- Revenue growth masks deteriorating profitability: operating margins trend lower (64% lower past two years) as Zynex accelerates hiring in face of early signs of reimbursement pressure.

- Tricare becomes first large health plan since Medicare to drop ZYXI’s device for one of its largest indications citing poor efficacy – we expect other payors to follow

- Zynex routinely waives deductibles and copays, a practice prohibited by Medicare and which likely violates insurance law pertaining to commercial payors constituting breach of contract

- We have been in contact with commercial and government investigators examining ZYXI claims, including the Department of Insurance of large state investigating after an insurance company reported Zynex’s billing

- Analysts mistake Zynex as a Medical Technology company. It’s actually a DME supplier – appropriate multiples would value the stock ³80% lower before reflecting the risks we have identified.

A Deeper Look Reveals New Concerns and Adds To Our Conviction

Zynex (NASDAQ: ZYXI) shares are up 180% year to date vs the Health Care Select SPDR ETF (NYSE: XLV) at -2%. We believe ZYXI’s outperformance is a function of retail investor complacency combined with sell-side analyst carelessness and leaves the stock extremely vulnerable to a major repricing lower.

In our previous report, we presented a bearish thesis predicated on two main points in context with valuation. First, Zynex sells generic commodities at prices multiples above market levels. Second, we were unable to reconcile ZYXI’s revenue per device with government payer reimbursement rates.

Since then we took a much more comprehensive review of the company. Over several months we interviewed former employees, customers, and competitors. We consulted healthcare lawyers and reimbursement consultants, and spoke with investigators at insurance companies and government agencies.

The bull case rests on several key assumptions. Revenue growth continues for years in a largely untapped total addressable market. Margins expand after Zynex hires a full salesforce. Competition won’t impact market share gains in a meaningful way. A new device is technologically innovative and anticipated to successfully launch. And most importantly, commercial insurer reimbursement rates for 9-volt batteries and electrodes remain stable.

In our view, each point is flimsy, but when combined the case becomes wholly unsupportable. And in context of the most significant risks and Zynex’s all-time high valuation, the set-up for investors is precarious. As a result of our research, we now believe the value of the business is near zero and the most probable outcome for shareholders is near total losses. We have identified troubling issues that raise immediate concerns regarding the fundamental and legal structure of the business:

- An apparent lack of management transparency or awareness of financial details as CEO maintains that revenue mix and reimbursements have been consistent for years, contradicting financial statements which show a major, unexplained shift beginning in 2017.

- Supplies revenue per order nonsensically increased by ~400% in 2017, allowing Zynex to reach profitability, but is now reverting to previous loss-making levels. Revenue per order is down ~30% in the last two years and we see signs of reimbursement pressure going forward.

- Zynex is totally reliant on supplies resales. In particular we estimate electrode resales alone account for ~50% of revenues and gross profits, highlighting the absurdity of the business model and how exposed ZYXI is to any change in reimbursement on this single commoditized product.

- Zynex is accelerating hiring (SG&A on pace to be up ~400% vs three years ago) while revenue per order is declining and as a result operating margins have collapsed 64% from peak to lowest level in three years.

- Zynex provides minimal disclosure on three products which may account for up to 20% of EBITDA. One product (back brace manufactured by Aspen) faces reimbursement cuts next year which could materially affect earnings.

- Zynex recently expanded into medical equipment dropshipping, a business with extremely thin margins. The company touted the announcement on social media causing the stock to rally 10% before the actual press release.

- Besides NexWave, every Zynex-manufactured product has been an unambiguous failure. Zynex is touting a new device it calls a “Blood Volume Monitor” and we expect it to follow due to woefully inadequate data and management’s inexperience.

- Zynex routinely waives deductibles and copays, a policy which likely violates contracts with payors who can sue for breach, stop paying claims and attempt to recoup past payments.

Since October 2019, Zynex has reported continued growth in orders and revenues which isn’t surprising as the company has almost tripled its salesforce in the last two years, adding a net 15 sales reps per month this year alone. Retail has been drawn in by this growth story, but actively-managed institutional ownership remains negligible. In fact, no institution, actively managed money or not, has owned more than 5% of shares since 2011.

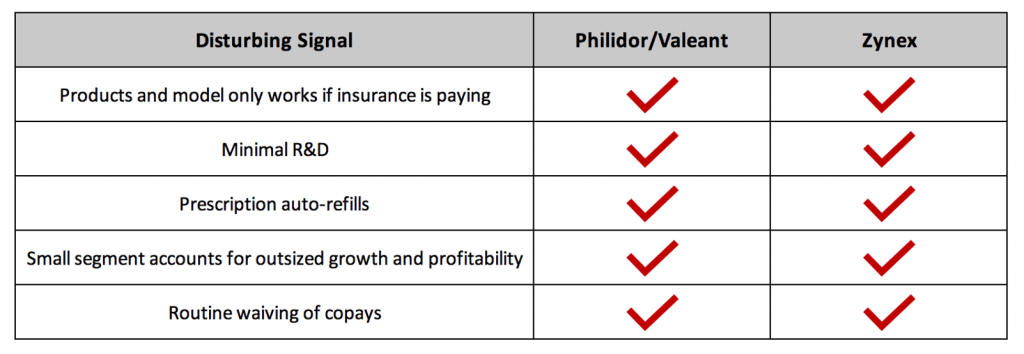

In reality Zynex is a parasitic business gouging insurers (and consumers), acting under the pretense of helping in the fight against the opioid epidemic. We see similarities to Philidor in Zynex’s minimal R&D, monthly prescription auto-renewals, and routine copay waivers.

Most troubling for Zynex in the near term, is early signs of payors questioning reimbursements. In Q1 20, gross margins fell below 80% for the first time since Q1 17, due to lower reimbursement from commercial payors. We believe this is only the beginning of payor pressure for several reasons. Tricare’s negative coverage decision puts TENS units under a spotlight. Commercial insurers and state regulators are paying more attention to Zynex, in part because of our allegations. At the same time, Zynex revenues are becoming too substantial (consensus 2020 revenues are $80mn), for health plans to ignore. We’ve heard from bulls who own Zynex in part because they believe regulators and insurers have bigger issues to worry about, that Zynex is inconsequential and can stay under the radar even if they are price gouging insurers. We believe this view is shockingly complacent.

In this report we examine additional irregular trends in revenues and inconsistencies in management’s attempt to rationalize them. We look at a recently public comparable trading with an EBITDA multiple 80% below ZYXI despite equivalent net margins, highly respected management and a credible business model. We disclose that several commercial and government investigators, in response to our concerns, are examining ZYXI claims, including the Department of Insurance of a large state. We also discuss factors contributing to the stock’s mispricing and present a valuation based on comparative multiples and DCF which prices the stock at least 70% lower.

