- POET Technologies has been pre-selling vaporware for over a decade. ‘Imminent commercialization’ is their motto—except it’s never materialized. Now they’re running the same playbook during an optical networking bubble.

- Two weeks ago, the façade cracked with POET falling 50% when it disclosed that Celestial AI / Marvell Technology canceled product orders, citing “disclosure issues.” We unveil the apparent truth behind the cancellation:

- A Senior Director of Product Management at Celestial AI told us POET hasn’t been discussed internally since 2023. The partnership has apparently been dead for years.

- POET waited days to disclose the cancellation. We think POET has history of inadequate transparency which we’ll show throughout this report.

- POET’s resurrection has been spectacular: a >200% rally in weeks, capped by a 43% pop yesterday. We think it’s full of hot air.

- Yesterday’s 43% surge was driven by a purchase order from Lumilens—an obscure startup that we believe has no intention of fulfilling it. Lumilens closely equates to Rain Tree, which we believe is a recycled relationship of POET. The red flags:

- Lumilens owns nothing. No patents, no tech, no customers. Everything comes from Rain Tree Photonics—acquired seven weeks before the POET order.

- Rain Tree Track Record: Generated $800k over three years while burning through $9.5m in assets. Nine years, zero commercial products.

- We believe POET and Rain Tree have been linked since 2022. The companies share A*STAR connections; POET’s SVP co-presented with Rain Tree’s founder (now at Lumilens) in 2024.

- Rain Tree’s tech has fatal flaws: die-shift, warpage, yield issues that blocked commercialization for a decade. POET’s $50m bet rests entirely on this failed technology.

- Worse yet, Lumilens lacks the financial capacity to fulfill this order. So why announce $50m on the way to $500m of purchase orders? Stock hype, in our view: POET gets a headline. Lumilens pocketed tens of millions in warrants just for signing—with zero obligation to buy anything.

- Lumilens appears linked to POET’s mysterious $5m customer. Its CEO sits on the board of Accton/GoldiLink, whose offices are literally hundreds of feet from Lumilens in San Jose. This looks like circular promotion, not organic demand.

- We’ve seen this flawed playbook before: Plug Power, Canoo, and Luminar used similar ‘customer warrant deals’ to fake traction. They’re now bankrupt or down >90%. One key difference: Plug had Amazon. POET has Lumilens.

- Lo and behold, POET just raised $400m on the back of the empty calorie Lumilens deal, completing the Lumilens pump and dump.

- Last night’s earnings raised more red flags. Here’s what stood out:

- POET repeatedly touts a partnership with LITEON—including in last night’s earnings release. LITEON’s President, asked about POET said: “LITEON doesn’t cooperate with [POET]” and “there isn’t actual business between us.”

- POET disclosed an unnamed lawsuit, which they likely have real liability from, given their obvious delayed disclosure of Marvell partnership loss

- POET’s most profitable business is lending: they loaned $30m at 6% to an undisclosed borrower. Material disclosure? Yes. Any meaningful details? No. Classic POET.

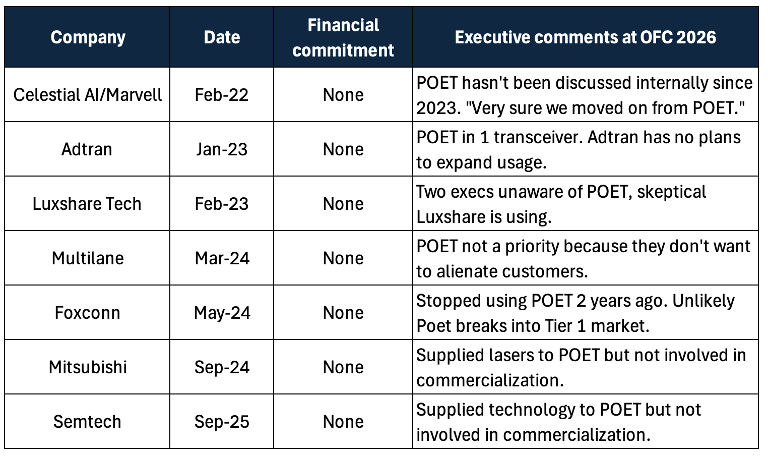

- At OFC 2026, we spoke with seven companies POET lists as active partners. Unanimous responses showed relationships that were commercially insignificant, stale, or worse:

- Foxconn stopped using POET 2 years ago.

- Two Luxshare executives had never heard of POET.

- Mitsubishi isn’t selling any POET product.

- Adtran: minimal use, no future plans.

- Semtech: low priority, component supplier only.

- Multilane: possibly ongoing but not a priority.

- POET systematically overstates the substance of partnerships. We think the Lumilens deal will prove equally hollow.

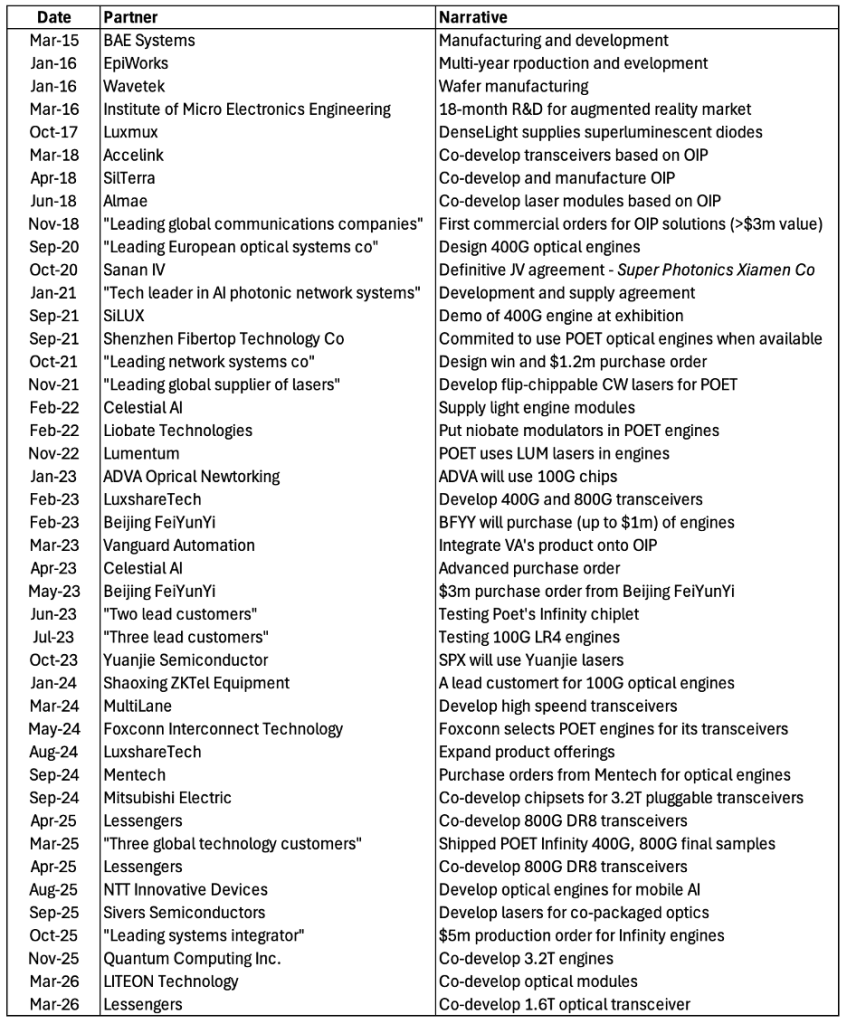

- Since 2015, POET has announced 30+ partnerships of little demonstrated commercial value—while diluting shareholders ~500%.

- In 2024, POET said Mentech selected POET chips but we contacted a Mentech spokesperson who denied this.

- The spokesperson expressed interest in partnering with us (Night Market), suggesting Mentech will partner with anyone.

- In 2024, POET touted co-development with Chengdu InSiGa Semiconductor Technologies, an entity whose website hasn’t been updated since 2022.

- Fact pattern of POET’s $5m order points to a lower-tier obscure counterparty and raises the risk of curtailment or cancellation, similar to POET’s unfulfilled $3m order from 2023.

- POET’s mysterious $5m customer: We believe it’s Accton—or more specifically, GoldiLink, an Accton subsidiary formed in 2024 with zero internet presence beyond a website. The $5m order risks cancellation, just like POET’s unfulfilled $3m order from 2023

- Rockley Photonics developed similar technology to POET and filed for bankruptcy in 2023.

- We spoke with a former senior engineer at Rockley who told us POET’s technology is “a solution looking for a problem”.

- Engineer believes POET’s technology doesn’t significantly improve performance and can’t compete in a cost-driven transceiver market.

- Engineer believes POET’s partnerships “mean nothing… and don’t indicate a business case”.

- Celestial AI’s October 2024 acquisition of Rockley Photonics’ IP for $20m, or roughly $0.15 per POET share, provides a benchmark for valuing POET’s IP.

- POET’s joint venture collapsed in November 2024 after its partner funded only ~1/3 of commitments. Our checks suggested the JV was effectively inactive even before the formal shutdown.

- Despite Rockley’s strong venture backing, it failed; POET’s institutional support appears limited to lesser-known investors with weak track records, including MMCap and L5 Capital.

- L5 Capital is managed by the CEO of Pharmacielo, a cannabis firm excoriated by Hindenburg Research in 2020. L5’s public holdings are down over 90% on average.

- We visited POET’s Toronto HQ building. No offices on POET’s floor had nameplates for POET or Suite 1107. Where 1107 should be located, offices were small or littered with trash. Neighboring tenants did not recognize POET.

- POET’s CFO Thomas Mika, who made comments regarding Marvell, previously led reverse mergers which destroyed shareholder value.

- One of POET’s primary manufacturing partners is a distressed Malaysian microcap facing governance issues, executive departures, and significant stock declines.

- POET touts vanity awards that are marketing schemes operated by promoters out of suburban homes (pictures below).

- We believe POET should trade at a discount to cash of $800m (~$5/share), given a decade of broken promises, overstated partnerships, and serial dilution.

Disclosure: We are short POET. Please see full disclaimer at bottom of report.

“These violent delights have violent ends…”

May 15, 2026 —We’re short POET Technologies (NASDAQ: POET) because we think it’s a dead end chip business with disclosure issues that justify a valuation below cash. The company recently disclosed that orders from Celestial AI / Marvell Technology were canceled. Based on our research, POET’s relationship with Celestial appears to have effectively ended years ago, despite management’s portrayal otherwise. We also believe that several of POET’s other highly promoted partnerships are deteriorating or no longer active. And based on history and our read of the circumstances surrounding POET’s $5m order announced in October, we think it’s at significant risk of curtailment or cancellation.

We think the POET story is set to unravel. With circular partnerships with obscure counterparties and concerning disclosure issues, we believe the stock has substantial downside ahead at a nosebleed $4B valuation.

Executives at OFC 2026 Describe Partnerships That Are Commercially Insignificant or Dead

In March we attended OFC 2026 in Los Angeles, the optical networking industry’s most important annual event. We spoke to executives from POET’s purported partners including Celestial AI, Marvell, Foxconn, Mitsubishi, Luxshare, Multilane, Adtran, and Semtech.

