- Despite billing itself as an artificial intelligence company, Veritone is primarily an advertising agency. Shares are up 1200% in the last year with strength in AI, EV and clean energy, despite Veritone’s limited association.

- Veritone’s AI offerings have failed to gain meaningful traction. The segment remains sub-scale and organic growth is below that of broad AI.

- Veritone hired an undisclosed “consulting firm” last year. The deal terms suggest the stock is grossly separated from fundamentals.

- Current stock price implies nosebleed valuations for AI segment which represents only a fraction of Veritone’s business.

- Even under very bullish assumptions, we see at least 50% downside in VERI. We think the FY2020 earnings report may be a significant negative catalyst.

“I’d rather be hated for what I am, than loved for what I’m not.” – Chuck D

Veritone (NASDAQ: VERI)generates the majority of its revenue in advertising, a mature, low-growth business, yet is valued as if it were a pure-play developer of artificial intelligence technology. Veritone shares are up over 13x in the last year, massively outperforming the Technology SPDR ETF (NYSEARCA: XLK) which was comparatively up a mere 35%. Assuming an average market multiple for Veritone’s content licensing and advertising segments, current prices equate to 65x 2021E revenue for the AI business, a non-sensical level before considering its small scale and negative margins. The most highly regarded growth SaaS names in the market, such as Palantir (NYSE: PLTR), Cloudflare (NYSE: NET) and MongoDB (NASDAQ: MDB), trade at lower multiples.

We believe the valuation disconnect stems from a misunderstanding of Veritone’s business and much of this is a result of management’s successful storytelling. Veritone has a history of aligning itself with high-profile trends, trumpeting its efforts, but minimal success actually monetizing any of it. Most recently, Veritone associated itself with EV and clean energy, sectors attracting huge levels of speculation. But based on the tepid reception for Veritone’s previous AI product offerings and the intense competition in the space, we think anyone buying Veritone for EV, clean energy or for that matter any other reason at this valuation, will be disappointed.

In addition, the details of Veritone’s relationship with an undisclosed party provide more compelling evidence that the stock has outrun its fundamentals.

We think Veritone is vulnerable in all realistic, fundamental near-term scenarios. After a massive rally on the back of hype and momentum trading, we find it hard to imagine how Veritone will satisfy the market when it reports FY2020 results on March 4. In a pattern resembling the stock’s past rounds of unwarranted strength, expect shares to reset meaningfully once investors are reminded of the dislocation between the stock and Veritone’s real business.

The Basics: Advertising Agency Wearing an Artificial Intelligence Shirt

Veritone operates three businesses: a media advertising agency, a content licensing segment and aiWARE, Veritone’s AI operating system and SaaS business. The advertising business is the core of Veritone accounting for $28m or 53% of trailing revenue (comparables include Omnicom (NYSE: OMC) and Interpublic (NYSE: IPG). Content licensing accounted for 24% and the remaining 23% was generated by aiWARE.

Veritone generates considerable losses. For the first nine months of 2020, net loss was $35m on revenue of $41m, compared to a loss of $49m on revenue of $37m for the same period in 2019. The improvement was mostly a function of cost reduction especially in research and development which was cut by $8m or 40%. As of Q3 2020, accumulated deficit totaled $268m.

The bull case for Veritone is based on two main premises. First, combining two mature businesses, advertising and content licensing, with artificial intelligence would result in synergies and reinvigorate the older businesses. Second, Veritone’s aiWARE platform and product entries into new AI use cases would drive additional revenue growth.

Veritone is at least partially hitting on the first premise. The media advertising segment has achieved ~35% revenue growth since 2018. But while the AI business is growing (~50% organic CAGR since 2017), it’s off of a very tiny base (near zero) and it remains small-scale.

Round One: Early Artificial Intelligence Hype Fades

Even though advertising has always accounted for the majority of its revenue, Veritone haspromoted itself as an artificial intelligence focused company. In the two years prior to its IPO, revenue generated from AI was only $0.6m or 3% of Veritone’s total. Yet the artificial intelligence “platform” was emphasized throughout Veritone’s IPO prospectus, as in the beginning of the business overview section [Pg.1]:

“Veritone has developed a proprietary artificial intelligence platform that unlocks the power of cognitive computing to transform unstructured audio and video data and analyze it in conjunction with structured data in a seamless, automated manner to generate actionable intelligence. Our cloud-based open platform integrates and orchestrates an ecosystem of best-of-breed cognitive engines in a wide range of classes to reveal valuable multivariate insights from vast amounts of audio, video and structured data.”

Five months after going public in 2017, Veritone rallied 400% (to an enterprise value of approximately $900m or 60x revenues) due to investor enthusiasm for AI, a bullish article in the mainstream financial press, and a series of press releases announcing Veritone partnerships against a tradeable float of only ~2.5m shares [Pg. 8].

