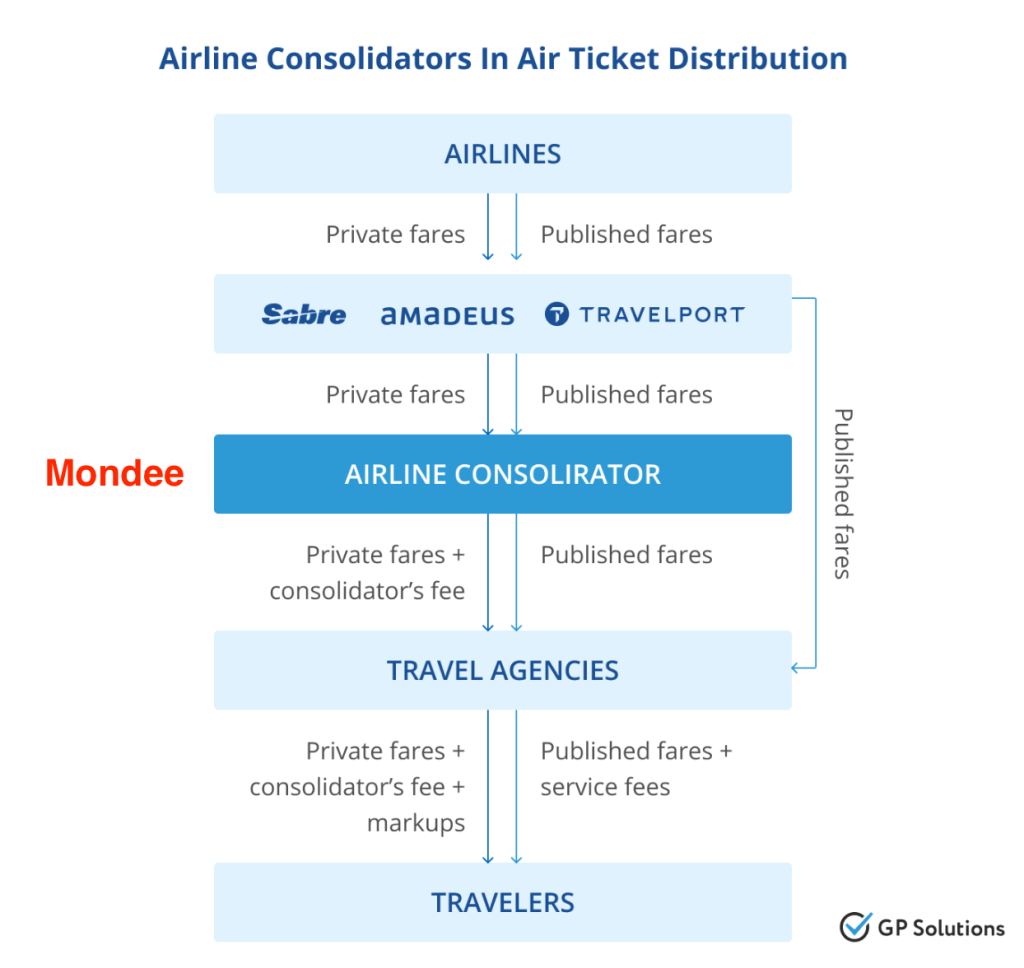

Airline consolidators like Mondee are intermediaries between intermediaries, sitting between airline inventory systems known as Global Distribution Systems (GDS) and travel agents. Pre-internet, consolidators were a key distribution outlet, providing bulk demand for tickets and then doing the relatively manual work of selling the tickets to travel agents.

Mondee is an intermediary between intermediaries

Today airlines increasingly sell tickets directly via their own online systems or through OTAs. The number of tickets booked through consolidators has declined significantly, but consolidators still serve niches for instance by marketing to specific groups or providing smaller travel agencies with access to GDS which can be expensive. Still, considering their intermediary between intermediaries function, we don’t think the outlook for the consolidators is particularly bright.