We learned that POET’s most heavily touted partnerships are immaterial, stale or defunct. An executive from Celestial AI told us POET hasn’t been discussed internally at Celestial in roughly 3 years – at odds with POET’s disclosures and its explanation for Marvell’s order cancellation.

Similarly, a Foxconn executive said they stopped using POET’s products two years ago.

CEO Suresh Venkatesen said POET “generated significant industry interest” at OFC calling it the company’s “strongest validation to date”, echoing prior claims of “robust engagement” (2025) “turned heads” (2024) and “earned industry acclaim” (2023).

Our findings point in the opposite direction. Executives from seven POET partners described relationships that were immaterial or no longer active.

We provide details on Celestial/Marvell, Foxconn, Luxshare Tech, Adtran and Mitsubishi.

Celestial AI – POET’s announces Marvell/Celestial canceled orders. We believe the orders have been dead for years.

Until recently, the partnerships most central to the bull case for POET Technologies were Celestial AI and Marvell Technology. On April 27, POET disclosed that Marvell had canceled all product orders as of April 23, attributing the decision to disclosure issues that allegedly breached confidentiality agreements. We believe this characterization is misleading and that the underlying relationship had effectively died years earlier.

POET originally announced a co-development agreement and purchase order from Celestial AI in February 2022 for laser modules based on its technology. While the last related press release came in April 2023, investors continued to associate POET with Celestial—particularly after Marvell acquired Celestial in December 2025.

That narrative was reinforced by CFO Thomas Mika in an April 21 interview where he referenced an “invoice” from Celestial AI and suggested near-term product shipments to both Celestial and Marvell. His comments implied an ongoing commercial relationship, which we believe was inaccurate and misleading:

“We have an invoice from Celestial AI which we’re intending to ship product against, and that will be shipped this year, in fact I believe some of it will be shipped next quarter. So that light source product is the product we’re going to be selling to Marvell and Celestial AI, and that will assist them internally in developing those GPUs.” – POET CFO

Mika’s use of the term “invoice,” typically an itemized bill, is notable. We believe he was referring to the same “advance purchase order for initial production units” disclosed in 2022, which POET continues to cite in filings but appears never to have fulfilled. POET never announced another Celestial order beyond the original 2022 agreement, which was reiterated in 2023, nor has it disclosed the deal’s size. Considering that POET issues press releases for even minor developments, including a $500k order, this silence suggests the arrangement was immaterial and likely expired.

Indeed, at OFC 2026 we spoke with Celestial AI’s Senior Director of Product Management who told us Celestial doesn’t use POET lasers. They also said POET hasn’t been discussed internally at Celestial AI since 2023.

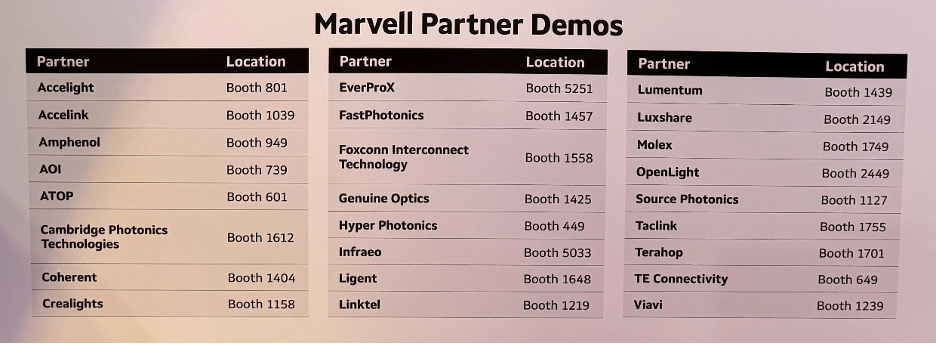

A display at Marvell’s OFC booth listing Marvell partners did not include POET:

We believe Celestial’s agreement with POET effectively expired years ago, and that Marvell only clarified its position because Mika publicly tied POET to Marvell. What sensitive information did Mika actually disclose in the interview, and why wouldn’t POET pursue legal recourse? POET’s explanation doesn’t add up. When POET blames a breach of confidentiality obligations, we don’t believe it is being fully transparent.

We asked management to clarify whether any Celestial orders exist beyond those announced in 2022 and 2023; we have not received a response.

In October 2024, Celestial acquired the patent portfolio of Rockley Photonics for $20m. Rockley was a close POET competitor, developing very similar optical chip integration technology. Given Celestial’s familiarity with POET through its partnership—and CEO David Lazovsky’s prior role on POET’s board—it’s telling that Celestial chose to buy Rockley’s IP rather than invest in POET. In our view, valuing POET’s IP at $20m, or roughly $0.15 per share, is generous.

Foxconn Interconnect – POET calls Foxconn one of its largest customers. Foxconn exec at OFC 2026 said they stopped using POET years ago

In May 2024, POET announced that Foxconn selected POET optical engines for its 800G and 1.6T transceiver modules. Production was scheduled to start in Q4 2024. POET has yet to begin production, according to filings. This was the company’s latest update on Foxconn from an October 2025 filing:

POET’s failure to deliver for Foxconn is consistent with comments from a Foxconn executive we spoke to at OFC. The executive told us Foxconn stopped working with POET two years ago and that POET will have a hard time breaking into the Tier 1 market given lack of commercial traction. Meanwhile, POET refers to Foxconn and Luxshare Tech as its largest customers.

LuxshareTech – POET calls Luxshare one of its largest customers. Luxshare execs at OFC 2026 were unaware of POET

POET announced a partnership with Luxshare in February 2023. According to POET, Luxshare would incorporate the Company’s 400G and 800G optical engines in its transceivers with product testing beginning in 1H23 leading to production in 2H23 handled by POET’s JV, Super Photonics Xiamen.

Of course, production didn’t happen in 2023 or even 2024. POET has yet to report revenue from the deal, although it has issued two Luxshare-related press releases painting a picture of continued work. In August 2023, POET announced a demonstration of a Luxshare transceiver incorporating POET’s 800G optical engine. In August 2024, POET claimed Luxshare was integrating POET engines into products already on the market. This integration appears to have failed or never happened considering POET’s trivial revenue in 2024 and 2025.

We spoke to two Luxshare product development executives at OFC 2026. Both had never heard of POET and were skeptical Luxshare was incorporating POET’s technology into Luxshare transceivers.

Adtran – Only using POET in 1 transceiver and no plans to expand usage

In 2023, POET announced Adtran was incorporating POET engines into an Adtran pluggable transceiver. POET also said the companies had a “good working relationship and discussions regarding additional products are on-going”.

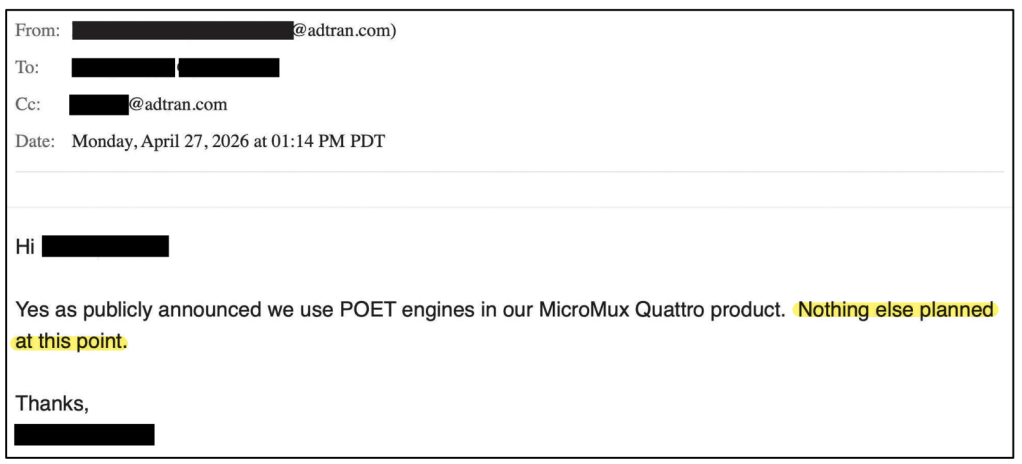

At OFC we spoke with an Adtran executive who told us POET’s technology is only in one Adtran transceiver which remains in technical testing.

We confirmed with another Adtran executive that Adtran has no plans to expand usage of POET engines into other transceivers:

Mitsubishi Electric – Another negligible revenue research agreement. Mitsubishi not marketing any products with POET

In September 2024, POET announced a collaboration with Mitsubishi Electric. POET claims the companies are co-developing optical engine chip sets for 3.2T transceivers.

However, it appears Mitsubishi is merely allowing POET to use its lasers:

“Mitsubishi Electric will contribute its highly differentiated 400G Electro-absorption Modulator integrated Lasers (EMLs) to the project. Using its optical interposer platform technology, POET will integrate the EMLs along with drivers, optical waveguides, and other key functional building blocks to produce 1.6T and 3.2T optical engine chipsets.”

So, what appears to show buy-in from a large manufacturer is in reality POET using Mitsubishi parts in another project that will likely go nowhere. Tellingly, Mitsubishi doesn’t consider the arrangement with POET significant enough to issue its own press release. We emailed Mitsubishi for further information but received no response.

$5 Million Order: Evidence Points to Obscure Lower-Tier Partner, High Risk of Reduction or Cancellation

In October 2025, POET announced a $5m order for optical engines that was expected to be delivered in 2H26. The order represents a degree of validation as it was and still is the largest ever product order POET has announced. After the Celestial AI/ Marvell debacle, the order has taken on a new level of importance – the bull case hinges on it in our opinion. Reviewing the fact pattern surrounding the order, we believe there is a high risk of curtailment or cancellation, or that POET has misrepresented the order.

POET has discussed the order in only two press releases – the original October 2025 announcement and the Q4 2025 results press release in April. In both, POET’s language has been limited and careful. POET says the customer is a “leading systems integrator that will manufacture and sell optical transceiver modules” and was “integrating POET across it’s ecosystem”. To us, this language suggests a customer who is not currently manufacturing optical transceiver modules.

POET management has had obvious opportunities to discuss the order but hasn’t. For example, in a January 2026 interview with Photonic Integrated Circuits, POET’s CRO Raju Kankipati was asked to discuss POET’s customers. He completely ignored the $5m customer and named three immaterial, dying or dead relationships:

“We have 3 types of customers: first type is using our engines for their optical modules. For example, Adtran, Luxshare, Foxconn. These customers use our transmit and receive engines and design optical modules for high speed and datacom markets.” – POET’s CRO

Why wouldn’t Kankipati at least discuss the $5m order?

Additional clues are found in a Zacks analyst report (which POET paid for). According to the report, product shipments to “Celestial AI (now Marvell), Adtran and unnamed non-Chinese Asian customer this year to generate most of its 2026 revenue.” The non-Chinese Asian customer “has data center customers lined up, although it has not yet announced its own products and possibly never will to keep them secret.”

Why would POET management provide this detail to Zacks? We think POET’s limited discussion and caged language are red flags. You’d expect POET to tout the $5m order whenever it can, but it seems POET would rather have investors focused elsewhere.

We think a company like Accton fits the profile of POET’s $5m customer.

