- Zentek, a long-floundering former junior mining company, claims it formulated an anti-viral ink that may generate billions in the face mask market.

- ZEN claims strong interest from multiple parties, but we find its only commercial partner is best described as a “mom-and-pop” operation whose parent is a children’s toy manufacturer.

- We sent an investigator to ZEN’s manufacturing facility. Photos showed minimal activity in a nearly empty warehouse, contradicting ZEN’s claims that it would soon produce ink for hundreds of millions of masks per month.

- We uncover that a former technological partner alleges ZEN stole the ink technology, filing a lawsuit alleging breach of contract. The lawsuit (undisclosed to investors) seeks to prevent ZEN from selling the ink, monetary damages, and disgorgement of profits.

- We have reported ZEN’s non-disclosure to the Ontario Securities Commission as we believe the lawsuit is material information and ZEN may be in violation of securities regulations.

- ZEN’s management team lacks relevant healthcare experience and education, substantiating the allegations in our view. ZEN’s Head of Science and Research is a pastor with a doctorate in Ministry.

- ZEN only has authorization in Canada, but projects profitability based on a global TAM estimate derived from an obscure, cherry-picked study which projects unit usage 4x higher than an estimate from Johns Hopkins University.

- Anti-viral masks are not new. A large manufacturer of a similar anti-viral coating exited the business reporting a market flooded with competition. Despite 2021E revenue and EBITDA of $63m and $6m respectively, the comparable is valued 60% below trivial-revenue ZEN.

- Given its premium valuation, a weak end market swamped with cheap supply and the undisclosed IP conflict, we believe ZEN is uninvestable.

Disclosure: We are short Zentek. Please see full disclaimer at bottom of report.

Executive Summary

March 8, 2022 – Zentek (TSXV: ZEN) (“the Company”) is a $320m (all figures in CAD) self-described IP-development and nanotechnology company focused on healthcare. ZEN shares are up over 1,000% in the last two years on excitement for its entry into the personal protective equipment (PPE) market with a graphene-based coating effective against Covid-19. We believe management and investors have misjudged the market opportunity and ZEN’s valuation has outrun all realistic commercial scenarios. Even more concerning is that investors are unaware of considerable intellectual property risk.

We find that a former partner alleges ZEN stole the ink technology during a brief collaboration in 2020. The UK-based nanomaterials company has filed suit in Ontario Superior Court seeking to prohibit ZEN from selling the ink and disgorgement of any profits. ZEN has not disclosed the lawsuit in possible violation of securities regulations. We have reported ZEN’s non-disclosure of the lawsuit to the Ontario Securities Commission. The former partner alleges a pattern of blatant self-dealing by ZEN.

We have not found evidence of ZEN’s IP related to the technology as it has not filed a full patent application in any jurisdiction. But even in the unlikely event that ZEN owns unencumbered rights to the technology, the stock is trading at untenable levels. ZEN’s current valuation is predicated on the “tiny share of a large market equals huge profits” conceit, but the company could not have timed its entry into the face mask market any worse with increasing vaccination rates, fading mask mandates, a market excessively stocked with cheap overseas supply and waning government support for the industry. And while ZEN touts a global opportunity, its masks are only authorized for sale in Canada.

Since its founding over ten years ago, ZEN has repeatedly pivoted without success. ZEN began as a junior miner before shifting to graphene production and trendy sectors such as clean technology and green energy. Healthcare and Coronavirus are its latest iterations (despite having a management team nearly devoid of relevant healthcare experience), but as with other “covid-plays”, we expect significant downside in ZEN’s shares as the hype fades and reality sets in.

We expect the stock will return to levels seen before ZEN announced formulation of the covid-killing ink as the consumer PPE market will not support even a fraction of ZEN’s current valuation. Nor will its other very early-stage commercial efforts in similarly crowded product areas. The downside is much lower if the IP risk materializes.

ZEN Touted Aggressive Production Targets While Its Manufacturing Facility Sat Nearly Empty

Until two months ago, ZEN was touting progress towards producing large quantities of its biocidal ink known as “ZENGuard”. In September 2021 we sent an investigator to Canada to visit the company’s manufacturing facility in Guelph, Ontario. The only discernable equipment in the building were stacked containers of graphene oxide (which ZEN purchases from a third-part party despite owing its own graphite mine).

Exhibit 1 – Investigator photos of ZEN’s manufacturing facility

Compared to pictures of the facility from November 2020 when ZEN signed the property lease, and photos tweeted by ZEN Chairman Francis Dubé in February 2021, it appeared that other than the erection of a wall, little progress had been made, contrary to ZEN’s representations.

Exhibit 2 – Photo of manufacturing facility tweeted by ZEN’s Chairman in February 2021

No surprise that ZEN repeatedly pushed back production targets. In March 2021, the company told investors it would have capacity to produce ink for 800 million masks per month by November. In August, this was pushed to Q4 2021 – Q1 2022. In September, the target was moved to end of 2021 [2:00] and then to February 2022 [2:30].