Mondee has attempted to differentiate itself by entering the more fragmented and higher margin hotel consolidator space, but competition is steep with large OTAs like EXPE and Webjet (ASX:WEB) already involved. The company also offers subscription products like its UnPub and Rocketrip platforms in which users pay membership fees for access to discounted tickets. Mondee touts a user base of 10m in its “SaaS platform” but only reported segment revenue of $930k through 3Q23 down 4% y/y.

We’d think Mondee common stock was doomed even if Mondee had somehow, overnight dramatically improved the technology behind TripPro, its main booking platform since 2015. But we couldn’t even sign-up for an account at TripPro in multiple attempts due to website malfunctions.

Half-way through the sign-up process, the TripPro website stalled every time. Customer service, on a scratchy overseas connection with a considerable lag, told us to try again after clearing our browser cache and cookies. That didn’t work either.

TripPro also has data security issues. According to TechCrunch, in July a researcher found a completely unprotected TripPro database 1.7 terabytes in size containing customer personal information including unencrypted dates of birth, genders, and credit card numbers. When TechCrunch asked Mondee for comment, a spokesperson didn’t acknowledge the security lapse, but the database was secured soon after.

We also briefly checked out Tripplanet, another of Mondee’s primary booking platforms and here the account creation process completed successfully. However, we don’t see significant differences between Tripplanet’s direct-to-consumer application and “traditional” OTAs. Multiple flight searches on Tripplanet produced the same pricing (+/- $1) for the same flights compared to searches on Kayak and Expedia.

In July, Mondee launched a generative A.I. assistant called Abhi, but as far as we can tell it’s basically a standard chatbot that can recommend itineraries and provide booking links within the Tripplanet app (as opposed to links to third-party booking websites). Tripadvisor announced the launch of its generative A.I. trip planner on the same day Expedia launched its A.I. product in April. Mondee isn’t breaking new ground here, in our view.

Abhi may lead to incremental gross bookings, but we’re skeptical it can generate needle moving improvements or significantly increase Mondee’s take rates. After an uninspiring 7% take rate in 2022, through 1H23 Mondee’s take rate improved to 7.6%, remaining below larger and significantly less levered traditional OTAs (DESP 14%, EXPE 11%, BKNG 12%).

On Valuation or Default Stock Belongs at Zero

We think Mondee’s $250m (and growing) high interest debt load drowns its undifferentiated low organic growth travel intermediary business which if valued at appropriate multiples leaves no value for common equity.

Mondee, which pays half of its interest expense in kind and is still CFO negative, is recklessly proposing buybacks of its objectively overvalued stock, apparently angering its lenders which are now requiring an external refinancing before March 2024 and the issuance of more preferred equity, cramming down common stock further. We see significant “jump-to-default” risk with common equity currently valued at $300m. We expect total loses for common shareholders.

Disclaimer

As of the publication date of this report, Night Market Research (NMR) and Connected Persons (as defined hereunder), along with or through its members, partners, affiliates, employees, clients, and investors, and/or their clients and investors have a short position in the securities covered herein (and options, swaps, and other derivatives related to these securities), and therefore will realize significant gains in the event that the price of any stock covered herein declines. NMR and NMR Connected Persons are likely to continue to transact in the securities covered herein for an indefinite period after an initial report, and such position(s) may be long, short, or neutral at any time hereafter regardless of their initial position(s) and views as stated in NMR’s research.

Use of NMR’s research is at your own risk. In no event shall NMR or any NMR Connected Person be liable for any direct or indirect trading losses caused by any information in this report. You further agree to do your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities covered herein.

This is not an offer to sell or a solicitation of an offer to buy any security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. NMR is not registered as an investment advisor in the United States, nor does NMR have similar registration in any other jurisdiction. To the best of NMR ‘s ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources NMR believes to be accurate and reliable, and who are not insiders or connected persons of the issuer covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind – whether express or implied. NMR makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and NMR does not undertake to update or supplement this report or any of the information contained herein.

NMR Connected Person is defined as: NMR and its affiliates and related parties, including, but not limited to any principals, officers, directors, employees, members, clients, investors, and agents. One or more NMR Connected Persons may have provided NMR with publicly available information that NMR has included in this report, following NMR’s independent due diligence.