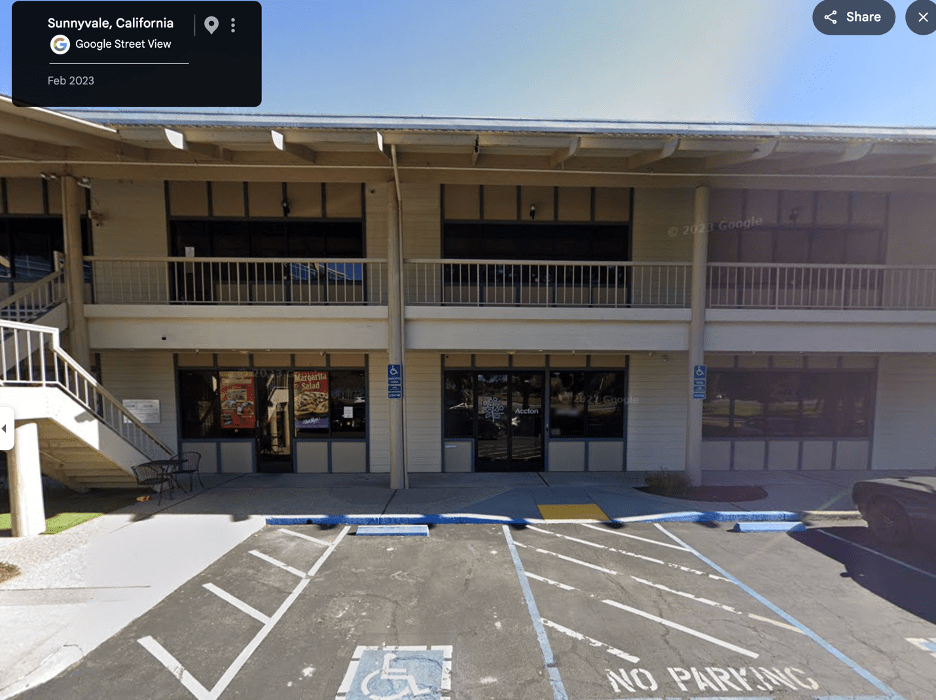

Accton, based in Taiwan, fits the description of a “systems integrator” as a white-label, original design manufacturer of networking systems and switches. Accton has an optical transceiver subsidiary known as GoldiLink which was only founded in 2024 [Pg. 19]. On its website, GoldiLink advertises two transceivers, both 800G which aligns with the 800G engines POET says it will begin shipping in 2H26. Accton has a satellite office in Sunnyvale, CA which is a 15 minute drive from the San Jose area where POET’s CEO and CRO are based.

A customer like Accton / GoldiLink would significantly increase the risk that the production order is not binding and will never be fulfilled. Judging by the quality of GoldiLink’s rudimentary website, it appears it’s not a serious manufacturer. Moreover, GoldiLink has no web presence outside of its website and a single LinkedIn post.

POET should provide transparency not only regarding Celestial AI / Marvell, but also with this $5m production order. Consider that in 2023 POET announced a $3m production order with an obscure entity that was never fulfilled (discussed below).

Lumilens Deal Appears To Be Incestuous Agreement Concocted For Circular Promotion

In May 2026, POET announced a supply agreement with Lumilens, a private company that purports to develop datacenter/AI interconnect technology. Investors reacted to the headline revenue figures in the press release, $50m initially and the potential for $500m+ over five years. We believe this partnership will join the heap of dead end agreements POET has promoted in the past.

According to the press release, Lumilens placed an initial purchase order for Electrical-Optical Interposer (EOI) based engines valued at $50m. Importantly, POET did not explain how or if EOI differs from its optical interposer technology. Lumilens was founded in 2024 – it’s barely two years old. Engineering samples from the POET-Lumilens partnership aren’t expected until late 2026, with production ramp in 2027 – product shipments won’t even occur until next year.

But we have high conviction that POET will fail to meet this timeline. The idea that this new product will begin shipping next year for this likely non-binding agreement is dubious in light of POET’s history. Consider POET’s celebrated $5m order for POET Infinity engines, products that were demonstrated at OFC 2023, yet still haven’t been delivered to the customer over 3 years later.

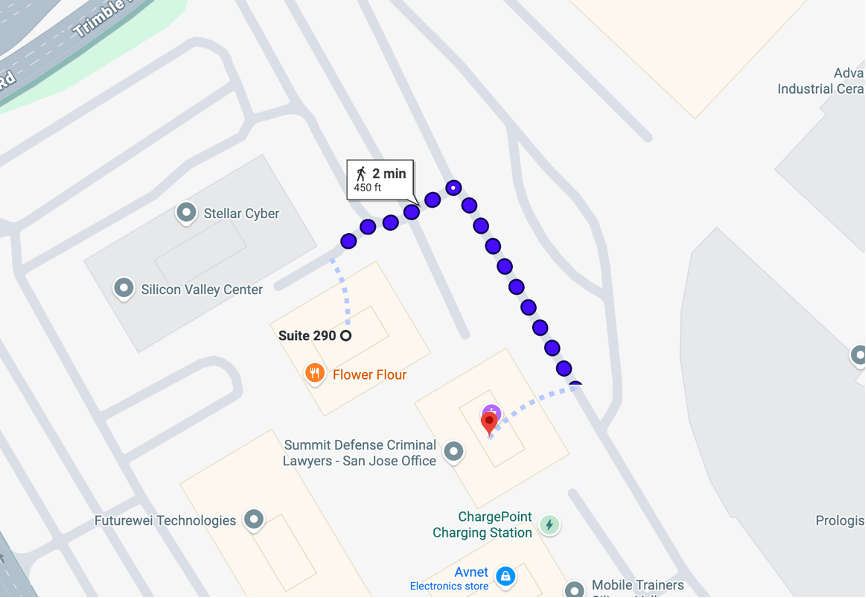

As noted above, we think POET’s unnamed $5m customer is likely Accton operating through an obscure transceiver subsidiary known as GoldiLink. The web of connections between Accton/GoldiLink and POET became more direct after the Lumilens deal was announced. Lumilens CEO Ankur Singla is a member of Accton’s board of directors. Moreover, in April 2025, Accton invested $9m into Lumilens Series B preferred stock. Strengthening the connection further, Accton and Lumilens have offices within a few hundred feet of each other in San Jose:

If Accton / GoldiLink is the $5m counterparty, we think this indicates the Lumilens deal is at high risk of falling apart as it’s simply a continuation of the $5m order, which is now an eight month old agreement that POET has yet to collect revenue for and rarely acknowledges except in the Marvell cancellation press release when it was desperate to show commerciality. Also, if Lumilens was connected to a deal involving a counterparty like GoldiLink, the signal would be extremely bearish for Lumilens’ as a credible developer of datacenter tech.

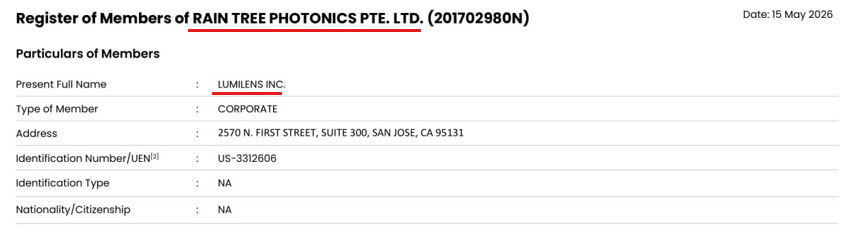

The relationship between POET and Lumilens also appears to predate the announced partnership. POET is a founding member of SHINE, a Singapore-based heterogeneous-integration R&D center that works closely with ASTAR IME, the country’s government-backed research agency. Rain Tree Photonics — now a subsidiary of Lumilens — is a direct spin-off of ASTAR IME. POET and Lumilens were connected through Singapore’s photonics network well before this deal was announced.

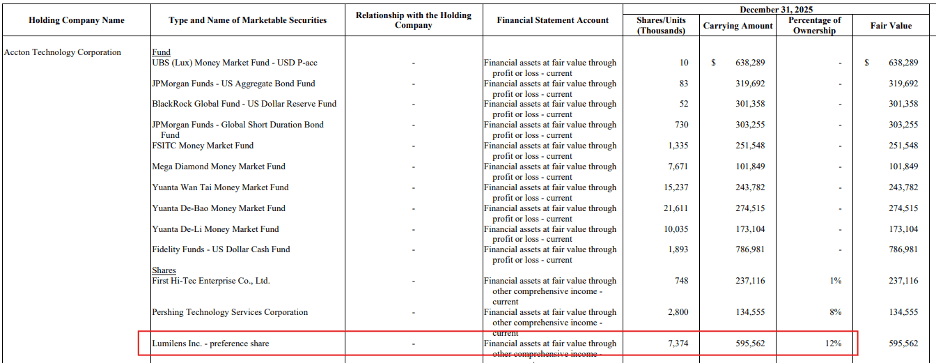

Beyond Lumilens’ intertangled relationship with Accton, we found several other questionable issues with the company. Notably, the POET partnership appears to mark Lumilens’ first-ever appearance in a press release. Despite reports that the company raised $100m last year, we could find no announcements of those raises nor any deal tombstones on the websites of its supposed VC backers Spark Capital and Mayfield. Beyond the POET announcement, Lumilens has an almost nonexistent digital footprint. The funding picture raises further questions. Lumilens sought approximately $106m from Accton in its most recent round but secured only around $9m. And while the latest financing ostensibly values the company at over $1B, Accton’s balance sheet tells a different story — carrying its Lumilens stake at 595k Taiwanese dollars for a 12% interest, implying a valuation of roughly $158m – an 85% discount to the headline number.

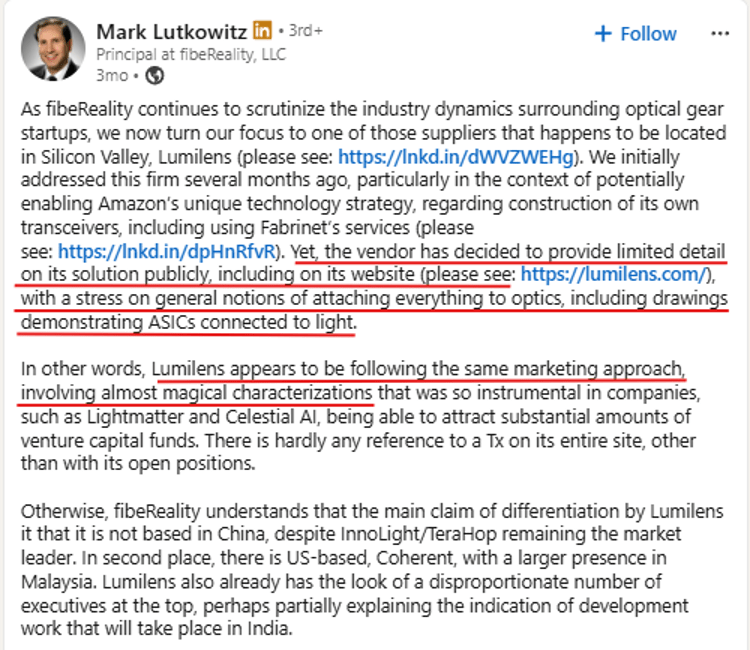

Industry participants have also raised concerns about Lumilens. In a recent LinkedIn post, Mark Lutkowitz, Principal at fibeReality LLC — a firm that tracks the optical gear industry — noted that Lumilens has provided limited detail on its solution publicly, including on its own website, while relying on what he described as “almost magical characterizations” reminiscent of other overhyped optical startups. He further observed that Lumilens’ main claim to differentiation appears to be that it is not based in China, and flagged a disproportionate number of executives at the top relative to the company’s apparent stage of development. In short, even credible industry observers appear skeptical.