A copy of this report has been sent to commercial insurance companies and state insurance regulators.

Parasitic Business Model

Zynex sells the NexWave, an unpatented transcutaneous electrical nerve stimulation (TENS) device for the treatment of pain. TENS units are based on archaic technology and commonly available over the counter. NexWave is not significantly different from OTC devices but it requires a prescription which allows Zynex to claim medical necessity and – most importantly – bill insurance.

NexWave sales make up approximately 15-20% of ZYXI’s revenue. Resales of the supplies used with the device – 9-volt alkaline batteries and cloth electrodes – account for 80%. Last year Zynex collected $35mn on battery and electrode resales at roughly 90% gross margins (we estimate ZYXI collects ~10x prices for exact same product sold at retail). The ability to bill captive and relatively price insensitive insurance companies has allowed Zynex to distribute commoditized goods at prices wildly above market rates. Similarly, Valeant and Philidor created an insurance-subsidized artificial market for absurdly expensive branded drugs. Both business models are only viable if insurance is paying and reimbursement is firm.

Exhibit 1. Zynex sends recurring monthly supplies to patients, bills payors, and routinely waives copay

Zynex calls itself an “innovative medical device company” (beginning of every press release) but it spends a negligible amount on research and development, an average of $330k per year since 2007. R&D is so insignificant at Zynex that it’s not even itemized on income statements, unlike every medical device company in Exhibit 2. Zynex operates as a supplies distributor in every respect yet realizes gross margins above the most innovative names in the Medical Technology sector. We fail to see how this model is sustainable over the long-term.

Exhibit 2: Zynex margins at top of Medical Technology sector despite model of generics distributor

CEO’s Attempt to Explain Revenue Shift Contradicts Financials

Before we discuss our new findings, we mention a critical issue which management has failed to adequately address, and which raises concerns around management transparency and credibility.

Recall Zynex reports revenues in two segments: device (NexWave) and supplies (batteries and electrodes). Between 2009 and 2016 supplies averaged 40% of total revenues but then jumped to 80% starting in 2017. After we made this point in our previous report, CEO Thomas Sandgaard claimed it was due to an accounting change during the Q3 19 earnings call:

“The split between device revenue and supplies revenue has always been fairly consistent over the past couple of decades. If you look at historical results and comparing those results, please keep in mind that we’ve reclassified our device and supplies allocations beginning in 2018, and those reclassifications were pushed back into the 2017 numbers, but not to any periods prior to 2017… [Reimbursement] has been fairly consistent over the past 24 years.”

However, Sandgaard’s explanation is contradicted by the 2017 10-K, before the reclassifications in 2018. As shown below, supplies as a portion of total revenues doubled from 2016 to 2017.

Exhibit 3. Revenue shift occurred before 2018 reclassification

Zynex has not responded to requests for comment. As we discuss below, supplies revenue (particularly one product) underpins the entire business and it’s concerning that management appears less than fully transparent or unaware of an issue so important and easily verifiable.

Profitability is Declining As Nonsensical Revenue Shows Signs of Reversal

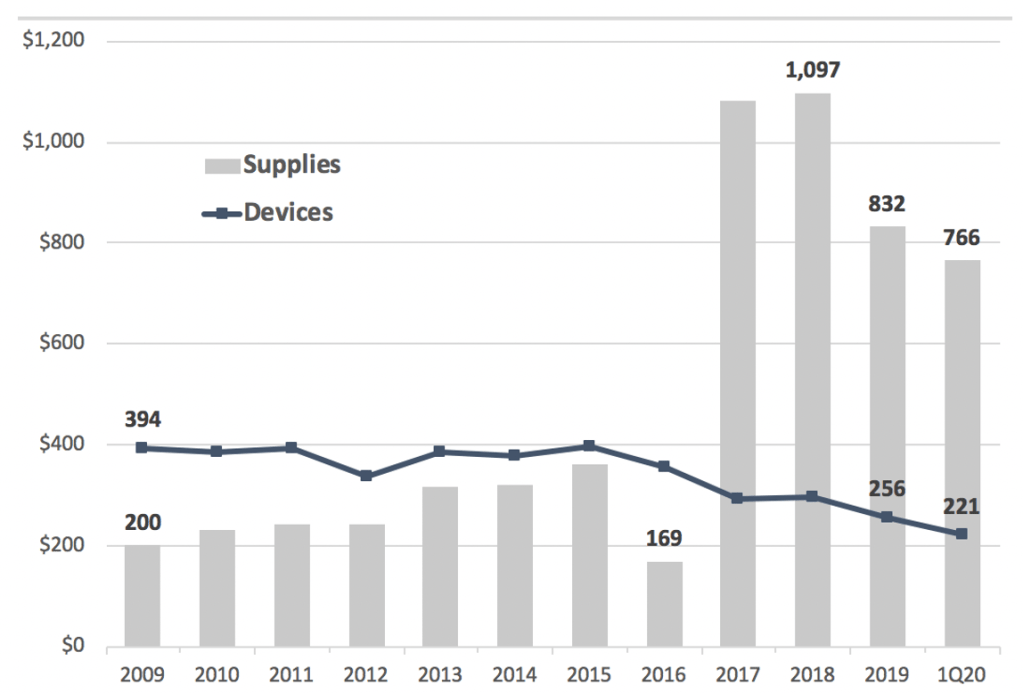

For this report we took a closer look at the composition of revenues and find signs that Zynex’s business is regressing. Between 2008 and 2016, revenue divided by total orders averaged $620, then suddenly increased to $1.4k in 2017. Note these figures are only approximations as revenue typically lags by a quarter or so due to order processing times, but the trend is what’s interesting and important (Exhibit 4).

Exhibit 4. Revenues per order doubled in 2017

Looking at each segment, average device revenues fell 40% but the average for supplies increased over 400%, spiking in 2017.

Exhibit 5. Revenue per order fell for device but increased sharply for supplies

We know supplies doubled as a percent of total revenues, but here we see revenue per order for each category moved in opposite directions. Reimbursement for each NexWave fell, but the increase in supplies has more than made up for it, revealing how dependent ZYXI is on supplies resales.

Zynex doesn’t disclose how supplies revenue is split between batteries and electrodes, but in a one-on-one conversation management told us the current split is roughly 35% and 65% respectively. This would mean ZYXI resold about $22.6mn of electrodes last year. Electrode resales account for roughly half of Zynex’s revenue.

It is not clear what caused the spike in supplies reimbursements. In its 2017 press releases and financial statements management generally attributed an increase in overall revenue to “improvements in cash collections as a result of improved billing efforts.”