The aggressive production targets implied demand for ZENGuard coated masks which in-turn implied significant near-term revenue for ZEN, exciting investors and supporting the stock. While disseminating the ambitious production targets throughout last year, ZEN conducted two offerings raising a total of $37m.

Upon reviewing the prospectus for the second offering, it appears regulators at the Ontario Securities Commission asked the company to update the targets. In response ZEN completely abandoned them, blaming “variables including, without limitation, the timing of completion of its industrial scale plant and evolving production methods.” ZEN was forced to lower the offering price by 11% due to this and other revisions, the most significant being a complete write-off of a graphite mine it was carrying at $26m for years and had just reaffirmed in quarterly filings only a month prior.

In ZEN we see a pattern of missed guidance and inadequate disclosure as we discuss below. We don’t believe ZEN will ever be producing hundreds of millions of masks per month due to a lack of demand – a realization that will become clear when revenue and margins are fractions of those implied.

ZEN’s published target of nearly 10 billion masks per year insinuates demand to meet that level but we think true demand, as described by other masks manufacturers below, is relatively minuscule and it’s questionable if the market can support new manufacturers at all.

ZEN’s Manufacturing Partner, Trebor Rx: A Literal “Mom and Pop” Shop

ZEN announced a “binding letter of intent” with Ontario-based Trebor Rx in November 2020. The press release described a one-year agreement in which Trebor would purchase enough ZENGuard to coat “a minimum of 100m masks/filters”. The deal appeared to substantiate demand, but we found Trebor Rx’s size and commercial record unimpressive.

Trebor Rx, founded in 2020 by Canadian toy manufacturer George Irwin and his wife, began as a mask distribution business supplied by Irwin’s contacts in China. In late 2020, Trebor began manufacturing its own masks and by July 2021 claimed to be manufacturing 10m masks per month. Trebor Rx only lists 7 employees on LinkedIn.

ZEN claimed Trebor was bound to purchase ink for a minimum of 100m masks and filters. But ZEN’s Director of Investor Relations, Ryan Shacklock, confirmed to us that the agreement was not binding, meaning Trebor is not obligated to purchase any amount of ink beyond the initial order delivered in September. ZEN only officially made this correction six weeks after the initial announcement in an amended MD&A (but not before attempting to raise $30m in November 2021).

ZEN could sign deals with larger manufacturers, but it’s been over a year since the company announced development of the ink and ZEN has only managed to sign the deal with Trebor.

While we don’t believe the mask or wider PPE market can support ZEN’s $320m valuation, fundamental concerns may not matter in the end since, if a former partner’s allegations are true, ZEN may not own the technology backing ZENGuard.

Previously Undisclosed: Former Partner Alleges ZEN Stole Ink Technology, Currently in Legal Dispute

In April 2020, ZEN announced a collaboration with UK-based Graphene Composites Ltd. (GC) to develop an anti-viral ink coating for PPE. This was the first time ZEN mentioned the possibility of using graphene to create an anti-viral coating. Less than six weeks later, ZEN quietly disclosed the termination of the partnership at the bottom of a press release.

Exhibit 3 – ZEN June 2020 press release

We found it odd that less than three months later ZEN announced development of a “graphene-based ink” active against COVID-19. How did ZEN manage to formulate an anti-viral compound so quickly?

Early in our research, we asked Shacklock and Dubé why ZEN ended the partnership. Shacklock told us ZEN felt it was not receiving adequate benefit for its contributions under the deal terms. Dubé essentially told us the same thing:

Graphene Composites wanted us to do all the work and they get the patent… GC is all talk and no commercial prospects… they got nothing and will never get there.

Zentek Executive Chairman Dr. Francis Dubé

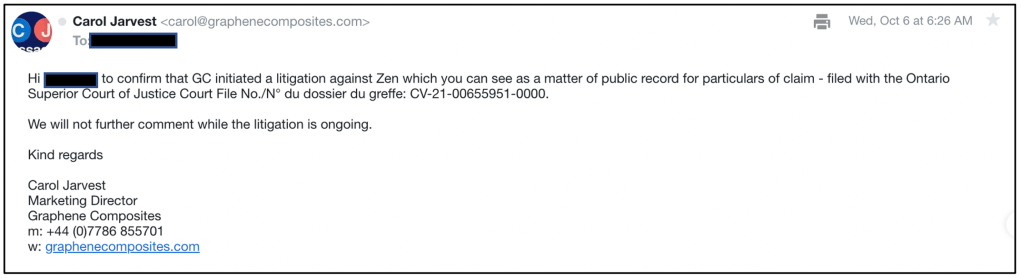

GC feels differently. We spoke with GC representatives who allege that ZEN stole the technology, characterizing the situation as “tied up in a severe legal battle”. Indeed, in January 2021 Graphene Composites filed a lawsuit in the Ontario Superior Court of Justice (File No. CV-21-00655951-0000).