Lumilens’ manufacturing claims also deserve scrutiny. On its website, the company states it has “developed highly automated manufacturing through the extensive use of robotics and AI-optimized processes” – implying proprietary, in-house capabilities. However, Cignal AI, classifies Lumilens plainly as “a startup design house for datacenter optics out of California with manufacturing in Thailand.” Thailand-based optical transceiver manufacturing, for all practical purposes, means Fabrinet. Lumilens did not build a manufacturing breakthrough. It almost certainly rents floor space from the same contract manufacturer everyone else uses.

This raises a fundamental question: why would a fabless company that specializes in design work, generates only a few million dollars in revenue, and has no publicly announced customers, commit to spending nearly half the proceeds from its most recent Series financing on $50m worth of POET products it has no apparent ability to sell?

We believe the answer is straightforward — Lumilens has no genuine intention of purchasing anything from POET. The 2.3m warrants, now worth over $30m, give Lumilens a financial incentive to lend its name to a press release. This partnership is likely nothing more than a transactional headline for Lumilens.

The warrant-for-purchase-order structure should concern POET shareholders. History offers no shortage of cautionary precedents. In 2017, Plug Power (NASDAQ: PLUG) granted both Amazon and Walmart warrants as incentives tied to hydrogen fuel cell purchase agreements. While both retailers profited handsomely from the arrangement, Plug Power shareholders were left holding the bag – the stock remains down over 90% from its all-time highs. Canoo (NASDAQ: GOEV) followed a similar playbook, issuing Walmart warrants as part of a vehicle purchase agreement; the company never fulfilled the contract at scale and filed for Chapter 7 liquidation in January 2025. Luminar Technologies (NASDAQ: LAZR) met the same fate issuing warrants to Volvo and eventually filed for Chapter 11 in December 2025 before entering a full liquidation plan in early 2026. We believe POET will face a similar situation eventually. We see no reason to believe POET will be the exception.

Rain Tree Photonics: A Dying Singapore Spin-Off Repackaged as Lumilens’ Technology Platform Weeks Before the POET Deal

Lumilens presents itself as a next-generation photonics platform company building the connectivity layer for AI infrastructure. It claims to have its own silicon photonics, mixed-signal ICs, electrical-optical interposers, and advanced manufacturing capabilities. However, the company has no patents. It has no observable proprietary technology. It has no publicly announced customers. What it does have, it bought. On March 25, 2026 – seven weeks before placing a $50m order with POET – Lumilens acquired Rain Tree Photonics, a nine-year-old spin-off from A*STAR IME, Singapore’s national Agency for Science, Technology, and Research founded to commercialize silicon photonics for the datacenter market, operating on a self-described “fabless++” model that extends beyond chip design into BOM selection, module design, and packaging. Raintree’s present full name on Singaporean filings are now Lumilens.

Over nine years, Rain Tree announced a series of partnerships that suggested real commercial traction. In 2020, it launched a 400G-DR4 silicon photonics module solution alongside MaxLinear. In 2024, it signed an MOU with Chinese transceiver company ATOP/Huatuo to commercialize 200G/lane silicon photonics engines for 1.6T and beyond optical modules. It also maintained a collaboration with JPT Lasers dating back to 2019, most recently signing a cooperation agreement in June 2025 for silicon photonic wafer-level testing.

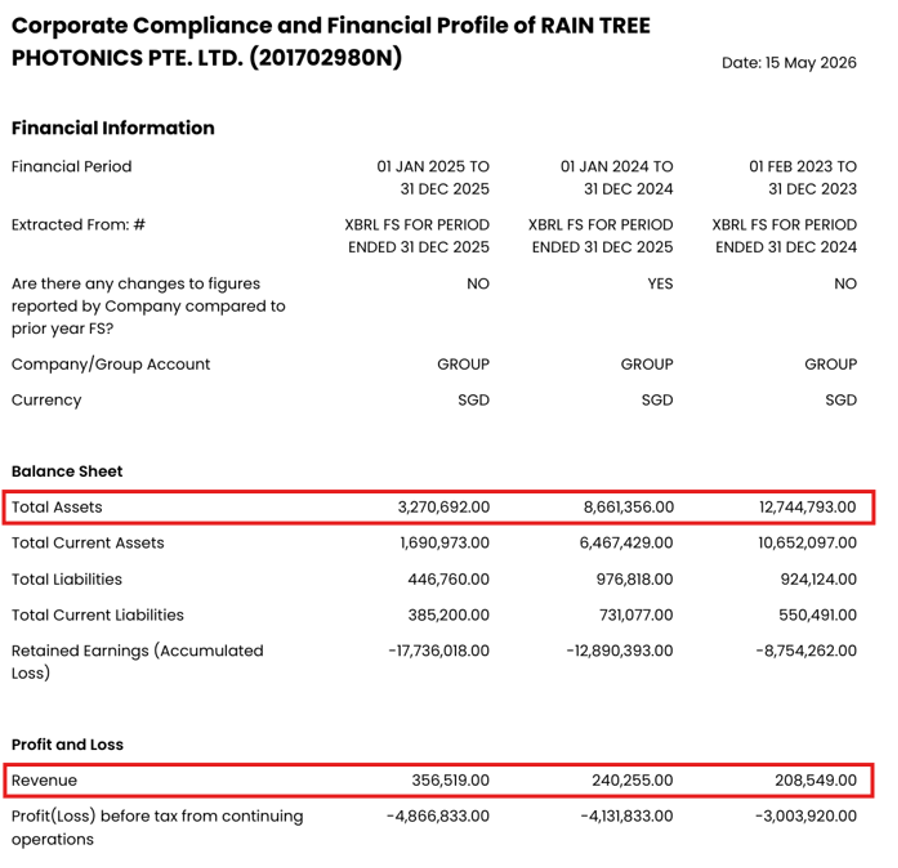

The financials tell a very different story. The Singapore filings for Rain Tree show $208k, $240k, and $356k in annual revenue across 2023 to 2025 – roughly $800k in total over three years. Total assets collapsed from $12.7m in 2023 to just $3.2m by 2025. It appears that none of the marquee partnerships translated into volume deployments.

The likely culprit is the inherent complexity of Rain Tree’s FOWLP-based photonic engine architecture. Fan-out wafer-level packaging, while mature and low-cost in electronic chip applications, introduces significant challenges when applied to complex photonic integration – including die-shift, die misplacement, and warpage caused by repeated temperature and pressure cycles during manufacturing. These issues directly limit yield and throughput at scale. By 2026, Rain Tree was a research group running out of cash with a platform no one had been able to bring to market. The $50m POET order is built on this very technology.

POET’s relationship with Rain Tree also predates Lumilens’ involvement by several years. In early 2022, POET joined the SHINE Centre — a Singapore heterogeneous-integration R&D program at the National University of Singapore involving A*STAR IME, the same body Rain Tree spun out of. The press release noted POET had worked with NUS for “a number of years.”

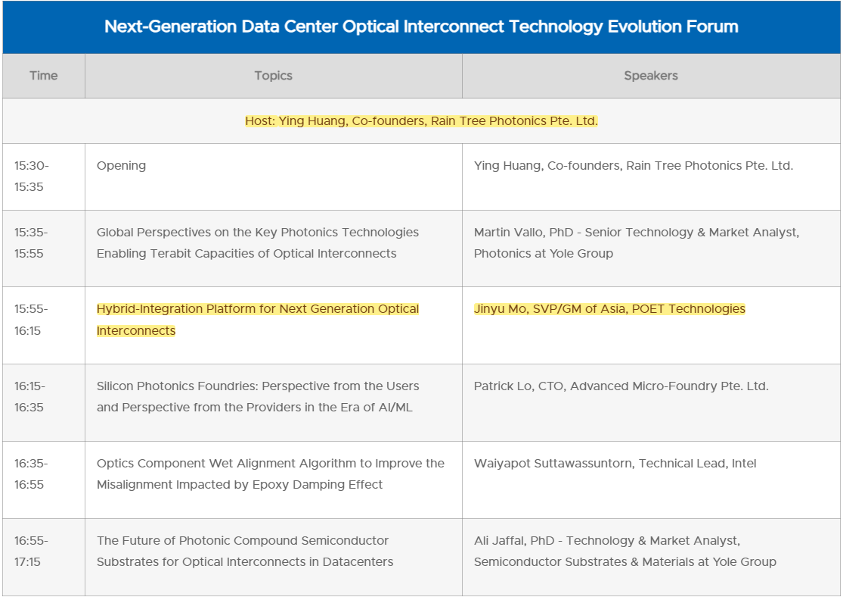

We think the relationship was driven by Jinyu Mo, POET’s SVP/GM of Asia, who describes her role as being “responsible for research and collaboration with universities, research centers and industry partners.” In March 2024, Mo presented at a “Next Generation Data-Center Optical Interconnect Technology Evolution Forum” that Rain Tree hosted.

Rain Tree’s co-founders have since joined Lumilens. Jason Liow is now VP of Silicon Photonics and Ying Huang — who hosted the very forum where POET’s Jinyu Mo presented — has also come aboard. Neither publicly lists their Lumilens role on their profiles. The picture is unmistakable: these parties have known each other for years through overlapping research programs, co-hosted events, and shared institutional ties in Singapore. There is nothing new about this partnership, in our opinion. We think POET is recycling old relationships.

Other POET Partnerships: Misrepresented or Trivial

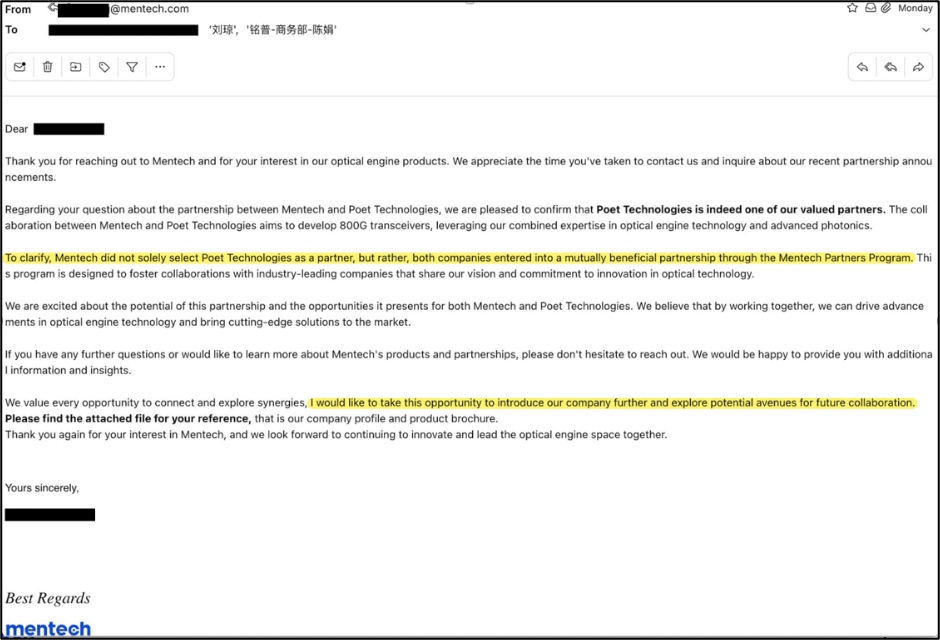

Mentech Technology – POET falsely claims Mentech selected its optical engines

In September 2024, POET announced a partnership with Mentech Technology, a Chinese semiconductor manufacturer. POET claimed Mentech “selected” POET to supply engines for Mentech’s 800G transceivers. The implication is that Mentech was so impressed by POET’s technology that it proactively requested a deal.