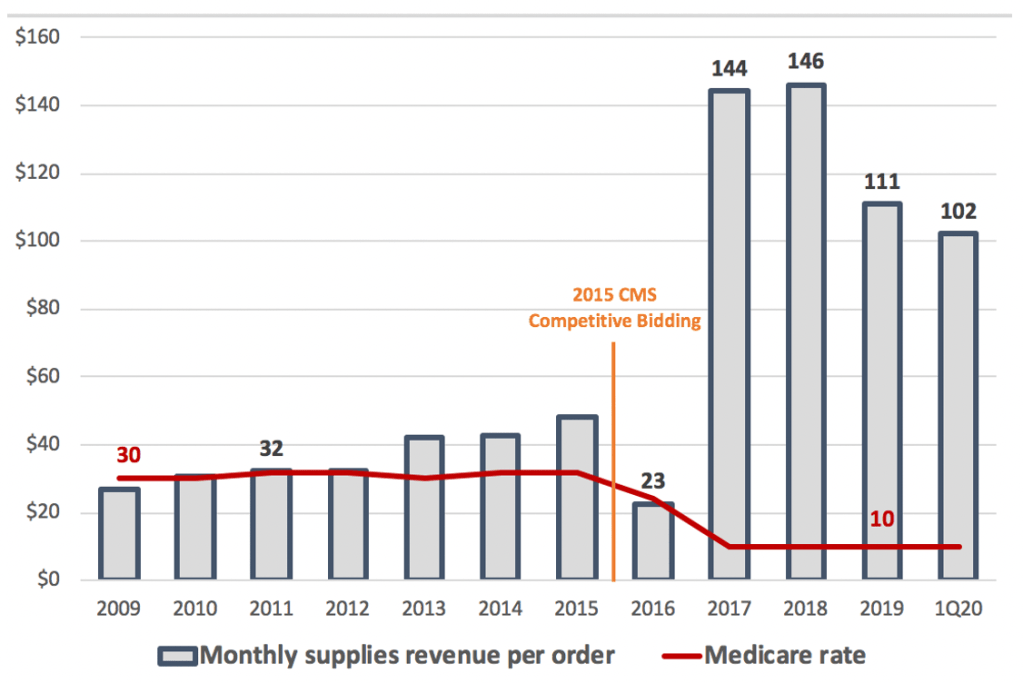

We doubt better collections alone could result in such a big increase in supplies revenue since collections were apparently consistent for the previous nine years. Besides if collections improved so much, why did revenue for NexWave drop? Also, recall that Centers for Medicare and Medicare Services severely cut reimbursement for TENS units and supplies between 2015 and 2017 as part of the Competitive Bidding program (CBP). Afterwards Medicare payments on TENS units fell from approximately $400 to $65 and from $32 to $10 on a monthly pack of supplies (which includes batteries and electrodes) [Pg. 44]. We would not expect commercial insurers to in turn increase rates, especially on supplies. Zynex has not responded to multiple requests for comment.

Exhibit 6. Medicare supplies rate per patient fell by 70% yet Zynex monthly supplies revenue up 4-5x

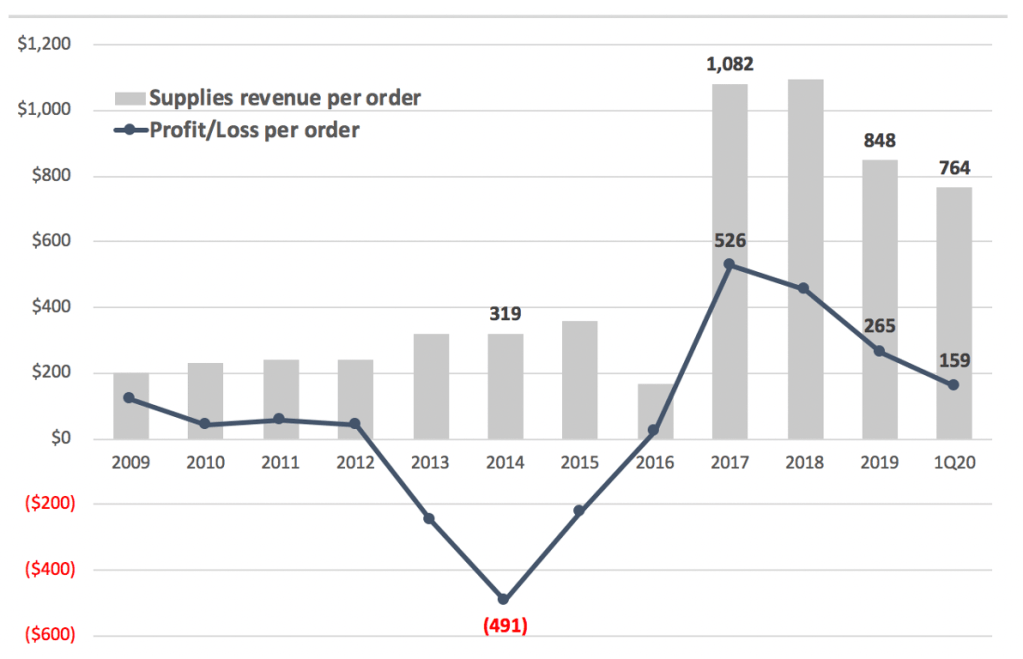

This leap in supplies revenue was crucial to Zynex’s survival. The company was in default of a credit facility and Zynex shares had not closed above $1 since 2010, trading as low as $0.10 in 2016. The influx of supplies revenue allowed Zynex to reach profitability and pay off its lender.

Exhibit 7. Zynex completely dependent on large increase in battery/electrode reimbursement

However, in our view the period before 2017 represents the natural state of ZYXI’s business and the anomaly seen that year is reversing (Exhibit 7). It’s possible Zynex experienced a surge of new patients covered by an insurer who temporarily allowed a greater quantity of supplies per patient. If so that grouping of higher margin patients is being diluted by patients covered by payors with typical coverage policies. Or maybe Zynex found a weakness in a large payor’s reimbursement policies which has been fixed.

In any case, this batch of abnormally high reimbursement appears to be running off. Margins have narrowed and we expect they will eventually move to levels seen before 2017. Reselling batteries and electrodes is unlikely to be a high margin, large scale business in the long-term, in our view. Anyone skeptical should ask themselves why no other company has made a meaningful effort in the TENS business since 2015.

Even more concerning is the average revenue decline is occurring while Zynex is on a hiring spree. So far this year Zynex has added 100 sales reps after attrition (60% increase) and will add another 100 before year end with a goal of 400 total. SG&A is on track to be up >5x this year vs 2017. This is hitting profitability – operating margins, which in the first quarter fell below 20% for the first time in three years, are 36% lower since our first report and 64% off the 2017 peak.