Exhibit 4 – Email from Graphene Composites co-founder

Exhibit 5 – Graphene Composites v ZEN, 2021

GC is alleging breach of contract, breach of confidence, civil conspiracy, and tortious interference. It is seeking a permanent injunction to prevent ZEN from selling the ink, monetary damages for development delays and reputational harm, and disgorgement of all profits made by ZEN resulting from ink sales.

Lawsuit Alleges a Pattern of ZEN Self-Dealing and Bad Faith

The lawsuit alleges and describes in detail a brazen pattern of deception by ZEN. We recommend current shareholders and anyone considering ZEN as an investment read the documents which we make available here. GC is making serious charges and provides a compelling sequence of events to support its claims, citing emails, conference calls, and signed documents involving a third party. One hundred pages of emails and documents are available here.

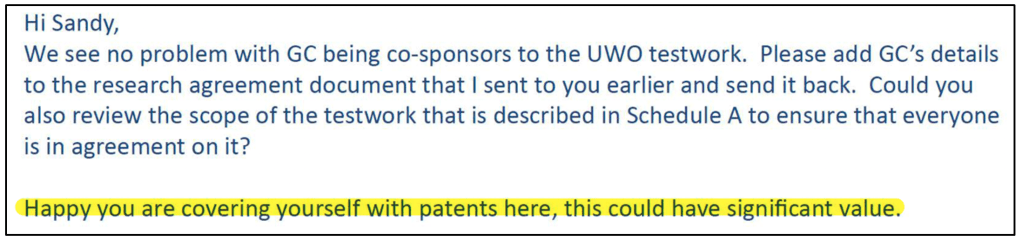

GC began working on a graphene-oxide ink with Brown University and the UK Centre for Process Innovation in the Fall of 2019. With the onset of the pandemic, GC shifted this effort towards development of a virucidal ink. In a March 2020 press release, GC invited the industry to collaborate, and offered to provide a white paper covering general information about the ink to interested parties. The next week Dubé sent an exploratory email to GC CEO Sandy Chen in which he acknowledged the graphene ink technology is owned by GC.

Exhibit 6 – Excerpt of email from ZEN CEO Dubé to GC CEO Chen (April 5, 2020)

What struck us most about the lawsuit was the description of ZEN’s alleged blatant self-dealing and deception. As alleged by GC, Dubé and ZEN CEO Greg Fenton were continually prodding for technical information about the ink, stressing an urgency to qualify for Canadian government funding for PPE production (in the end ZEN never received funding from these programs). As is evident in the emails provided by GC, the technical information consistently flows one way – from GC to ZEN.

Two weeks after the initial contact, both parties agreed that ZEN would be a main supplier of the ink’s graphene oxide silver/nanoparticle base. Dubé also asks Chen how GC was protecting its IP.

Exhibit 7 – Excerpt of email from Chen to Dubé (April 23, 2020)

Exhibit 8 – Excerpt of email reply from Dubé to Chen (April 23, 2020)

Work was continuing throughout this period, with ZEN attempting to synthesize the ink and arrange testing while GC managed the technical aspects of formulation. Dubé eventually suggests and both parties agree upon a joint press release. However, ZEN’s press release omits that GC formulated the ink and uses incorrect technical terminology. As shown in emails, GC asks ZEN to correct the error which Dubé acknowledges and says will be corrected in the version on its website. Dubé also comments that ZEN’s stock price reacted positively.

Exhibit 9 – Graphene Composites’ April 2020 press release excerpt

Exhibit 10 – ZEN’s April 2020 press release neglects to mention that GC formulated the ink

ZEN never corrects the errors. After Fenton sends an email in early May inquiring again about GC’s patent protections, ZEN stops responding to Chen and GC’s emails. Finally on May 23, 2020, Dubé explains by email why ZEN has been non-responsive:

…radio silent because we have been reconsidering our partnership with Graphene Composites… Furthermore, ZEN no longer wishes to continue a relationship with Graphene Composites because the two parties are clearly not aligned as to the terms of their existing and future relationship.

Zentek Executive Chairman Dubé

Two weeks later ZEN issues the press release disclosing the end of the GC collaboration.

As alleged in the lawsuit, GC learns that ZEN convinced the University of Western Ontario (UWO) to cut GC out of a three-party research and testing agreement that both GC and ZEN signed. During this time ZEN allegedly promised testing results from UWO, but ZEN kept the results for itself.

To summarize the allegations, ZEN:

- Stole the ink technology.

- Took advantage of GC’s altruistic willingness to share confidential information during a pandemic.

- Issued a misleading press release which induced investors to buy ZEN stock.

- Conspired with the UWO to cut GC out of an already agreed upon testing framework.

We asked ZEN investor relations for comment on the allegations, and why the lawsuit has not been disclosed. ZEN IR has not responded to our March 3rd email.

It’s important to note that ZEN never mentioned work on anti-viral inks (or any ink) before its partnership with GC. And that’s not surprising since it lacks the expertise to develop such a technology, in our view.