We contacted Mentech. A Mentech spokesperson confirmed the partnership but said Mentech did not solely select POET and rather the relationship originated through the Mentech Partnership Program, which anyone can apply for on Mentech’s website. The spokesperson even indicated Mentech would be interested in forming a partnership with us, revealing how easy it easy to engage Mentech in a partnership.

Mentech recruits partners through an application form on its website in product areas including Transceivers and Devices. Clearly, POET over-sold this trivial agreement.

Chengdu InSiGa Semiconductor Technologies – Commercially inconsequential agreement with obscure entity headed by former colleague of POET COO

The day after touting the Mentech partnership, POET announced the combination of its optical engines with drivers from Chengdu InSiGa Semiconductor Technologies, an optical device company based in China. According to POET, the combination would be used in 800G and 1.6T transceivers, demand for which Venkatesan said was “skyrocketing”.

InSiGa’s footprint is small. Only 7 LinkedIn profiles are associated with the company. The most recent news release on InSiGa’s website is from 2022.

To add context to the deal, we believe the collaboration stems from a personal relationship of Vivek Rajgarhia, POET’s former President. InSiGa’s CEO Dr. Vikas Manan has a long history with Rajgarhia. According to their LinkedIn profiles, between 2007 and 2016, Manan’s and Rajgarhia’s work history overlapped at GigOptix, Optomai, and MACOM. In 2016, Manas left to start InSiGa. Senior executives using personal relationships to foster business opportunities isn’t out of the ordinary. However, its important context for a partnership between two companies with little to no industry footprint or traction.

LITEON – POET CEO calls it a major step, LITEON President says there’s no actual business

In March, POET announced a partnership with Taiwanese electronics manufacturer LITEON to develop modules based on POET’s technology. POET CEO Venkatesan called it a “major step” and expected to have prototypes ready by end of 2026.

During LITEON’s Q1 2026 earnings presentation on April 29, LITEON’s President was asked if the company would be affected by POET’s issues with Marvell and Celestial AI. He seemed unaware of POET, but an aide apparently gave him a hint and he described an immaterial relationship [26:00]:

“So LITEON doesn’t cooperate with this company. Well, of course, with POET, there is some contact, but there isn’t actual business between us.” – LITEON President

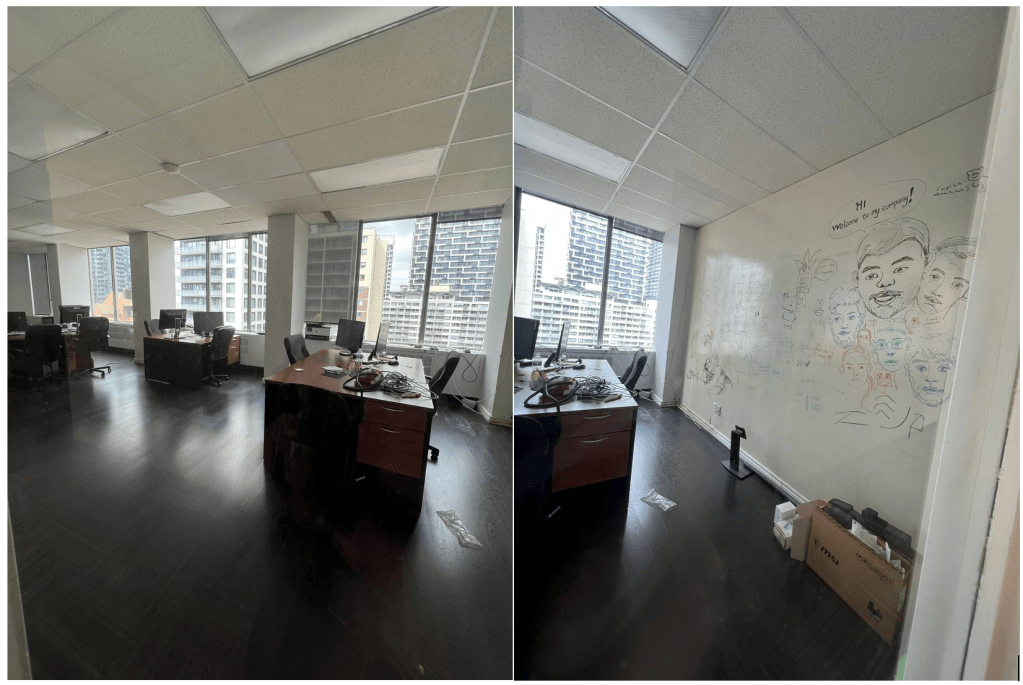

POET’s Headquarters in Toronto: Abandoned and Trashed

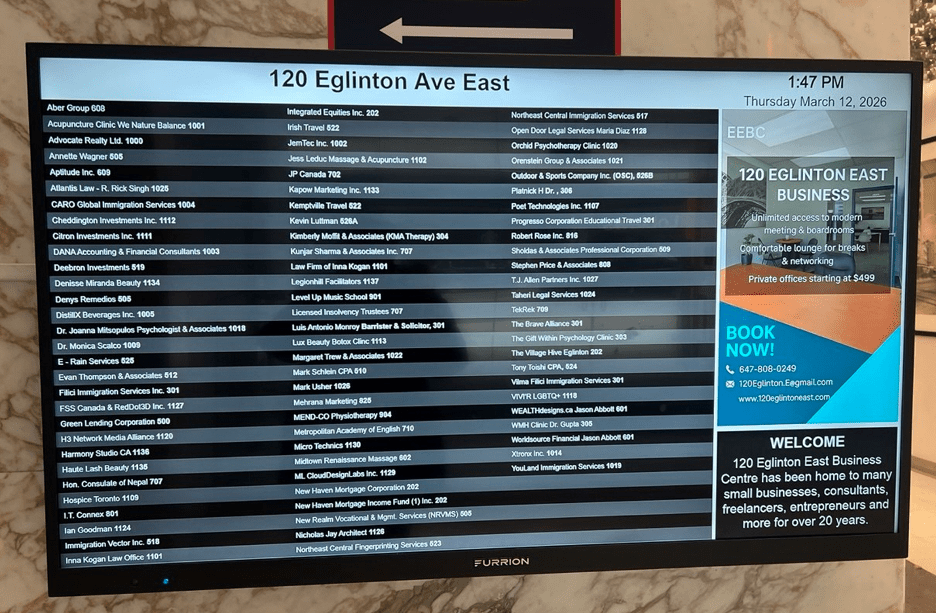

We visited the building where POET’s headquarters is located at 120 Eglinton Ave East in Toronto. The office houses the company’s finance and administrative functions, according to management.

Other tenants on the 11th floor include Haute Lash Beauty, Jess Leduc Massage & Acupuncture, and Lux Beauty Botox Clinic.

None of the offices on the 11th floor had a nameplate for POET or Suite 1107. None of the other tenants on the 11th floor whom we spoke to had heard of POET. Based on the floor plan, they pointed us to two spaces which could be POET’s office.

POET HQ – Option 1 is a closet sized room (80-100sq ft). Other tenants told us they have never seen anyone enter the space.

POET HQ – Option 2 is an abandoned, trash strewn office with dirty walls:

POET Has Promoted Near Term Commercialization Since 2013

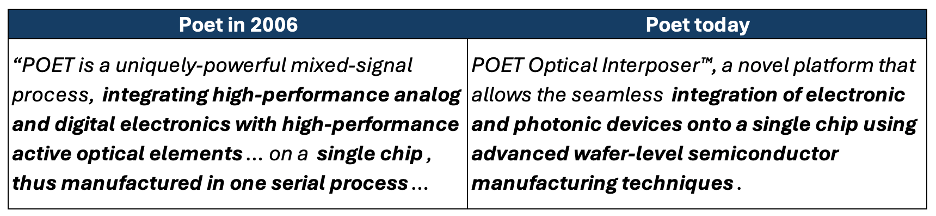

POET is developing the Optical Interposer, a technology it claims allows for passive alignment of networking chip components that normally require active (and more costly) alignment.

The company was originally the semiconductor division of Opel Solar, a solar panel firm that went public in a reverse takeover of a mining shell in 2006. Opel was working on a semiconductor fabrication technology it coined Planar Optoelectronic Technology, or POET, which had been in development since 1994. An archived version of Opel’s website from 2006 describes POET in terms very similar to those used by POET today.

In 2013, Opel Technologies abandoned the solar business to focus on semiconductors, changing its name to POET Technologies. Even then, POET made claims of imminent commercialization. The company said it was on track to introduce a fully-integrated semiconductor chip based on the POET platform by mid-2014, and that “several large-scale technology firms have expressed interest in jointly adapting POET to commercial scale implementation”.

Investor materials in 2016 promoted commercialization by 2018, advertising advantages in power efficiency, cost, and size. The story is the same today.

Dozens of partnership announcements have followed which appear to validate POET but have proven commercially worthless.

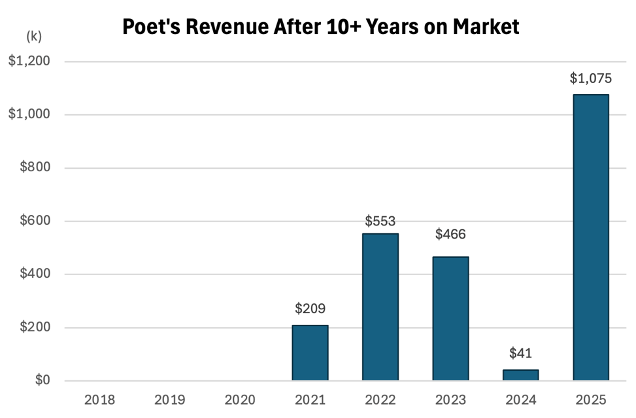

In January 2018, POET formally re-coined the technology as the Optical Interposer. Commercialization at 100G failed, as did attempts to adapt the technology to 200G and 400G. Chip revenue (revenue excluding non-recurring engineering fees) since 2018 totals $1.2m. If POET wasn’t able to get traction between 100G and 400G, why would 800G+ be different?

Before AI-related stock strength, POET sustained investor support (diluted share count up 4x since 2023) in part with vanity award schemes and low brow stock promotion.

For example, in February 2024, Canadian stock promoter McNallie Money pumped POET to their 46k followers in a YouTube video funded by CAPITALIZ ON IT whom POET paid $90k for 3 months of promo work. McNallie touts nano-caps like Hillcrest Energy ($18m market cap), Sol Global ($15m market cap) and Thumzup Media ($35m market cap). POET also employed a Toronto-based entity called LFG equities whose principle promoted the ICOs of multiple defunct cryptocurrencies (For more coverage on POET’s stock promotion, see Bear Cave, The Plain Bagel, and Wolfpack Research).