We note the large increase in supplies revenue in 2017 occurred at a time of management disorder. Zynex was required to disclose material internal weaknesses during this period:

- Sandgaard was the only member of BOD after he requested the resignation of the other four members in 2014. He remained sole director until January 2018.

- Sandgaard assumed the role of CFO between October 2015 and June 2017, after the previous CFO was “discontinued”.

From the 2016 10-K [Pg. 18]:

“As previously reported and not remediated as of and during the year ended December 31, 2016, we reported material weaknesses in our internal control over financial reporting (ICFR) as we do not currently have an independent audit committee overseeing our internal controls, or an independent member of our Board. In addition, we have material weaknesses due to a lack of segregation of duties within our accounting and approval process.”

Exhibit 8. Jump in supplies reimbursement occurred during management deficiencies

TRICARE Concludes TENS Ineffective For Lower Back Pain, Will No Longer Cover – Can Other Payors Be Far Behind?

Tricare, the health plan for military members, retirees and their families, recently decided to stop covering TENS units for lower-back pain beginning June 1, 2020. Tricare based its decision on studies by the Defense Department, American College of Physicians, and Department of Veterans Affairs which found “insufficient evidence” to support the efficacy of TENS therapy as a treatment for lower-back pain. From the above linked article:

“Additionally, reliable evidence in published medical literature increasingly finds that TENS for lower back pain is no more effective than sham TENS (placebo),” a Tricare official said via email..

Recall Medicare stopped covering TENS for lower-back pain in 2012 as it also found clinical evidence was lacking. After extensive review Centers for Medicare and Medicaid Services (CMS) stated:

“TENS is not reasonable and necessary for the treatment of CLBP… We in fact found that sham (placebo) TENS produces equivalent analgesia to active TENS… While we agree that the apparent patient risks are low, we do not believe that outweighs the direction of the evidence base considered as a whole – that TENS does not improve health outcomes and therefore should be noncovered.”

Zynex does not disclose how much revenue is tied to Tricare patients, but in addition to the negative impact on ZYXI profitability, the signal this sends to commercial payors and worker’s compensation plans is ominous, for one of the most prevalent musculoskeletal disorders. According to a review by St Sauver et al. (2013) back problems is the third most common reason for doctor’s office visits. What’s especially alarming is how unequivocal Tricare is in concluding TENS therapy is ineffective. See also the extensive research done by CMS in reaching the same conclusion. It would not be surprising to see other payors follow suit.

Shades of Philidor: Focus on Maximizing Insurance Reimbursement Not Patient Needs

Unique to companies whose primary source of revenue is insurance companies, is that as revenues rise, so does the risk that your business model – products, quantities, prices – will be scrutinized. This is especially so if your products provide low value relative to cost, or if you are distributing generics as were Valeant and Philidor and now Zynex.

We believe Zynex’s model shares several characteristics with Philidor/Valeant. Philidor, the infamous specialty pharmacy Valeant used as a channel to inflate revenues, was criticized for using aggressive tactics to maximize volume and reimbursement on several medications.

For instance, Philidor repeatedly submitted unwanted or unnecessary prescription renewals to boost sales on drugs with generic alternatives. Zynex is incentivized to do the same, but with generic batteries and electrodes. On the Q3 19 earnings call, Sandgaard admitted to auto-renewing monthly supplies shipments to NexWave users, regardless of need and without checking with patients:

Analyst: “Can you remind us, is there a standard kind of quantity and cadence of supplies that patients usually receive? And then, piggybacking on that, is there a process for patients to either request more or less supplies? What percentage of patients actually vary from that standard quantity?”

Sandgaard: “…it’s really up to the individual insurance company and how they allow, how many supplies they allow for the patients. Some insurance companies have rules in there where we need to check with the patient every three months, and then we can continue if we get a confirmation. So, it’s really all regulated by the insurance companies, and they obviously get an initial amount of supplies when we ship the device, and from there on out, it’s really what kind of quantities that the insurance company allows.”

Key to the auto-distribution strategy is ZYXI’s choice of disposable rather than rechargeable batteries since the goal is to bill for as many units as possible. We estimate Zynex is reimbursed approximately $10 per battery. The same battery is available at retail for $1.35, or less with volume discounts.

Evidence of over-shipments can be found on eBay where thousands of unused Zynex-labeled electrodes are listed. And this doesn’t account for completed offerings – thousands more were sold in just the last three months in 80+ listings. Battery listings are more difficult to spot since Zynex stopped reselling private-labeled Rayovac 9V batteries, opting instead to resell the batteries in the original Rayovac packaging. Zynex has not responded to request for comment.

Not only are the products egregiously priced, but Zynex is also apparently forcing excessive quantities through the system. How long before insurers step in, especially as revenues grow?

Shades of Philidor: Medical Equipment Distributed by Zynex Is Only 5% of Revenues But Likely Outsized Earnings Contributor

In a 2017 press release titled “Zynex Continues Fight Against Opioid Abuse and Expands Its Arsenal of Pain Relief Products”, the company announced it would start offering back braces, hot/cold therapy and cervical traction. Similar to its battery and electrode segment, ZYXI does not manufacture any of these products – it purchases them from manufacturers, distributes them to patients and bills insurance – the standard durable medical equipment (DME) supplier model.

The back brace Zynex distributes is the Aspen Horizon 637 LSO. As is common among “prescription” braces, its name includes the Healthcare Common Procedure Coding System (HCPCS) code suppliers use to bill insurance. Manufactured by Aspen Medical Products, the Horizon 637 can be found online for around $100, but reimbursement fees range from $1050 to $1400. With such large margins, the back brace industry (and durable medical equipment in general) is a common target of insurance fraud.

Zynex does not specify how much revenue is generated from these products, but CFO Dan Moorehead told us the total is around 5%. If so, Zynex distributed approximately $2.3mn of this equipment in 2019. Given the extremely wide margins, these products – for which Zynex provides minimal disclosure – may have accounted for up to 20% of 2019 EBITDA.

We note that another round of Competitive Bidding will take effect in 2021 and back braces are included for the first time, cutting reimbursement for a potentially significant ZYXI earnings contributor. The lack of disclosure here is concerning as any change in reimbursement would have a relatively large effect on overall profitability.

Shades of Philidor: Zynex Routinely Waives Deductibles and Copay – Potentially Fraud, Likely Breach of Contract

Insurers use copays (deductibles and copayments) as a form of cost-sharing to incentivize patients to consider cost thereby curbing overutilization. Copay assistance refers to manufacturer sponsored programs that limit these out of pocket costs. Since these programs can steer patients towards higher priced drugs or equipment instead of cheaper alternatives, their use receives regulator and payor scrutiny. See Valeant for instance, which at its peak was spending almost 10% of revenue on copay assistance. CEO Michael Pearson was eventually forced to explain Valeant’s use of copay programs in front of Congress. The following is an exchange with Senator Elizabeth Warren:

Warren: “Well, let me ask you a question in a different direction. Why don’t you use these co-pay reduction programs with federal government programs like Medicare and Medicaid?”