ZEN’s Management Team Lacks Relevant Experience: VP of Science Is a Pastor

Graphene Composites’ management team includes scientists and physicians with educations and work experience relevant to nanomaterials and healthcare. It’s Chief Technology Officer, Dr. Steve Devine, has a PhD in nanotechnology and held senior scientific positions at several organizations including Principal Scientist at the Graphene Applications Centre within the Centre for Process Innovation. GC has two medical doctors serving as advisors, both with experience in senior public health roles including serving on the Emergency Physicians National Board of Directors, and Acting Medical Director for the US Department of Justice, Federal Bureau of Prisons.

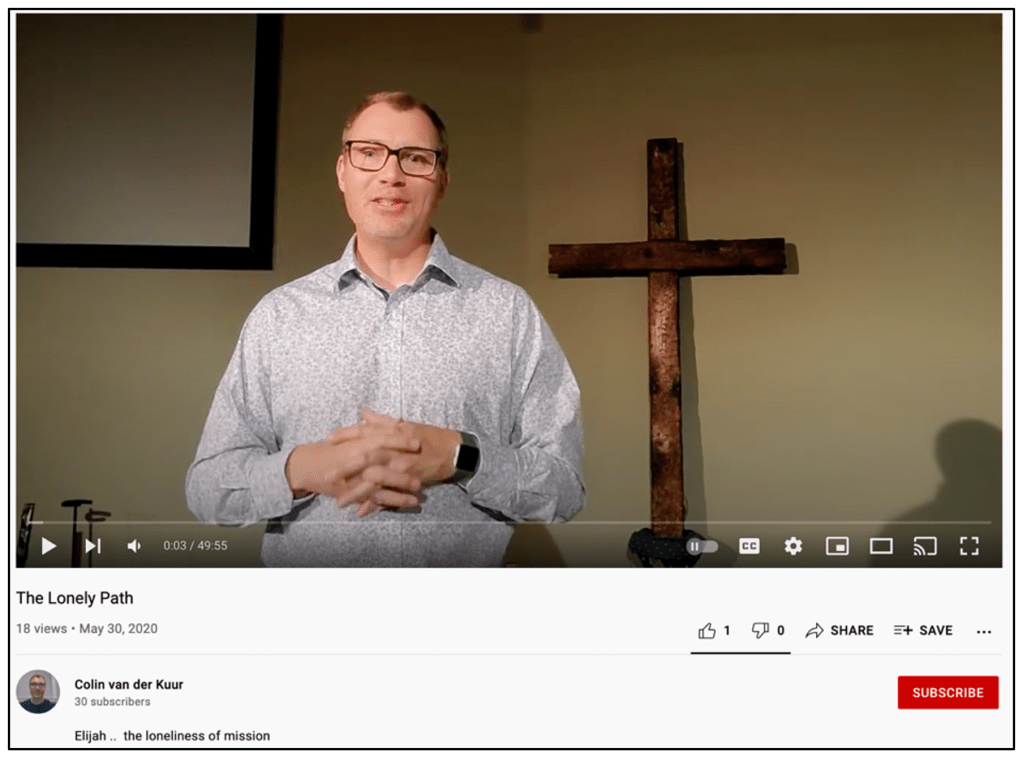

Compare to ZEN’s management team which is relatively short of relevant medical or scientific education and training. ZEN’s VP of Science and Research, Dr. Colin van der Kuur, completed a bachelor’s degree in physical chemistry but appears to have no science-based work experience before starting at ZEN as a “Research Catalyst” in 2018. In fact, the only other work experience Kuur lists on LinkedIn is as a Director of Church Reproduction at an evangelical organization. Although ZEN claims Dr. Kuur completed a doctorate in “leadership”, Dr. Kuur actually earned his honorific after completing a doctorate in Ministry, an advanced degree for pastors. Indeed, Kuur has posted dozens of sermons on YouTube.

Exhibit 11 – ZEN VP of Science and Research sermon video

We take no issue with Dr. Kuur’s faith. However, given his education and experience, we find it hard to believe he led the development of a novel compound effective against a novel virus. The only members of ZEN’s management team with backgrounds in medicine are Executive Chairman, Dr. Francis Dubé, an optometrist with a bachelors degree in organic chemistry, and three members of the advisory board who joined the company over 8 months after ZEN’s supposed breakthrough.

Patent Filings: GC Files Full Applications in Multiple Jurisdictions, ZEN Files “Delay Mechanism”

We think patent filings also support GC’s allegations. ZEN claims it filed a US provisional patent in September 2020. We are unable to verify this since provisional patents are unsearchable, abbreviated applications whose primary purpose is to preserve a filing date on the proposed invention. Provisionals must be converted into standard applications within one year or they expire. ZEN has not announced a full US patent application, so it’s possible the provisional application has lapsed.

On October 6, ZEN announced the filing of a “full international patent application” under the international Patent Cooperation Treaty (PCT). We note PCT applications are like provisional applications but with a 30-month deadline. PCT filers must still file in each member country to obtain a patent. According to a patent attorney, “… a PCT application is by nature a temporary placeholder. It serves as a delay mechanism to buy more time before entering the national stage of each desired member country.”