POET’s Crown Jewel Fails – JV Partner Abruptly Exits and Gets a Refund. Poet Must Now Fund 100% of Manufacturing Costs

In October 2020, POET Technologies entered into a joint venture with Xiamen Sanan Integrated Circuit, a subsidiary of Sanan Optoelectronics. The venture, named Super Photonics Xiamen (SPX), was established to manufacture optical engines and modules based on POET’s Optical Interposer platform, fulfilling anticipated demand.

Under the agreement, Sanan committed manufacturing expertise along with up to $25m in cash over two to three years, contingent on milestone achievements. POET contributed intellectual property. Financial terms implied an estimated valuation of $50m for SPX, with ownership expected to be split roughly equally once Sanan’s full investment was made.

At the time, POET’s CEO, Suresh Venkatesan, framed the venture as a pivotal moment:

“Super Photonics is both the culmination of a long path for POET and the beginning of a new phase in our growth and development as a company. We cannot overstate the importance of this moment and the depth of our commitment to making this joint venture a resounding success.”

Former President Vivek Rajgarhia described SPX as a “strong indicator of commercialization of POET’s Interposer platform” and called the ability to attract a partner like Sanan a “proud moment.” Sanan IC’s CEO was similarly emphatic, stating that Sanan was dedicating “significant capital and management talent” to the venture.

In February 2023, POET announced an agreement with Beijing FeiYunYi Technology (BFYY), a Chinese entity created to purchase engines from SPX. Public evidence of BFYY’s operating presence is limited, with its CEO, Wei Zhang, difficult to identify outside POET’s own announcement.

According to the press release, BFYY was expected to buy more than $30m of engines over three years. In May 2023, POET announced BFYY’s first purchase order, valued at $3m.

Those numbers did not translate into reported revenue. POET never generated $3m from BFYY, let alone the more than $30m contemplated over three years.

By November 2024, the SPX story had effectively reversed. Sanan withdrew from the joint venture after contributing only $7m of the $25m originally contemplated, with the final $2m coming in the second half of 2021. In our view, Sanan’s decision not to fund the remaining $18m is a clear negative signal. Whether due to missed milestones, weak commercial traction, or a reassessment of the opportunity, the outcome is hard to reconcile with the original commercialization narrative.

Not only did POET lose Sanan as a partner – it’s also paying them back. As part of the JV’s dissolution, POET is paying Sanan $6.5m over the next 5 years, or nearly all of the cash Sanan contributed into the JV.

Management presented the separation constructively, but the signal from POET’s closest partner is troubling. After 4 years with POET, Sanan had second thoughts about “dedicating significant capital” to SPX. And while Sanan was plotting its exit, POET hyped imminent large-scale commercialization while issuing stock 7 times in 2024.

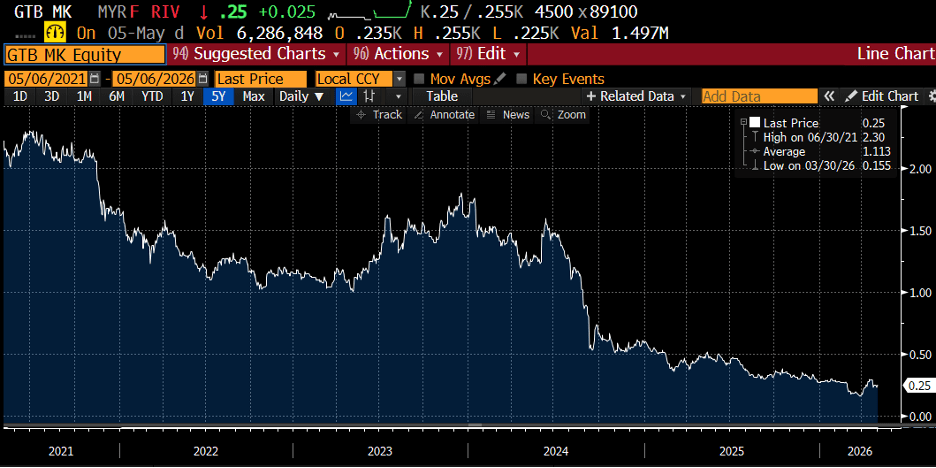

POET’s New Manufacturing Partner: Globetronics, A Financially Troubled, Scandal Plagued Penny Stock

POET attempted to paint Sanan’s sudden departure as a positive, claiming it freed the Company to expand production capacity to meet AI infrastructure demand. This idea is nonsensical – the agreement with Sanan covered optical engines up to 400G. Nothing prevented POET from engaging other manufacturing partners for products above 400G.

After Sanan’s exit, POET said it was in negotiations with several manufacturers. Those negotiations appear to have gone poorly. In December 2024, Company signed an agreement with Globetronics (MYX: GTRONIC), a troubled $50m Malaysian penny-stock plagued with controversy and a plummeting stock down 90% from its highs.

Since October 2024, Globetronics has seen the resignations of its CEO, Executive Director, and auditor (KPMG). The departure of the two senior executives may be in response to a steep and prolonged decline in Globetronics business, with negative revenue growth since 2022.

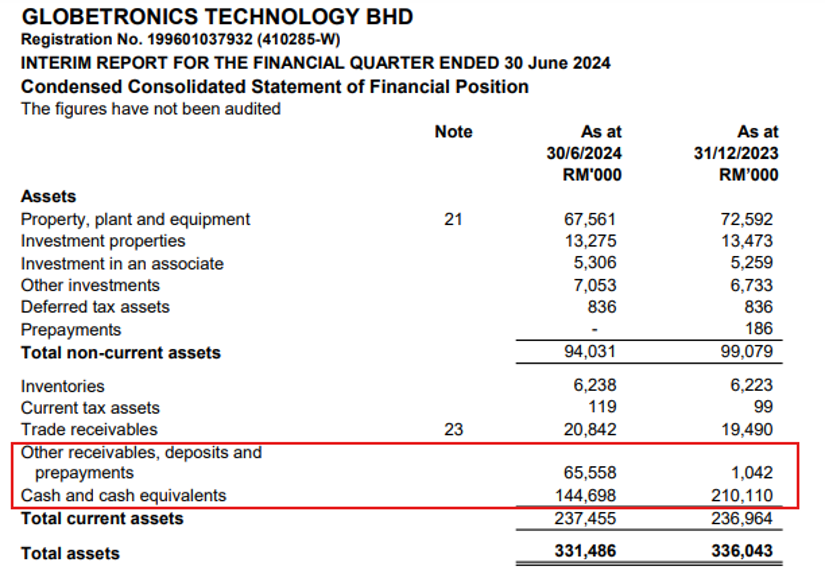

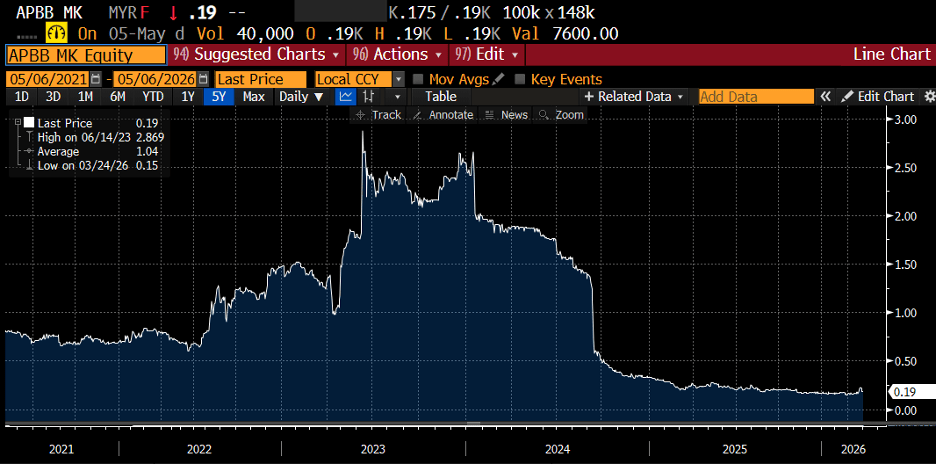

Their resignations could also be related to concerns that a new large shareholder is siphoning away Globetronics’ cash. In early 2024, APB Resources BHD (MYX: APB) bought Globetronics shares from co-founder and Chairman Michael Ng at a premium to the market. It was speculated that APB was interested in the RM200m cash on Globetronics balance sheet. Indeed, without explanation, in the quarter after APB became involved, Globetronics’ balance sheet showed cash decreased by RM65m offset by a receivable of RM65m.

In November 2024, Globetronics’ now former CEO warned that its dividend was at risk, substantiating cash concerns. The combined issues have punished Globetronics and APB shares since mid-2024.

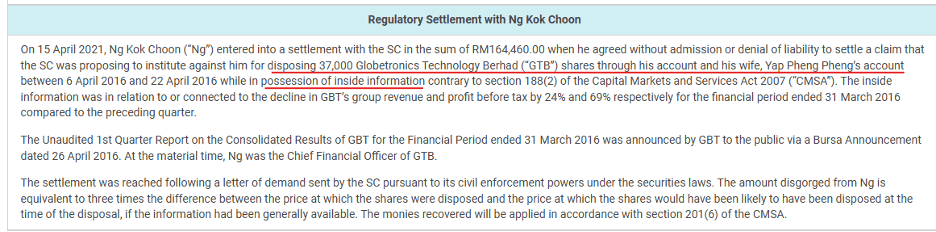

Prior to these issues, Globetronics was beset with an insider trading scandal involving its CFO, Ng Kok Choon. While in possession of inside information, Choon, who is also the nephew of co-founder and Chairman Ng, sold shares in his wife’s account before the company reported steep revenue and earnings declines.

We acknowledge that concerns related to APB and Globetronics’ cash are speculation, and that the concurrent resignations of Globetronics’ senior executives and auditor could be ill-timed coincidence. However, we’d expect that a company soon to be inundated with orders from hyperscaler suppliers (as POET assures investors) would avoid a manufacturer with so many controversies. POET could have chosen another manufacturer but didn’t.

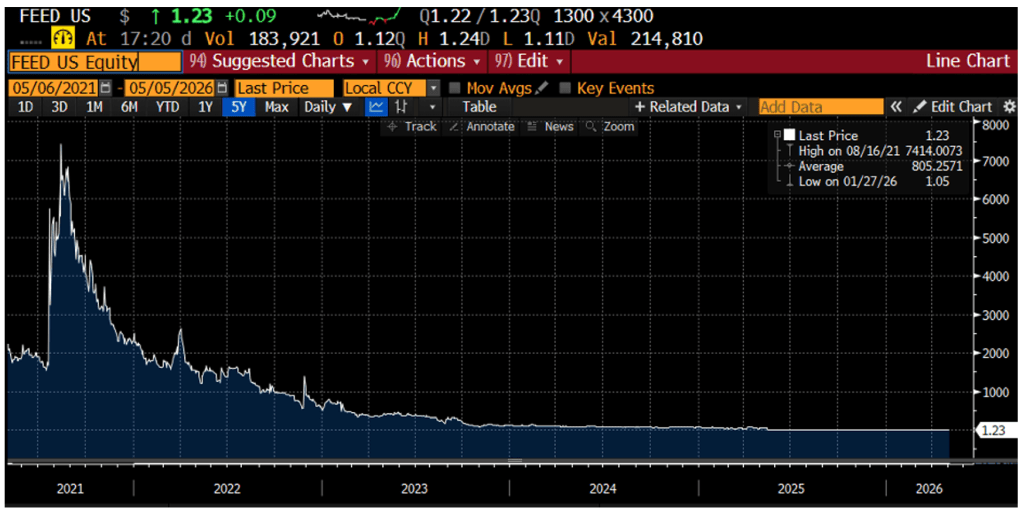

The stock of POET’s other manufacturing partner is also in a steep decline. In June 2025, POET announced an agreement with Malaysia-based NationGate Solutions (MYX:NATGATE) to assemble a custom optical engine for a “key customer.” Since then, NationGate’s stock has fallen 50%, weighed down by weaker-than-expected AI-related revenue and margins.