Pearson: “Um, my understanding is we are not allowed to.”

“Yup,” responded Warren. “Because it’s illegal. And that is exactly the problem here. These programs are illegal because Medicare and Medicaid understand that the programs are scams to hide the true cost of the products from the consumers and drive up the costs for all of the taxpayers.”

Federal law considers copay assistance to Medicare patients to be fraud unless in rare instances of a patient’s financial hardship. Specifically copay programs violate Anti-Kickback Statutes by offering remuneration to induce individuals to purchase medical care at taxpayer expense [Pg. 22], and the False Claims Act by misstating usual, customary or reasonable charges.

We have learned that Zynex routinely waives deductibles and copayments for both in- and out-of-network patients. We have no evidence that Zynex does so with Medicare covered patients, but several current employees told us it is company policy to avoid billing commercially insured patients for any amount as long as Zynex is reimbursed at least $250 per NexWave.

Patients who receive a NexWave prescription assign their insurance benefits to Zynex allowing Zynex to send claims to payors. If a payor refuses coverage Zynex directly bills patients a monthly $25 “rental fee”. If NexWave is covered, Zynex continues to submit monthly claims:

- NexWave purchase at $1,995 or

- NexWave rental at $369 per month

- Each pack of electrodes (2 pairs) at $99

- Each battery at $9.99

For patients with an unmet deductible, Zynex will bill insurance until its met and as long as they eventually collect $250, Zynex will not ask for payment from patients to cover deductibles nor will it attempt to collect any payor mandated copays. Not bothering patients with copays makes it much easier for Zynex to send recurring monthly shipments of batteries and electrodes and then collect from insurance at prices multiples above retail.

As with Medicare patients, the problem is that by accepting payment from insurers net of copay as payment in full, but then accepting a higher reimbursement for patients with lesser or no copays, Zynex is misrepresenting its actual charge. In other words, Zynex is filing false claims.

A close acquaintance was recently prescribed NexWave. With his permission we called Zynex customer service posing as him, using his account number, date of birth and address. Several Zynex reps told us on separate phone calls that even though there was over $800 in unmet deductible, he would not be responsible for any payment since his insurance would reimburse at amounts large enough to meet the deductible and copays and still leave Zynex adequately compensated. The reps told us this was routine practice.

While federal law prohibits copay assistance for public payor patients, the law as it applies to commercial insurance varies between states. Certain states like Colorado, Texas and Florida have statutes that prohibit waiving copayments unless in circumstances of financial hardship.

New York Department of Insurance states that routine waiving of co-insurance may be “fraud”:

“If a health care provider, as a general business practice, waives otherwise required co-insurance requirements, that provider may be guilty of insurance fraud.”

Colorado law specifically states that routine waiver of copayment is illegal:

“Business practices that have the effect of eliminating the need for actual payment by the recipient of health care of required copayments and deductibles in health benefit plans interfere with contractual obligations entered into between the insured and the insurer relating to such payments;… the general assembly declares that such business practices are illegal…”

The following is a good legal summary of the issues and legality of patient assistant programs as it applies to commercial payors (h/t Bronte Capital):

Private insurers and the courts are not generally alarmed by occasional accommodations for individual patients with documented financial limitations. However, insurance carriers have successfully challenged the routine waiver of copayment obligations in the courts on numerous occasions.

Courts dealing with challenges to discounts of copayment obligations have been concerned with two basic issues. First, a provider who discounts established fees for some patients but not others, without a valid distinction for the differing treatment, can be subject to claims of false billing by a party not receiving the discount or consideration, including claims by insurance carriers. Second, the routine waiver of patient copayment amounts can be viewed as breach of contract. Almost without exception, insurers impose a contractual duty on providers to make a reasonable effort to collect applicable copayment amounts from patients, and benefits are only available when the charge for the service submitted by the provider is the actual, and the usual, reasonable and customary charge (URC). The reasoning in these cases is that the uniform discounting or waiver of patients’ copayment portion of a provider’s fee evidences that the provider really only intends to collect that portion of the fee that is not discounted, making it improper to claim that the fee is the full undiscounted fee.

We spoke with several healthcare attorneys and reimbursement consultants. All agreed it would be surprising if commercial insurers would not find Zynex in breach of contract if made aware of the waivers.

We found numerous examples of case law. Aetna successfully argued a provider committed insurance fraud by waiving copayments and failing to disclose (Aetna Health, Inc. v. Carabasi Chiropractic, 2006). Aetna recently won a $37.4mn judgement against a provider group in part for routinely waiving copayments (Aetna Life Insurance Co. v. Bay Area Surgical Management LLC, 2016). Blue Cross successfully claimed providers violated contracts by failing to charge patients for coinsurances (Pennsylvania Chiropractic Association v. Blue Cross Blue Shield Association, 2011).

The financial implications are considerable. Insurance companies could find ZYXI in breach of contract, refuse to reimburse claims and attempt to recover past payments. We emailed Zynex for comment, and asked questions including what percentage of patients receive copay assistance, how much is spent on it and what if any disclosure is provided to insurers. Zynex has not responded. Analysts would do investors a service by asking such questions on the next call.

One former employee told us Zynex frequently uses the back brace to “bust deductibles”. According to her, salespeople are encouraged to promote brace prescriptions in conjunction with NexWave, since the $1,000+ brace reimbursement can instantly fill a deductible, allowing Zynex to pocket all reimbursement for NexWave and supplies for very little upfront cost.

Exhibit 8. Zynex shares several troubling characteristics with Philidor

There Will Not Be Blood: New Device Unlikely to Sell

In late February, Zynex announced FDA clearance of its CM-1500 “Blood Volume Monitor”. Sandgaard has promoted a TAM of $3bn (20 units in 5,000 hospitals at $30k). We think this is a wild exaggeration of the market and belies the actual technology and usefulness of the device. We believe the device will follow a path similar to that of every other device ZYXI has touted in the past and end up as a failure.

The CM-1500 has been in development since 2011. First filed under the 510(k) pathway in 2015, it took over four years to receive clearance from the FDA. We suspect one of the reasons it took so long was that FDA took issue with certain efficacy and marketing claims. Zynex was originally calling the CM-1500 a “Blood Volume Monitor” as shown on the webpage from 2018 but the current page refers to it as a “Cardiac Monitor”.