ZEN has not announced any other patent filings. It’s been over a year since ZEN supposedly developed ZENGuard. Why hasn’t a full patent application in a single jurisdiction been filed?

Meanwhile, in 2020 GC filed an international PCT application and full applications in the US and UK titled, “Viral active and/or anti-microbial inks and coatings”. And in October 2020, a month after ZEN announced successful development of the ink, GC filed an application in Canada. What reason would GC have to file in Canada other than to protect itself from Zentek?

Exhibit 12 – Graphene Composites’ UK patent filing

It should be noted that GC has encountered issues proving the novelty of its claims. Examiners in Canada and Europe have found prior art describing the use of graphene in anti-microbial formulations. Although GC has amended its claims in Canada, it remains to be seen if graphene-based anti-microbial ink is indeed inventive and patentable. As such, even if ZEN were to successfully defend itself against GC’s allegations, the win could be moot since ZENGuard may be ultimately unpatentable.

At the very least, assuming ZEN has valid claim to the technology, GC will be a considerable competitor. GC has already filed standard patent applications in the UK and Canada. Its partnered with researchers at Brown University with whom CTO Devine published an academic paper on the anti-viral activity of GC Ink. They have a commercialization partnership with G-Form, a medical and athletic equipment manufacturer based in Rhode Island with an estimated $19m in revenue last year. With a headquarters in the UK, and offices in the US and Norway, GC will have significant advantages in the US and Europe.

Despite the advantages, GC last raised money in August 2021 at a $70m valuation – 80% below ZEN’s current market cap.

Lawsuit Implications: Negative, Potentially Catastrophic

While ZEN may successfully defend itself or quietly settle the lawsuit, the severity of the allegations and the evidence presented by Graphene Composites is cause for concern, in our view. We see three main takeaways from the lawsuit. None of them good for ZEN.

- ZEN may not own the technology backing its only commercial product. If the GC lawsuit is successful, ZEN could be forced to stop selling the ink and pay any profit to GC. In another scenario, ZEN is permitted to continue selling the ink but owes GC royalties.

- ZEN potentially violated regulations requiring disclosure of material information. The Ontario Securities Commission (OSC) requires issuers to “publicly disclose any material changes to their affairs.” The OSC defines a material change as “a change in the business, operations, or capital of a company that would have a significant effect on the market price or value of its securities.” Given the sequence of events, the circumstances surrounding the dispute (comparison of management teams, patent filings) and that the plaintiff is a former partner, we find it highly likely the lawsuit meets this standard. All substantiate GC’s claims, increasing the probability of the lawsuit’s success in our view. In this context it’s important to note that ZEN has a history of serious disclosure issues. As previously noted, in December 2021, the Ontario Securities Commission forced the company to amend quarterly financial statements filed in November to include previously undisclosed product abandonments, stalled partnerships and a complete write-off of its largest asset.

- ZEN could be depicted in a negative light which could signal management issues. Improperly prodding for information about GC’s intellectual property with malicious intent, convincing the UWO to renege on signing an already agreed upon partnership, and concealing that effort from GC while lying to them about test results which were never coming – if the allegations are true, ZEN looks horrible.

History: A Failed Junior Miner Followed by Series of Unsuccessful Pivots

Before its latest nanotechnology/healthcare manifestation, Zentek began as Zenyatta Ventures, a junior mineral exploration company. Incorporated in 2008, Zenyatta was engaged in locating copper and nickel deposits. By its 2010 IPO, Zenyatta was exploring a graphite mine known as the Albany Graphite Deposit in northern Ontario.

Management claimed it “accidentally” discovered a vein of raw graphite in the mine that could be economically processed into 1.5m metric tons of a rare form of high purity graphite. CEO Aubrey Eveleigh pointed to “a lot of interest globally from electric car makers, battery makers, fuel cell makers, people interested in graphene.”

In 2012, Eveleigh was guiding for synthetic graphite production by 2015. He was simultaneously making bold claims regarding the purity of Zenyatta’s graphite and cost advantages of processing it relative to other supposedly inferior forms. A series of bullish press releases related to drilling results and the assistance of a promotional marketing firm fueled investor speculation leading to a 600% rally in ZEN shares over seven months in 2013.

However, Zenyatta never generated revenue from selling graphite (or any other product), and by the end of 2017 the stock was 90% off its peak. Zenyatta pivoted to graphene production in early 2018. A group of shareholders launched a proxy battle in mid-2018 resulting in a restructured board and management team.

Current Executive Chairman Dubé became ZEN’s Co-CEO in 2018. With a new focus on converting the Albany mine graphite into sale-able graphene, Zenyatta began touting research partnerships and supposed interest from multiple counterparties in off-take agreements:

Zenyatta’s unique Albany Graphite has been shown by multiple academic institutions including Sussex University and Ben-Gurion University to exfoliate more easily with higher yields of mono-layer to tri-layer graphene. This has attracted interest from other graphene producers to work with Albany Graphite.