POET Claimed it Would Continue to Operate the JV Entity, But We Found An Entity That Appeared Defunct

After “taking control” of SPX in November 2024, POET said it would continue to operate the entity. CEO Venkatesan said,

“We can now present one face to our customers in China, exercise full control over company operations, benefit from a consolidation of SPX financial results with POET and fully implement our ‘China Plus One’ strategy.”

We found the operations at SPX were not as significant as claimed by POET. The SPX website was basic with limited functionality. Messages the Sales and Information departments using the contact page generated errors.

The phone number listed on the website was inoperable or disconnected. Multiple emails to Sales, Information, and Human Resources were unreturned.

Although POET claimed SPX was a standalone, separately registered entity with over 40 employees, our attempts to contact Sanan IC employees were unsuccessful. SPX did not have a LinkedIn page and the only profile which listed the entity is that of SPX CEO and GM Xiaozhong Zheng. Messages to Mr. Zheng were unreturned.

Photonics Expert: POET’s Technology is Expendable and a Commercial Dead End. Competitor Developing Similar Technology Went Bankrupt

“Technology Looking For a Problem…”

To better understand POET’s technology, we spoke to a senior engineer with over ten years of experience in the optical sector. The engineer worked at Rockley Photonics, a developer of silicon photonics technology very similar to POET’s Optical Interposer.

How similar? In 2021, POET CFO Thomas Mika said Rockley was POET’s closest competitor [15:30]. An industry publication from 2018 mirrors POET’s description of the Optical Interposer:

“[Rockley] says its ability to integrate electronics and photonics without compromising manufacturability or performance enables it to serve numerous emerging applications. Target markets include consumer electronics, autonomous vehicle, biomedical and industrial sectors, as well as high-performance networking optics for data centre and infrastructure networking.”

The engineer told us Rockley was trying to do in 2017 what POET is still trying to do today. However, Rockley figured out interposers were a commercial dead-end.

Senior Engineer: “What we were trying to do [at Rockley] is what POET is positioning themselves to do right now for the same market that we went after six years ago. This was 2017 to 2019.”

Senior Engineer: “[the Optical Interposer] seems like a compromise where the problem statement is not clear, and it feels like a technology looking for a problem rather than a problem looking for a solution. That’s the challenge we faced at Rockley as well. We were doing something very similar at Rockley, and we eventually decided not to pursue it in data center applications anymore because of the fact that there is no real value in data center applications, but there is value in consumer applications like LiDAR and sensing applications. That’s why Rockley Photonics went bankrupt and then it made a pivot to biosensing and different consumer applications.

Rockley Photonics filed for bankruptcy protection in 2023. Note that Rockley had substantially more financial support than POET, attracting significant venture capital, non-recurring revenue, and government grants. Rockley had enough traction in 2020 to generate $21m in annual non-recurring engineering revenue (nearly 40x POET’s best year) and in 2021, Rockley reported > $390m in total funding.

Like POET, Rockley signed a joint venture with a Chinese manufacturing company to build transceivers based on Rockley’s technology. Hengtong, Rockley’s partner, invested even more into the partnership: $42m into the JV and an additional $30m in Rockley’s equity two years later in 2019. Recall Sanan invested only $7m of $25m promised before bolting.

Senior Engineer: “Got $30 million LOI, and we created a joint venture that was publicly announced. A lot of fanfare and exact same thing. Basically, say that there is a silicon photonics angle which China will fund to build a transceiver line there. The goal [for Hengtong] was to get into the US hyperscale market before they could get to the China hyperscale market, but then the economics didn’t work out. Then Rockley got out of the joint venture and moved out of that space and moved directly into the sensing space because they realized this was not going to last. The adoption barrier was too high.”

We wondered if Rockley was too early 6 years ago – perhaps the industry is ready for the Optical Interposer technology today? The expert said no.

NMR: “During that time period, would you say that POET’s interposer technology might have made sense, but the industry hadn’t figured it out?”

Senior Engineer: “No, even then it didn’t make sense. I heard about POET during that time. Even at that time, we thought it made sense, but we thought that Rockley and POET were competitors. Having competition validated the market. We felt good that there was some competition in the market, but we thought it made sense. The conclusion was it didn’t make sense to us. I don’t know if they did something different, but based on public information, I don’t think they are doing anything different than what Rockley was doing back then.”

We asked why POET’s technology couldn’t work in the datacenter-transceiver market. The expert believed current technologies adequately fulfilled the needs of transceiver module customers:

NMR: “Why won’t Poet’s technology work in the transceiver market?”

Senior Engineer: “Because the incumbent solutions are good enough. In a transceiver market, the customers like hyperscalers that include Google, AWS, Meta, and Microsoft, they buy what are called pluggable transceivers… The existing two technologies [externally modulated lasers and silicon photonics] are able to meet everything that the customers foresee needing for the next decade. POET, with its interposer technology, it’s a hybrid between these two approaches. It’s not clear why someone would use that approach and what problem it is solving in the existing ecosystem. There is no real problem there that [POET] is trying to solve, and that’s why it was not clear to me where the market fit is for the technology within the pluggable transceiver ecosystem.”

The expert thought POET’s technology was also at a cost disadvantage compared to current technologies:

NMR: “You said cost management is key for POET’s technology. Am I understanding you correctly that the margins, when Rockley was working on this five or six years ago, didn’t add up and that’s why you decided to pivot?”

Senior Engineer: “That’s right. It was purely a cost play. There was no performance benefit. It was purely a cost play. The interposers were supposed to be a cost play. The question is, if it is a cost play, what exactly are you replacing in the existing thing that gives you that cost benefit? The pluggable cable industry is a race to the bottom when it comes to cost. If they sense that someone else is trying to pitch a low-cost solution, the incumbents will just drive down their price. It’s extremely difficult to compete with China on cost. That’s why Intel got out of that business. Broadcom got out of that business. Every US vendor got out of that business, except China.”

Based on his experience at Rockley, the engineer believed the Chinese partnerships touted by POET are often tax benefit schemes for the counterparty, for example the collaborations with Foxconn Interconnect, Luxshare, and Mentech.

Senior Engineer: “…In my experience, I can say that in China they usually fund efforts for tax benefits… What happens is the Chinese government provides tax credits that pay for the investment in new technologies. That’s a huge tax benefit that they get out of it. Some of the partnerships that they have with new players are usually funded by that. Where there is no real business case, it’s purely just the ability to get some tax.”

NMR: “POET announced a collaboration or early-stage partnership with Mitsubishi. Are these real contracts?”

Senior Engineer: “Partnerships mean nothing. I have been in this industry long enough to know what each of these means. Early-stage partnerships only mean they’re exploring the ability to jointly develop something for some new application. It doesn’t mean it’s an actual product or there’s a business case, nothing. It’s usually exploratory research.“

POET CFO Executive History: Failed Reverse Mergers

Given our view that CFO Thomas Mika was not being transparent in the Stocktwits interview which led to the recent volatility, we think his resume is worth considering.

Between 2002 and 2012, Mika was President, CEO and CFO of Tegal Corporation, a producer of computer chip manufacturing equipment. In 2011 Tegal sold its primary technology for $2m and pivoted to solar plant development, investing $2m into Sequel Power, where Mika was Executive Chairman. In 2012, Tegal wrote its investment in Sequel down to zero.

In 2011, Tegal also invested $300k into NanoVibronix, a medical device company. Mika joined the NanoVibronix board when it went public in 2015 and remains on the board today. NanoVibronix completed a reverse merger with ENVue Medical in 2025. The stock of NanoVibronix/ENVue is down 99% since inception.

In 2012, Tegal reverse merged into CollabRx, a data analytics company in genomics medicine. Mika served at CollabRx as President and CEO beginning in 2012. In 2015, CollabRx reverse merged with Medytox, a urine testing firm which later changed its name to Rennova Health. Rennova had dire financial issues: in 2016, Rennova had difficulty paying employees, was sued by its landlord for unpaid rent, and received a delisting notice from Nasdaq after its shares dropped 90%. Mika resigned as Rennova’s Chairman in 2016.

POET’s Institutional Backers Have Checkered Records – L5 Capital Positions Are Down 93% on Average

Only two active institutional investors are publicly associated with POET: MMCap and L5 Capital. Both have checkered records.

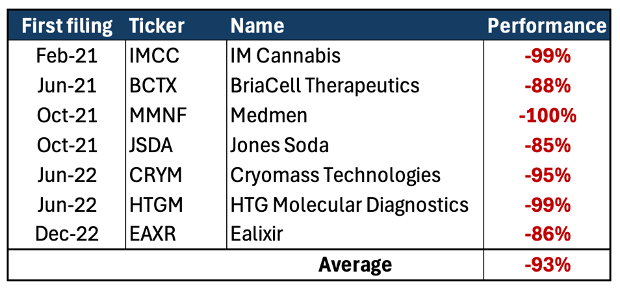

In May 2024, Cayman Island-domiciled MMCap first disclosed ownership in POET (last filed a 9.9% or 14.5m share stake). MMCap was a common financier of cannabis firms during the sector’s boom period. In 2018, Financial Post reported on the controversial tactics used by MMCap, including using bought deals to close short positions and borrowing shares from insiders to close long positions before the expiration of lock-up periods. Financial Post highlighted 8 companies financed by MMCap – since then all are down by 80% or more and 5 are down by 99%. MMCap was the sole investor in at least 5 POET offerings since 2024.

In April 2024, POET hired L5 Capital as a consultant for $1.5m plus additional fees in the event the Company completes “certain corporate transactions involving specified third parties”. A search for other companies which entered into consulting agreements with L5 Capital only produced one. IM Cannabis (NASDAQ: IMCC) engaged L5 as a consultant in December 2020. Since then, IMCC is down 99%.

L5 Capital is managed by Marc Lustig who is also the CEO of cannabis cultivator Pharmacielo. Hindenburg Research profiled Pharmacielo in 2020 (the stock is down 95% since).

In December 2024, POET announced its “intention” to raise $25m in a non-brokered offering from unnamed buyers. However, the press release footnotes mentioned “L5 Capital” and the filing on SEDAR is named “12-12_Unit_Offering_to_L5_Capital_FinalR” suggesting the investor is L5.

L5 has not disclosed ownership in POET. Filings show L5 ownership of 7 other companies, all down between 85% and 100% since L5’s involvement.