Note another significant change in language – the prior page stated, “indicate fluid balance or blood loss in the OR and potential internal bleeding in the Recovery Room”. The current page never mentions the words fluid or blood, instead focusing on cardiac monitoring. On the Q2 19 earnings call Sandgaard is asked to comment on FDA’s outstanding questions and he hints that claims and phrasing were issues:

“So, recently, we have submitted a response that should be aligned nearly word-for-word with their suggestions as to how we should phrase things, so with a bit of luck, the next response, they don’t have any further questions or suggestions to us, and else, we’ll just keep answering the questions.

We also note the CM-1500 was cleared by the Cardiovascular review panel and classified as a Plethysmograph, Impedance device (electrical impedance plethysmography is old technology – see this paper from 1950 discussing its usefulness). Compare this to Daxor (NYSE: DXR) which is marketing a blood volume monitor called the BVA-100, cleared by the FDA’s Hematology panel and classified as a Blood Volume Measuring device.

The CM-1500 combines several basic physiological measurements such as heart rate and skin temperature into a numerical index, changes in which are supposed to inform clinicians of blood loss. We spoke to a senior official at Daxor familiar with the CM-1500 as concerned investors were calling him the day it was cleared. Even though he noted Daxor’s device would not in theory directly compete with the CM-1500, he believed it to be redundant and was skeptical of its accuracy noting that tachycardia can indicate both hypo and hypervolemia.

Indeed the only study results we found on the CM-1500 show its lack of precision. The 2016 “study”, administered by ZYXI’s Director of Strategy and Business Development, consisted of eight volunteers whose index changes were recorded during a local blood draw Zynex hosted at its headquarters. Results were mixed at best as the index for two participants unexpectedly increased.

Judging by the limited information available, in our view the CM-1500 is best characterized as a cardiac output monitor (matching its name), which primarily uses bioelectric impedance analysis to measure fluid levels. The non-invasive cardiac output or hemodynamic monitor space is led by Edwards Lifesciences (NYSE: EW). Other manufacturers include Cardiodynamics, Deltex, Lidco and Retia Medical.

Experienced healthcare investors know that except in rare cases, commercialization is an uphill and costly effort. Consider Cheetah Medical whose Nicom hemodynamic monitoring system uses an advanced form of impedance analysis. Cheetah raised over $90mn, published seven peer-reviewed studies of its technology over six years, and still took five years to reach $4mn in revenue. Zynex has completed zero peer-reviewed studies and we will point it out again – has only spent an average of $330k on R&D since 2007. In this context, it seems absurd to even consider the CM-1500 a serious, viable product, especially considering that cost sensitive hospitals rather than obligated insurance companies would be the paying customers.

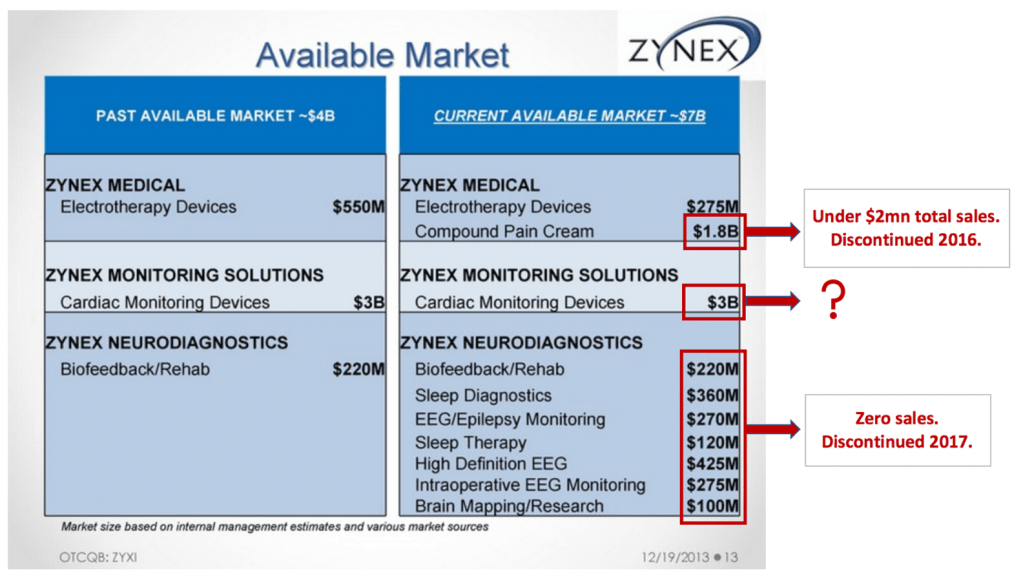

Investors should note that Zynex has repeatedly touted new products in the past, and all were unequivocal failures. These include a compound pain cream Zynex called a $1.8bn opportunity, and various products in it’s now closed NeuroDiagnostics segment (another $1.8bn TAM). Below is a slide from a 2013 investor presentation (our marks in red).

And then there are two products Sandgaard has highlighted during earnings calls for years. The NeuroMove, a stroke rehabilitation product Zynex claimed is a $200mn opportunity and has tried to sell since 2001, and the InWave cleared in 2012 for urinary incontinence (appears to be a NexWave reconfigured with a vaginal probe) with a supposed TAM of $5bn. Both have had negligible sales despite being on the market for years.

Exhibit 9. Zynex has touted other products in past – all have been failures

On May 14 Zynex teased “Something BIG is coming” on its social media accounts. The stock ran up 10% into the announcement on May 18, which turned out to be a catalog of products manufactured by other medical equipment companies. Any revenues from this business will be extremely low margin, as none of the equipment is reimbursable by insurance. We think it’s noteworthy that Zynex, which purports itself to be an “innovative medical technology company”, for its first new business effort in years chose dropshipping medical equipment for other manufacturers.

Several Insurers Respond To Our Concerns, Investigate ZYXI Claims

After we reported our findings to large commercial insurers late last year, several responded by examining Zynex claims including Aetna and Humana. We have also discussed our findings over the phone with several Blue Cross Blue Shield investigators in several states.

Aetna:

Humana:

Zynex reported Q1 20 gross margins of 78%, the first time quarterly margins fell below 80% in three years, citing “lower collections from certain commercial payors”. It’s possible that insurers, spurred by our reported concerns, are finding irregularities in ZYXI claims or issues with overall reimbursement policy.

We have since expanded our effort to alert insurers and relevant authorities, sending complaints to special investigation units of the largest plans in multiple states [samples]. And we have had direct communication with an investigator at the Department of Insurance of a large state which is investigating after an insurance company reported Zynex’s billings.

ZYXI bulls may paint this effort as simply an attempt to help a short position. But we are confident the market will reprice the stock lower once certain misconceptions about Zynex are better understood (more on this below), even without our reports to insurers. We firmly believe Zynex is a textbook case of corporate waste and abuse contributing to higher costs in our healthcare system.