However, none of these news stories were financially significant to Veritone and nearly all of Veritone’s $30m in revenue to that point was generated by its advertising operation. In hindsight it was no surprise when Citron Research sent a single tweet questioning Veritone’s technology causing the stock to eventually fall 70% from its peak. Veritone would later report 3Q2017 AI revenue of only $0.4m.

In summary – AI hype lacking financial substance fueled a hugerally which eventually failed. We think Veritone is currently at another point of gross misalignment between news, fundamentals and stock price.

Round Two: Law Enforcement and Government Vertical Disappoints

In 3Q 2018 Veritone launched two AI applications aimed at law enforcement and government. The products known as Redact and Identify would become part of a new Government, Legal, and Compliance (GLC) vertical. At the time, aiWARE revenue was only ~20% of Veritone’s total. Investors were hoping GLC would be the source of growth that would push AI into a large–scale business. Management enthusiastically promoted GLC, guiding that it would be largest business within the aiWARE SaaS segment:

“In addition to that growth, the activity level and the opportunity pipeline in our government, legal and compliance business are both expanding rapidly, giving us further confidence that our revenues from GLC will eventually eclipse, our M&Es SaaS revenues, even as revenues in our M&E business continued to grow off its strong base.” – CEO Chad Steelberg, 4Q2019 earnings call

However, at the end of 2019, GLC was generating less than 2% of the Veritone’s total sales ($0.9m for the year). In 2020 Veritone announced the signing of two GLC deals: an agreement in April with the Pemberton Township for Veritone’s redaction software, and a contract signed in May with the U.S. Department of Justice for aiWARE’s transcription functionality.

Similar to the post-IPO announcements, both contracts were of little financial value. The DOJ agreement, an “indefinite delivery indefinite quantity” contract, has only paid Veritone $850. And Pemberton is a small township in New Jersey with a population of only 27k. How much could a contract be worth?

Exhibit 1. Erratic growth in government vertical

Source: Company filings

Yet both announcements contributed to a ~400% rally in shares between April and June. Which in turn helped Veritone qualify for inclusion into the Russell indices, forcing additional demand for the stock by tracking funds.

The Redact product in particular appears to be well-received by law enforcement and Veritone has booked hundreds of demonstration sessions and dozens of trials. However, Redact and the other products in the GLC vertical have struggled to grow, remaining only a minor part of the Veritone’s overall business: through the first three quarters of 2020, GLC only accounted for $1.2m or 3% of revenue, up from $0.8m or 2% in 2019. Indeed, last year Veritone softened its bullish tone on GLC:

“And GLC, we think it’s going to grow at a faster pace, but frankly, there’s no internal concern about having to have GLC exceed M&E. Frankly, we’re trying to serve customers in both of those markets and see them kind of developing somewhat independently. There’s not a scarcity of resources that needs to be balanced between those two.” – CFO Pete Collins, 2Q20 earnings call

Round Three: EV and Clean Energy?

More recently, Veritone pivoted into clean energy. And in a familiar pattern, a series of press releases announcing developments with little financial impact contributed to a large rally in the stock:

- In October 2020, Veritone issued a press release touting the potential of aiWARE when applied to clean energy use cases. Veritone announced four “flagship solutions” including Forecaster which “accurately detects and predicts energy supply, demand and price.”

- In November 2020, Veritone issued a press release announcing it was awarded three new patents in “renewable energy optimization”, publishing a two-page summary of its battery optimization technology with the Tesla logo despite there being no formal relationship between the two companies (we confirmed this with investor relations).

- Later in November 2020, Veritone announced aiWARE would support NVIDIA’s processors. But GPUs like those produced by NVIDIA have long been the standard processors for AI.

(The battery optimization effort appears to be adapted from technology from Atigeo, which Veritone acquired for $3m in 2017. Atigeo was a VC-backed big data analytics company that applied “Hamiltonian learning technology” in artificial intelligence.)

The energy vertical is still only a minor part of Veritone’s revenue, generating $0.4m or 2% of sales in 3Q 2020, but we expect the energy vertical to follow a similar pattern to the “AI for law enforcement” and GLC efforts.

Exhibit 2. Veritone information sheet on EV product using Tesla logo

Source: Veritone

Veritone’s entry into clean energy has coincided with the remarkable, ongoing rally in the sector. VERI shares have followed in sympathy despite no real evidence of a significant change in its business. We suggest investors consider the early stage of Veritone’s energy effort, especially in the context of Veritone’s experience with GLC.

Consulting Agreement: More Evidence That Price Is Disconnected From Fundamentals

In April 2020 Veritone entered into a “consulting agreement” with an undisclosed firm. Veritone paid the firm 450k warrants [Pg.11], 50k of which would vest immediately and the remaining 400kin three equal tranches of 133k. The first tranche would vest based on a “market condition” and the second and third were tied to “performance goals”.

It’s noteworthy that Veritone would offer almost 2% of its outstanding shares to an undisclosed “consulting firm” for work not specifically highlighted. Furthermore, the compensation structure provides further evidence that the stock has far outrun Veritone’s fundamentals.