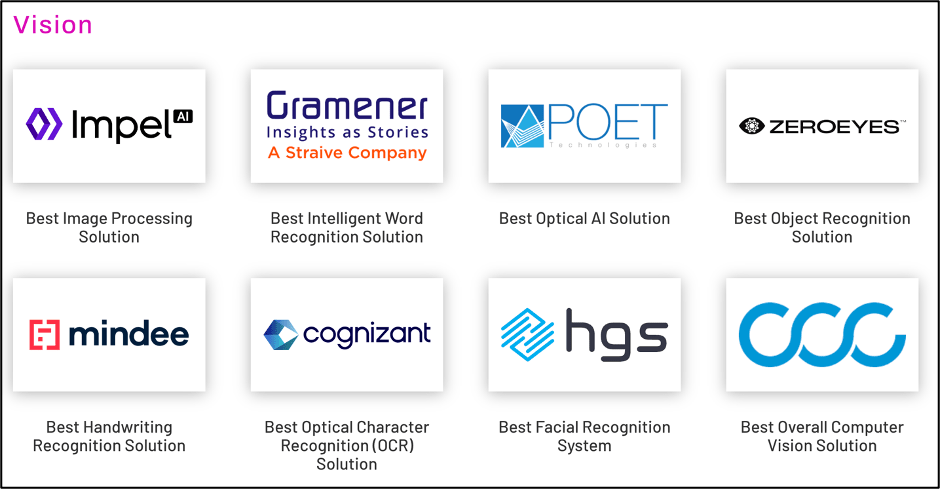

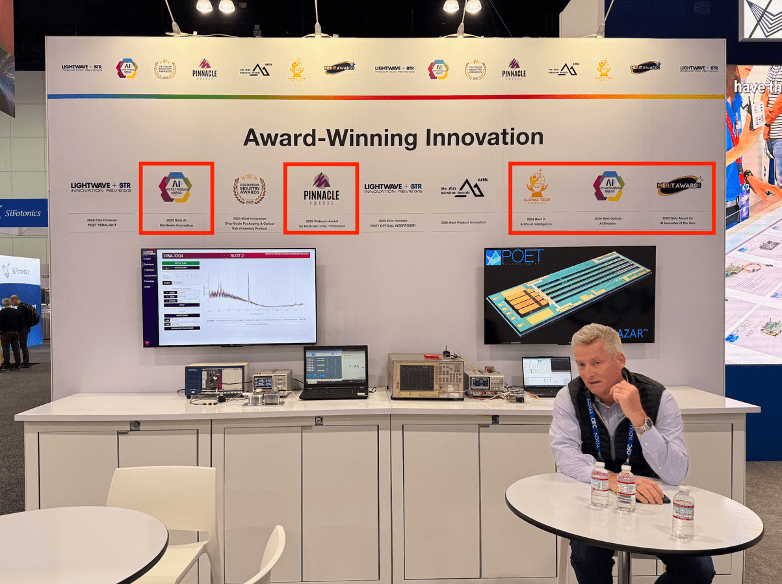

POET Touts Vanity Awards – Shenanigans of a Nano-Cap Promotion

Companies focused on selling cutting-edge optical technology typically have their hands full. However, POET has found time to coordinate vanity awards, issue shameless press releases, and conduct cringe inducing interviews.

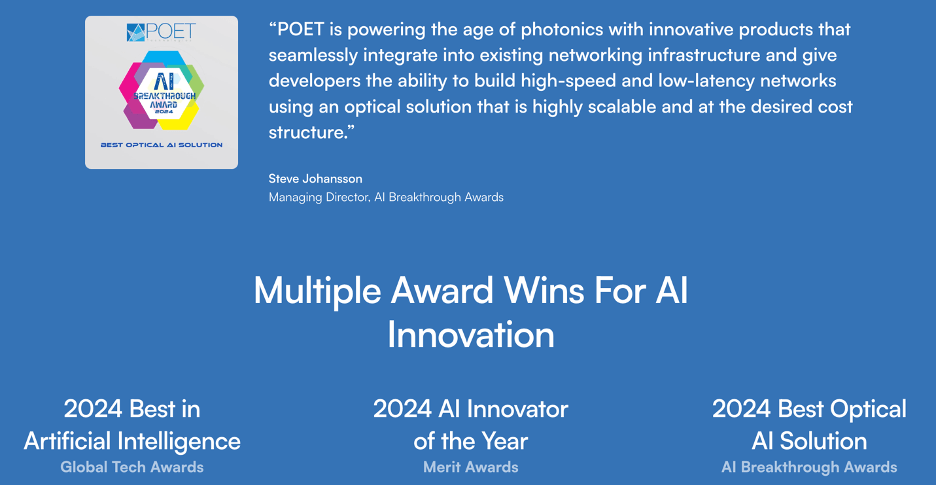

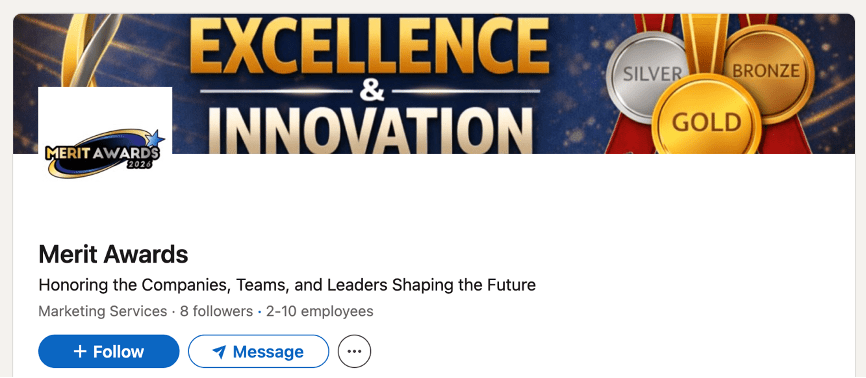

In June 2024, POET announced it won “Best Optical AI Solution” in the seventh annual AI Breakthrough Awards. In October 2024, POET won a Gold Prize for “AI Innovator of The Year” in the “prestigious” Merit Awards. Later that October, POET won “Best in Artificial Intelligence” honors at the “prestigious” Global Tech Awards. POET touts the awards on its homepage with a quote from the Managing Director of the AI Breakthrough Awards, Steve Johansson.

Spoiler alert: the awards are not prestigious. The awards and associated press releases announcing “winners” are paid marketing schemes meant to create the illusion of industry recognition. Serious companies with valuable products don’t take part.

The AI Breakthrough Awards are operated by Tech Breakthrough LLC, which is registered to Steve and Deborah Johansson. The registered address for Tech Breakthrough LLC is the Johansson’s house in San Clemente, CA.

POET won “Best Optical AI Solution” in the Vision category. Vision in this context refers to eyesight. Other “winners” in the category are developing visual recognition technologies. The year before, Best Optical AI Solution was awarded to Alitheon, a company developing machine vision technology. The Johansson’s mistook the Optical Interposer as a technology related to sight, fooled by the word “optical”.

These facts suggest the judging process at the AI Breakthrough Awards is not rigorous.

Venkatesan even did a paid promotional video celebrating the award. And just last month, POET highlighted a quote from Johansson even though he clearly has little idea of what POET does.

Then there’s the Global Tech Awards, which is administered by an entity known as Global Tech Media run by a Sirisha Lanka. Lanka’s LinkedIn header is a generic award graphic and describes him as an “award winning events coordinator”. The registered address of Global Tech Media appears to be Lanka’s home in Austin, TX. We contacted a Global Tech Awards judge who told us there was little downside in participating if an “applicant” wanted marketing and visibility.

Lanka also runs something called the Global Tech Expo which appears to be a template for another promotion disguised as a legitimate exposition. The website for Global Tech Expo is riddled with errors.

We were unable to find a registered corporate entity behind Merit Awards which awarded POET a Gold Prize for “AI Innovator of The Year” in 2024. Nor could we find information on Merit Awards’ Executive Director Marie Zander. A LinkedIn profile associated with the Merit Awards displays generic pictures of medals.

In June 2025, POET announced it won an award from Pinnacle Awards, another vanity awards operation. We were unable to find information on Pinnacle Awards’ Executive Director Kate Lang, but we know that Pinnacle Awards is associated with the Merit Awards since Pinnacle’s announcement was issued by Merit Awards.

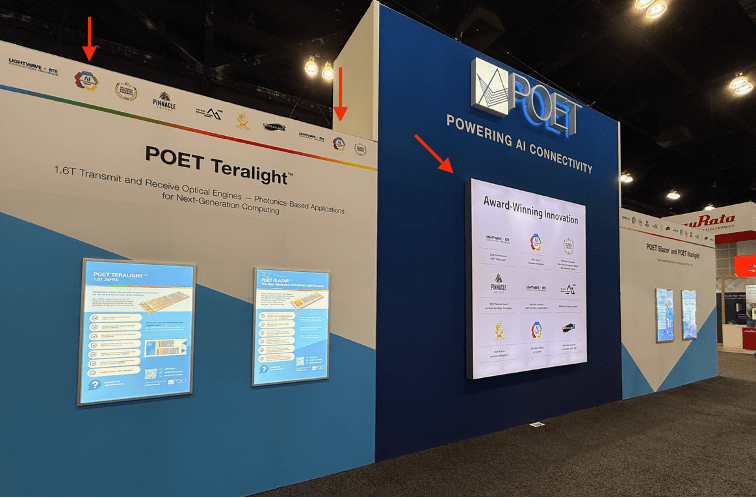

POET prominently displayed these vanity awards at OFC 2026, a troubling choice more in line with a micro-cap stock promotion rather than management’s “imminent large-scale commercialization” story.

Conclusion: Further Substantial Downside

Recent speculation of connections to hyperscaler suppliers has fueled POET stock strength but based on our research and conversations we had with POET’s most prominent alleged partners at OFC 2026 including Marvell/Celestial, Foxconn and Luxshare, we have conviction that the partnerships are misrepresented, stale or dead. POET’s $4B valuation (3700x 2025 revenue) is nonsensical for a company with significant disclosure issues selling a technology that has proven expendable. We believe there is further substantial downside for the stock.

“What’s past is prologue.”

Disclaimer

As of the publication date of this report, Night Market Research (NMR) and Connected Persons (as defined hereunder), along with or through its members, partners, affiliates, employees, clients, and investors, and/or their clients and investors have a short position in the securities covered herein (and options, swaps, and other derivatives related to these securities), and therefore will realize significant gains in the event that the price of any stock covered herein declines. NMR and NMR Connected Persons are likely to continue to transact in the securities covered herein for an indefinite period after an initial report, and such position(s) may be long, short, or neutral at any time hereafter regardless of their initial position(s) and views as stated in NMR’s research.

Use of NMR’s research is at your own risk. In no event shall NMR or any NMR Connected Person be liable for any direct or indirect trading losses caused by any information in this report. You further agree to do your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities covered herein.

This is not an offer to sell or a solicitation of an offer to buy any security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. NMR is not registered as an investment advisor in the United States, nor does NMR have similar registration in any other jurisdiction. To the best of NMR ‘s ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources NMR believes to be accurate and reliable, and who are not insiders or connected persons of the issuer covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind – whether express or implied. NMR makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and NMR does not undertake to update or supplement this report or any of the information contained herein.

NMR Connected Person is defined as: NMR and its affiliates and related parties, including, but not limited to any principals, officers, directors, employees, members, clients, investors, and agents. One or more NMR Connected Persons may have provided NMR with publicly available information that NMR has included in this report, following NMR’s independent due diligence.