Source of Mispricing: Analysts Confuse Zynex For A Medical Technology Company and Misunderstand TENS Market

At a stock price of $24, Zynex has an enterprise value of $830m, yet we believe the value of the business is zero. In our view the disconnect is rooted in the misperception that Zynex is a Medical Technology company and that innovation and superior execution has allowed it to succeed where others failed.

Zynex management has successfully shaped this narrative, at least to retail investors. Sandgaard maintains that larger competitors were shut down by the government (most recently on a sell-side call) but this is unsupported. In actuality, the two largest companies in the TENS sector – DJO Global (Empi) and RS Medical – essentially ceased business by the end of 2015 since it was no longer profitable. See this note to Empi customers and management’s press release announcing the exit. What’s more, both companies were unable to find a buyer for even part of the businesses.

“This healthcare environment has impacted our Empi business negatively despite our investments and best efforts to return that business to sustained profitability. As result, we have made the difficult decision to exit the Empi business…” – Empi management, 2015

Zynex shareholders are implicitly betting that every other operator in the sector was unable to make the model work and that potential acquirers of DJO and RS missed the value. Consider how implausible this idea is. After all, there isn’t much room for alpha in the non-patented, prescription TENS business. There may be some variation in negotiating contracts with payors, but prices and margins are largely set for all suppliers.

Zynex clearly is not Medtech – recall the minimal amounts spent on R&D, or that 80% of revenue is from distributed supplies, or that NexWave has been on sale since 2011, a product for which it has never held a patent. (“NexWave” is not even trademarked. See this USPTO suspension of application letter from 2012 and notice of abandonment in 2015.)

Or just look at its business model (Exhibit 1) and now its new catalog business. Zynex is a DME supplies distributor and it should be evaluated as such.

Yet the four sell-side analysts (B Riley FBR, H.C. Wainwright, Ladenburg and Northland) covering Zynex all classify it as Medical Technology and comp it to SMIDs actually engaged in innovation. Mischaracterizing Zynex as Medtech has allowed analysts and retail investors to view the 80% gross margins and lack of competition as fundamental positives rather than aberrations.

Part of problem is that until recently there has not been a publicly-traded pure DME distributor since 2013 (Rotech filed for bankruptcy). The DME industry underwent significant change beginning in the 2000s and leading up to the CBP in 2011, which forced margin compression on an industry full of inefficient and debt heavy companies, leaving it extremely fragmented among private suppliers. Traditional equity investors had little reason to look at the sector and as a result, investor awareness is limited. This is especially the case with the TENS sub-sector. To our knowledge, no notable public M&A has occurred in the space since 2005 so investors and analysts have not had a benchmark in over 15 years.

Sources: Empi [Pg. 42], Compex [Pg. 55], DJO Inc [Pg. 39], Apria [Pg. 32], Lincare [Pg. 24], DJO Global

This has contributed to retail shareholders and sell-side analysts misinterpreting industry dynamics including market size and risks, especially associated with reimbursement. FBR applies an 20x multiple to 2021 EBITDA and the DCFs of Ladenburg and HCW use discount rates of only 10 and 11%. In our view these analysts are not only underpricing reimbursement risk, but ignoring it almost completely (not a single analyst on the Q1 20 earnings call asked about the impact of Tricare’s coverage decision). The potential for competition is also underpriced – for instance HCW assumes competition does not enter until 2028 and Ladenburg applies a 6x multiple to 2022 revenues.

In our view, the sell-side is also wrong or has done minimal diligence on the CM-1500. Despite the inadequate data, Zynex’s unbroken history of failed products outside of NexWave and inexperience in cardiac monitoring, sell-side analysts have helped promote the CM-1500’s potential to retail shareholders, repeating management’s $3bn TAM and promises of commercialization. HCW is even modelling 2021 sales over $3mn at full MSRP.

So when Zynex was up-listed from OTC to the NASDAQ in early 2019, retail investors, attracted to the story of growth and limited competition, bid up the stock. Sell-side analysts helped by evaluating Zynex as a Medical Technology company, applying inappropriate multiples and downplaying risk. ZYXI shares then qualified for addition into the Russell 2000 index in June which forced buying by passive index funds. As sales headcount has grown, so have revenues, fueling another cycle of analyst price target increases feeding retail investor interest. And now add excitement of a new device with a supposed multi-billion dollar TAM. All has left ZYXI shares completely mispriced with an earnings multiple 80% above its closest comparable.

Valuation: Best Case Values Shares 80% Lower

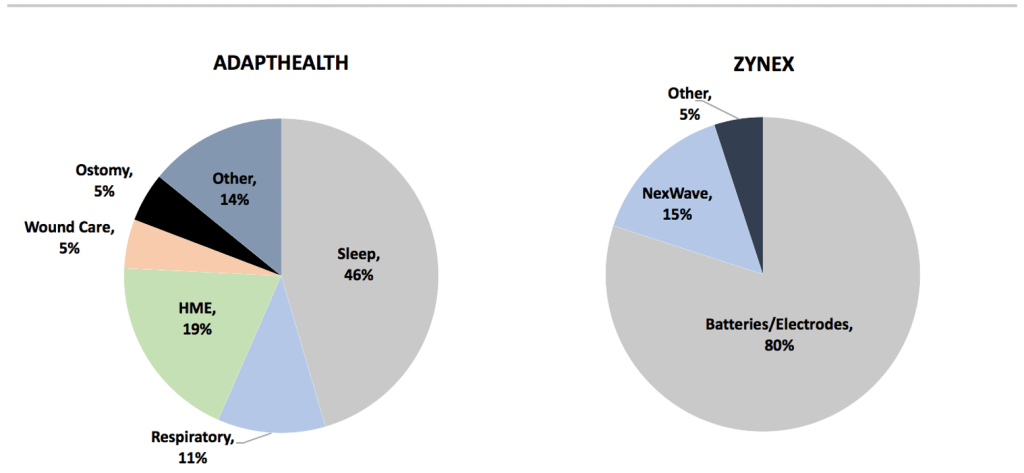

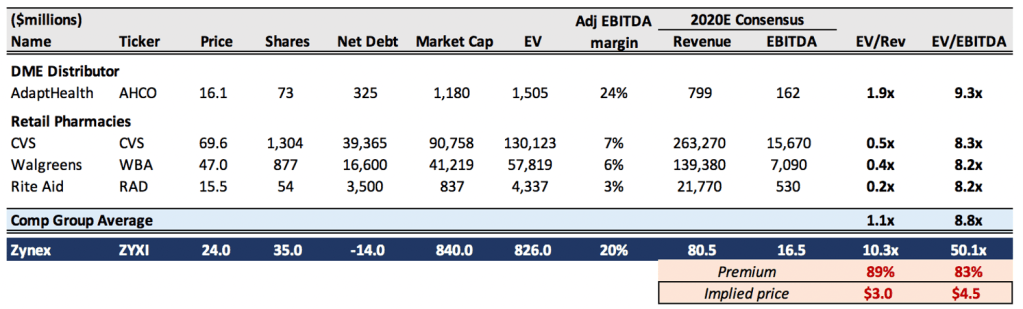

Finding an appropriate DME supplier comp for Zynex was only possible recently when AdaptHealth (NASDAQ: AHCO) went public late last year. AHCO distributes a broad set of home medical equipment (HME) across a variety of product categories including sleep apnea, supplemental oxygen, general HME and supplies. Started in 2012, AHCO’s strategy involves growing through acquisitions of smaller regional companies, and realizing cost efficiencies with a differentiated technology system that automates many critical parts of the DME business through e-prescribing, automated patient outreach and order intake.