The “market condition” linked to the first tranche was most likely a stock price and “performance goals” likely refer to a fundamental target, such as revenue or margins. Both targets were set at the same time – for example a $15 stock price and $300m in annual revenue. In the third quarter 10-Q [Pg.11], it was noted the market condition was met and thus the first tranche of warrants was exercisable (between April and July 2020, Veritone shares rallied from $3 to almost $20, unexpectedly triggering the first tranche of warrants).

Meanwhile as of 3Q 2020, Veritone is valuing the warrants tied to performance goals at $0“because the achievement of such performance goals is not yet considered probable.” Not much in the business has changed since then, so we fully expect the performance warrants will still be valued at $0 at the next quarterly report.

Valuation – 50% Downside in Bull Case

Most of the excitement around Veritone is for aiWARE which isn’t surprising. Consider high profile artificial intelligence IPOs like Palantir (NYSE: PLTR) which went public at $7.25 last October and has since tripled in price. Or look at C3.ai (NYSE: AI) which priced its December IPO at $42 and is now trading at $120. Advances in machine learning alongside a huge increase in unstructured data production, has created new opportunities and markets.

But there’s a significant difference between what Veritone is doing in AI versus what companies like Palantir or C3.ai are doing. The latter are developing proprietary cognitive engines, machine learning algorithms and customized enterprise artificial intelligence solutions. Veritone aiWARE’s is an operating system for AI engines developed by pure-play AI firms and large-scale tech companies like Microsoft, Google, and IBM. While Veritone develops a handful of applications with relatively small, highly specific use cases (recall GLC) that operate within aiWARE, its mainly an aggregator and distributor of artificial intelligence technology.

That’s not to say Veritone’s aiWARE doesn’t provide value.However, aiWARE is currently priced at a significant premium, above the most advanced and fastest growing names in AI, despite years of underwhelming demand for aiWARE and Veritone’s applications. Veritone’s is an AI middleman and in our view, current prices misjudge the actual value produced and the potential market.

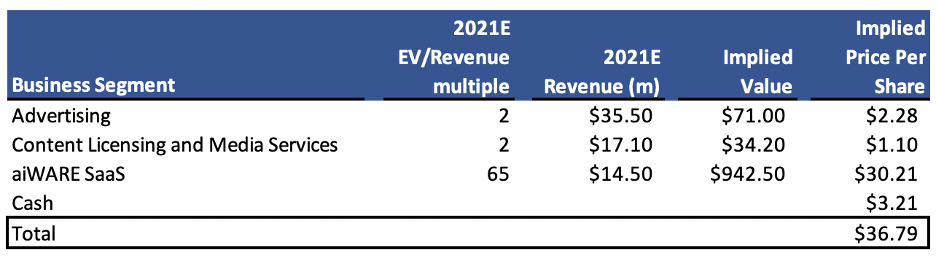

To illustrate how overvalued Veritone is relative to comparable firms, consider Veritone’s three segments separately. Media advertising is a mostly penetrated, low-growth industry with profitable comps trading at an average 1.4x EV/Sales multiple. Veritone acquired its content licensing business when it bought Wazee Digital for $15m or 1.2x recurring revenue. Applying an above average multiple to both businesses and backing into Veritone’s current valuation implies a 75x multiple for the aiWARE segment.

Exhibit 3. Current price implies extremely high multiple for aiWARE

Source: Company filings, analyst research

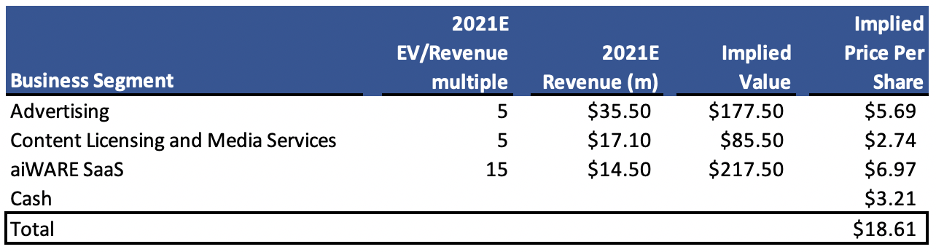

In a bull case we can optimistically assume synergies between Veritone’s AI business and its advertising and content licensing segments. Applying a far above market 5x multiple to those segments and the average industry 15x multiple to aiWARE (despite the fact that Veritone’s is more of a distributor than a developer of AI technology), produces a value of $17 per share, 50% below current levels.

Exhibit 4. Bull case – 50% downside

Source: Company filings, analyst research

We think the Q4 earnings report has the potential to be a significant negative catalyst for the stock. Investors will be reminded that aiWARE has been on the market for over three years and is still only expected to generate $15m or 22% of 2021E revenue, and that the GLC vertical which Veritone has been promoting for several years remains only 3% of the business. The figures are especially stark considering Veritone’s current $1bn enterprise value.