Zentek, September 2018

At the end of 2018, the company announced several new verticals including “aerospace, biomedical, water treatment, transportation and civil engineering.” Among the potential product offerings – lightning strike protection, radar/sonar absorption, oncology treatment and diabetes testing. In 2019, Zenyatta changed its name to ZEN Graphene Solutions to reflect the company’s focus on a “graphene nano-material product opportunity”. In March 2020, ZEN announced the launch of graphene product sales on its website. Products included graphene product dots and graphene oxide.

We have reached a major milestone as our 2020 goal is to start bringing in revenue from the production and sale of Albany Pure TM graphene products. Graphene is the new wonder material that is just beginning to be used in many large-scale industrial applications and we are entering the graphene sales market at an optimal time.

Zentek, March 2020

Contrary to management’s optimism, ZEN never generated any revenue from the sale of graphene. The company has apparently abandoned these efforts as graphene oxide is no longer offered on its website.

Between 2019 and mid-2020, ZEN’s stock traded below $0.50. After the onset of Covid-19, ZEN was one of many floundering small-caps which changed course to capitalize on the pandemic. During a time of frenzied demand for PPE, ZEN entered the partnership with GC, asserting that it had a “significant competitive advantage in the production of large-scale graphene projects including graphene oxide…” [Pg. 7]. Note, ZEN currently purchases third-party graphene oxide, claiming it does not have the proper permits to produce its own [Pg. 6].

ZEN’s Advertises a Global TAM (Likely Inflated By 300%), But Its Masks Are Only Authorized in Canada

In September 2020, ZEN announced the development of ZENGuard and its “99% effectiveness” against Covid-19. ZEN shares closed 63% higher and the stock continued upward on investor hopes for applications in PPE amid heightened pandemic demand.

ZEN investor presentations contain profitability estimates which appear attractive – even a small share of a large face mask TAM produces gross profitability figures which at the high end are multiples of the current market cap. But ZEN is basing its projections on a poor, overinflated TAM estimate in our view.

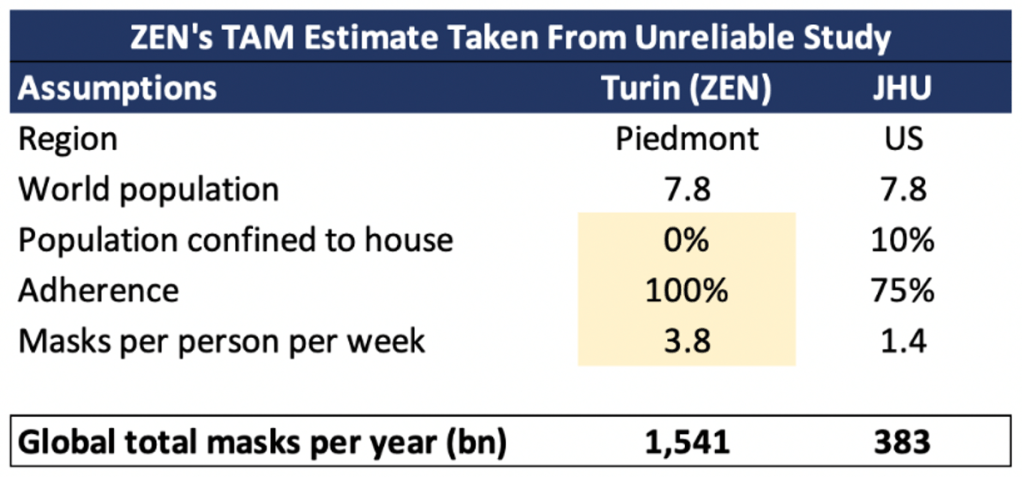

ZEN assumes current usage of 1.5 trillion masks per year and discounts this by 40% to arrive at a post-pandemic demand of 930 billion. The 1.5tn figure was taken from a June 2020 paper titled “COVID-19 Pandemic Repercussions on the Use and Management of Plastics” by Prata et al. which estimates global mask use at 129bn masks per month.

Prata took this figure from an April 2020 study by the Polytechnic University of Turin which estimated the PPE usage of the workforce of Italy’s Piedmont region. Turin estimated a need of 80m face masks per month and extrapolated this to 1bn per month masks for Italy as a whole. This equals approximately 17 masks per month per person. Prata applies this to the global population of 7.8bn to arrive at an annual figure of 1.5tn masks. So, from a single estimate (calculated during peak pandemic fear) of the mask needs of the employed population of one of Italy’s 20 regions, global mask demand is calculated, and ZEN estimates its profitability. Ha senso?

Exhibit 13 – ZEN investor presentation

While the actual usage of face masks globally has not been well quantified, researchers at Johns Hopkins University (JHU), published their own estimates in a model last year. The model assumes 75% of the US population uses 1 mask every 5 days. It discounts for adherence and people confined to their house.

Exhibit 14 – ZEN mask TAM estimate vs Johns Hopkins

If JHU’s figures are extended to the world’s population, annual mask usage is below 400bn units, or approximately 25% of the estimate ZEN is using. And as a sanity check, how many people use 4 new masks per week? ZEN assumes everyone does.