In contrast to Zynex, AdaptHealth has a diversified product mix and gross margins that make sense for a legitimate distributor of DME (17% in 2019). And AHCO is a sophisticated business, with highly-regarded management – Chairman Richard Barasch is former CEO of Universal American and “one of the most prominent thought-leaders in the payor space” according to SVBLeerink.

AdaptHealth has equivalent adjusted EBITDA margins to Zynex, though it isn’t growing as fast. However, given that Zynex is operating in a constrained market (more on this below) and in our view entirely dependent on abusive and unsustainable billing, we don’t believe ZYXI deserves credit for this growth. As we stated previously – as revenues grow so do the risks.

Exhibit 10. Zynex revenues are highly concentrated

Where should ZYXI shares trade? If we are being kind, Zynex’s operating model is a cross between an HME supplier like AHCO (without any of AHCO’s technological and service value add) and a retail pharmacy, dispensing generic products it does not manufacture and processing reimbursements, profiting off of the difference between wholesale costs and insurance payments. In our bull case, Zynex trades with the average EV/EBITDA multiple of this comp group, valuing shares at $4.5 or 80% lower. This is supported by a DCF using optimistic assumptions including margin expansion from current levels and a steep increase in revenue per sales rep relative to history.

Exhibit 11. Zynex very expensive to comps with legitimate, sustainable business models

Exhibit 12. DCF supports EV/EBITDA multiple valuation

However, the names in our comp group don’t carry the same regulatory and reimbursement risks that Zynex does. In our base case, these risks materialize and reimbursement rates are reset to “normal” levels.

To approximate normalized revenues and gross margin for Zynex, we use average reimbursement fees realized between 2013 and 2016. This period incorporates two significant industry developments: 1) Medicare dropping TENS coverage for lower back pain, a major revenue driver for TENS units and 2) the first two years of the CBP adjustment (we exclude 2017, the final year of the adjustment since revenue per order nonsensically increased 250%).

Applied to 2019 results, this would’ve cut average supplies revenue per order from $832 to $300 and total revenues by nearly 50%, dropping gross margins to 62%.

Exhibit 13. Zynex completely dependent on supplies reimbursement

Zynex swings to steep losses here, even though 62% margin is only slightly below the average of the Medical Technology names mentioned previously. Even if Zynex reduced SG&A to 75% of revenues, its average between 2009 and 2016, the company would still operate at a significant loss. These figures make clear why DJO/Empi and RS Medical left the business during this period.

What would the stock be worth in this scenario? NexWave itself isn’t worth anything significant since much cheaper and similarly unpatented alternatives are available at retail for a fraction of NexWave’s total cost. Its actual value for Zynex has been as a vehicle for battery and electrode resales reimbursable by commercial payors, which we have shown would turn unprofitable under a normal, rational reimbursement structure. In our base case, the value of the business is zero and shares are only worth the $14mn cash on the balance sheet, or $0.50/share.

Current Stock Price Removed From Reality

The current price of $24 is pricing in nonsensical outcomes. Besides misjudging risk, investors are severely overestimating the size of the TENS market, in our view.

We estimate US TAM for TENS devices and supplies at $250mn based on the following:

- We estimate Empi accounted for 50% of DJO’s recovery sciences 2011 revenue of $343mn [Pg. 49]

- Zynex estimated DJO/Empi had 57% market share in 2011 [Slide 17]

- Empi 2015 annual run rate revenue was $140mn [Pg. 66]

- Zynex 2014 investor relations estimated TAM at $275mn (before Competitive Bidding) [Slide 12]

- Independent research firm Grand View Research estimates market below $200mn

- Empi, RS Medical and Zynex combined revenues were ~$270mn in the years before CBP (so our estimate is likely on the high side)

If we assume Zynex quickly captures 100% market share in 5 years (40% CAGR), with revenue per rep increasing to $625k, and doesn’t lose share to competition until 2031, operating in perpetuity we still get valuations 45-60% lower.

More simply, at a stock price of $24, ZYXI’s market cap of $840mn is over 3-times TAM.

Exhibit 14. Assuming Zynex captures 100% market share, DCF values stock 70-80% lower

(Note: Implied revenue per sales rep of $625k in this scenario is also detached from history. Going back to 2010, median revenue per rep is $184k, with a range of $64k to $259k.)

Risks Increasing: Avoid Shares of Zynex

Rarely have we come across a stock so simple to value yet so mispriced. Zynex isn’t a biotech developing new drugs with variable pricing or a technology company attempting to create new markets. Zynex distributes a handful of basic items, most of which can be found on the shelves of a local Walmart, and one of which makes up half of total revenue. Pricing should be stable and we know the size of the market.

Yet Zynex shares are priced beyond perfection due to analyst and retail investor confusion and complacency. Risks such as reimbursement cuts are being ignored. Same with the potential for payor or regulator intervention (see Tricare’s recent decision to no longer cover TENS for lower-back pain). Red flags like a lack of competition are rationalized and viewed as positives. Sell-side valuations require inputs completely divorced from reality.

Eventually the market will adequately price the risks in ZYXI or insurers and regulators will force it. Because Zynex has been collecting such egregious amounts and margins on two generic items, and using abusive billing tactics such as regularly waiving copays, the probability that regulators or insurance companies investigate has been rising. Last year Zynex resold $35mn in batteries and electrodes at ~90% gross margins. Consensus supplies revenues for 2020 and 2021 are $60mn and $95mn. Indeed we already see evidence of insurers beginning to reexamine reimbursement policy for Zynex products, with gross margins narrowing last quarter and many commercial and state insurance investigators now aware of our concerns.

Owning Zynex is a bet that insurance abuses or inefficiencies can persist indefinitely. Perhaps equally concerning for shareholders is that even if regulators or insurers never intervene, and Zynex achieves full market share and competition doesn’t show up for a decade – fair value in such a fantasy is still at least 70% lower.