Regardless of how TAM is estimated, perhaps the more important point is that ZENGuard masks are only authorized for sale in Canada which accounts for less than 0.005% of the world’s population (Canada has a reciprocal authorization agreement with the EU, but ZEN must still apply under an expedited process). Authorization outside of Canada will take time and resources, and the associated regulatory risks are significant (see the case of HeiQ below). However, we expect ZEN will not apply for authorization in many areas outside of Canada as it becomes clear the consumer PPE market isn’t attractive.

Face Mask Manufacturers Report Supply Glut, Collapse of Demand

While ZEN is accounting for a drop in peak demand post-pandemic, is 60% a reasonable discount? 3M and Honeywell, two of the largest mask manufacturers in the world, were already reporting huge drop-offs in demand last summer and Honeywell closed two mask factories in June.

PPE manufacturer Alpha Pro Tech (NYSE: APT) in November reported mask sales normalizing to pre-pandemic levels, due to high levels of inventory, increased competition, and an improved pandemic outlook. APT is on track to generate over $90m in sales and $8m in net income in FY21 but has an enterprise value of only $50m.

The company continued to see the normalization of mask and shield sales to pre-pandemic levels in the third quarter…

Lloyd Hoffman, CEO Alpha Pro Tech, November 2021

Members of the American Masks Manufacturer’s Association (AMMA), a group of 28 small-business mask manufacturers founded at the beginning of this year, report similar difficulties and a lack of government support against cheap supply from Chinese manufacturers. This, in addition to the mass vaccination drive, has already put 5 of its members out of business with more likely to follow, according to the AMMA.

Virginia Beach-based manufacturer Premium-PPE entered the face mask market last year and by early 2021 was producing 1m masks per day. By June it had cut production by 80-90% and laid off most of its employees.

DemeTech, a medical suture manufacturer, pivoted to mask production last year. The company expected to sell bulk orders to state and federal governments but according to DemeTech’s president Luis Arguello, demand has severely disappointed and DemeTech is instead selling small batches in the consumer market via its website. It has let go of over 1,300 workers and has almost 200m masks in inventory. “We haven’t sold one order to any government this year,” Arguello said in October.

See also Texas-based Prestige Ameritech, the largest face mask manufacturer in the US. Founded in 2000, Prestige has estimated annual revenue of only $50m. Prestige CEO Mike Bowen, a 35-year industry veteran who saw how new entrants crowded the industry during the 2009 swine flu pandemic, offered a warning for companies entering the market during heightened pandemic demand:

We’ve seen this movie before. If and when the pandemic is over, it’s going to be a freaking blood bath.

Prestige Ameritech CEO Mike Bowen

In our view, if established mask manufacturers are reporting such difficulties, ZEN and Trebor Rx will not sell hundreds of millions of masks a year, let alone billions. It won’t help that ZEN is positioning its masks at the higher end of the mask spectrum. An independent, one-person distributor company offering ZENGuard masks (one of only two distributors that we could find) lists them at $0.48 each. This is considerably more expensive than the masks that likely make up most of global usage – disposable masks made in China that sell for an average of $0.01 each. At $0.48, ZENGuard masks are at a similar price point as some 3M N95s.

Exhibit 15 – ZEN masks price $0.48 each (50 per box)

And if 3M, a multinational conglomerate with over $30bn in revenue, only sold 2bn N95s during the peak demand of 2020 (up 4x vs 2019), what are the chances of ZEN approaching even 10% of that?

Neither will it help that states are quickly dropping face mask mandates. Increasing vaccination rates, and declining covid cases and hospitalizations have led states to ease mask requirements (only three currently have mandates).

Award Winning Anti-Viral Face Mask Manufacturer Reports Flooded Market, Valued 60% below ZEN

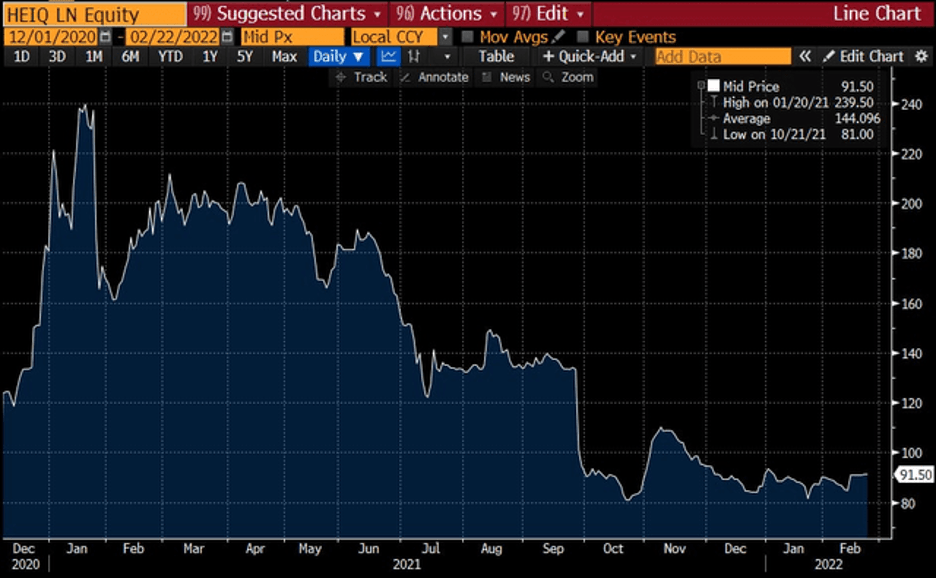

Even assuming ZEN owns full rights to the ZENGuard technology and that it survives in a crowded face mask market, the upside is nonexistent in our view. Look at HeiQ (LSE: HEIQ), a London-based textile company. HeiQ received the Swiss Technology Award in 2020 for developing Viroblock, a silver-based antimicrobial coating that can be applied to face masks. Tests showed Viroblock killed coronavirus within minutes. Sound familiar?

HeiQ developed Viroblock during the 2013 Ebola crisis but shelved the technology due to weak demand. The company restarted production in early 2020 at the pandemic’s onset and went public in December 2020. Excitement for Viroblock caused shares to double by March 2021.

Viroblock was used by over 150 brands and in over 1bn face masks in 2020, yet total revenue for the product was only around $20m [Pg. 9, 17]. Echoing other mask manufacturers, HeiQ reported a severely deteriorated face mask market in its 2Q 2021 earnings release:

“The market for face masks and personal protection equipment is under extreme price pressures caused by low-cost suppliers flooding the market in Q1 2021 and there being large amounts of excess stock from the previous year.“

According to a company representative, HeiQ recently took Viroblock masks off the market after the EPA requested additional safety documentation, an indication of the regulatory hurdles ZEN will face if it intends to market ZENGuard in the US.

HeiQ is debt free, has seven manufacturing sites and over 300 brand partners including names like Bosch, Burberry, and GAP. HeiQ shares traded sharply lower after the Q2 report and are currently 30% below their IPO price. The company is expected to generate $63m in revenue and $6m in EBITDA for 2021 yet has an enterprise value of $190m – over 60% below ZEN’s.

ZEN Is Uninvestible

At a $320m valuation based on a highly promoted but remarkably flawed story, we believe a correction looms for ZEN stock. Hysteria and momentum trading gripped “covid-plays” earlier in the pandemic, but most of the mispricing has reverted. ZEN, however, remains in bubble territory in our view.

We believe management has shown a pattern of poor disclosure and, if its former partner’s allegations are true, unabashed self-dealing. We think ZEN’s lack of scientific expertise and its failure to complete even a single full patent filing substantiate the allegations.

We think it’s absurd that ZEN, a company that recorded its first ever revenue – only $705k – in the last two quarters of 2021 and has no other near-term commercial products, is trading at such a premium to HeiQ. Accounting for the fundamental risks alone – an extremely weak mask market, ZEN’s capital intensive manufacturing plans which are severely behind schedule, a valuation based on a bloated TAM estimate – we expect the relative value relationship will eventually be reversed.

We think the absolute bull case valuation for ZEN should be a considerable discount to HeiQ which served the same market at peak demand and generates revenue from several distinct product segments. A 50% discount to HeiQ would equate to $1/share. Considering the undisclosed legal risk, and the possibility that ZEN does not own the technology backing its only product, fair value is likely much lower.

We recommend investors exit long positions and/or initiate short exposure. Risks to the upside include better than expected face mask sales and positive developments with ZEN’s other early stage efforts.

Disclaimer

As of the publication date of this report, Night Market Research (NMR) and Connected Persons (as defined hereunder), along with or through its members, partners, affiliates, employees, clients, and investors, and/or their clients and investors have a short position in the securities covered herein (and options, swaps, and other derivatives related to these securities), and therefore will realize significant gains in the event that the price of any stock covered herein declines. NMR and NMR Connected Persons are likely to continue to transact in the securities covered herein for an indefinite period after an initial report, and such position(s) may be long, short, or neutral at any time hereafter regardless of their initial position(s) and views as stated in NMR’s research.

Use of NMR’s research is at your own risk. In no event shall NMR or any NMR Connected Person be liable for any direct or indirect trading losses caused by any information in this report. You further agree to do your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities covered herein.

This is not an offer to sell or a solicitation of an offer to buy any security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. NMR is not registered as an investment advisor in the United States, nor does NMR have similar registration in any other jurisdiction. To the best of NMR ‘s ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources NMR believes to be accurate and reliable, and who are not insiders or connected persons of the issuer covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind – whether express or implied. NMR makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and NMR does not undertake to update or supplement this report or any of the information contained herein.

NMR Connected Person is defined as: NMR and its affiliates and related parties, including, but not limited to any principals, officers, directors, employees, members, clients, investors, and agents. One or more NMR Connected Persons may have provided NMR with publicly available information that NMR has included in this report, following NMR’s independent due diligence.