- We identify UnitedHealthcare as Zynex’s largest payor and estimate it was paying ~7x more per order relative to other commercial insurers, artificially sustaining the weak underlying business

- We find UHC recently changed its TENS coverage policy which may lower its payments to Zynex by 80% – equivalent to 40-100% of 2021 EBITDA

- Reimbursement pressure is evident in accounts receivable which ballooned in Q3, outpacing revenue growth. Days sales outstanding rose to highest level in over 4 years.

- Zynex could be forced to modify its revenue recognition and write-down accounts receivable to adjust for the new policy

- The most surprising aspect of the policy change is that it took so long – UHC recently attempted to recoup $5m from a smaller TENS company billing less abusively than Zynex

- In a best-case scenario, Zynex shifts focus to a small subset of payors offering viable reimbursement levels. We think this means Zynex shrinks by at least 50%

- The fundamental stress comes at a time when Zynex’s CEO is forced to continually tap his 43% stake to meet substantial personal cashflow needs.

December 10, 2021 — The bull case for Zynex Medical (NASDAQ: ZYXI, “the Company”) is based on the belief that insurers would continue to pay for its overpriced TENS units and generic electrodes because waste and abuse is ingrained in the US healthcare system. “Everyone is overbilling.” The idea proved more resilient than we expected. We thought payors, particularly commercial insurers, would have a better handle on waste and abuse, especially involving products as unproven and primitive as transcutaneous electrical nerve stimulation (TENS) units which are technologically on par with transistor radios. Skeptics like us believed Zynex would eventually collapse, the only question was when. We think the end is in sight.

We have identified UnitedHealthcare (UHC), the benefits division of parent UnitedHealth Group (NYSE: UNH), as Zynex’s largest payor and primary target of abuse. We estimate UHC was paying Zynex ~7x more per order relative to other commercial insurers. We find the insurer recently changed its coverage policy for TENS, which will cut its reimbursement to Zynex by approximately 80%. Consequently, Zynex will lose high margin orders that we estimate account for 40-100% of 2021 EBITDA.

Zynex was already showing signs of nearing the limit of what insurers would tolerate, backing away from aggressive hiring guidance and reducing staff beginning in Q1 2021. Now after being cut-off by a large source of earnings, Zynex will be left with few options, none of them good for shareholders. Any meaningful order growth will likely come at the expense of margins as the average reimbursement per order turns loss making. Zynex could focus on pockets of high reimbursement, but this means becoming a much smaller company.

If the stock weren’t about to be crushed fundamentally, it will nonetheless be pressured by CEO Thomas Sandgaard who must sell stock to meet his significant cashflow needs. In 2020 Sandgaard, whose wealth is tied up in his 43% stake in the company, bought a 3rd-tier English football club that was burning through £1m per month. Sandgaard most recently tapped his shares in August ahead of the league’s transfer deadline. His Premier League aspirations will require copious funding underwritten by unwitting Zynex shareholders.

With the fundamentals and technicals aligned, we think now is a great time to be short Zynex.

Temporary Payor Vulnerabilities Enabled Zynex Turnaround

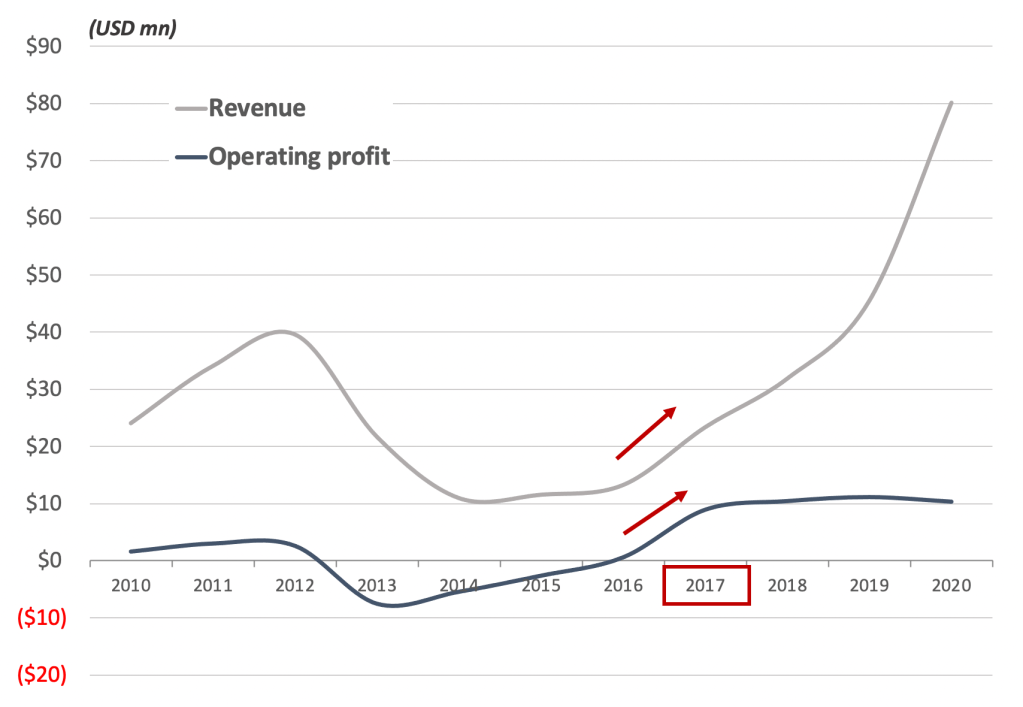

It’s important to remember that before Zynex began its rise from an OTC penny stock in 2017, its underlying business was so weak that it was on the edge of bankruptcy under the weight of a $3m line of credit [Pg. 9]. At the end of 2016, Zynex couldn’t even pay the premiums on its liability, property and auto insurance [Pg. 25].

Then out of nowhere the business improved. Zynex was offering the same unpatented, archaic TENS unit yet revenue per order nearly tripled from 2016 to 2017 – suddenly the business was profitable.

The improvement was never well explained. After the Centers for Medicare and Medicaid Services (CMS) instituted competitive bidding in 2015, slashing Medicare reimbursements for TENS, public reimbursement policy has remained weak. Sandgaard claims the upswing was the result of increased market share after the exit of two large competitors. He’s likely referring to an increased share of the workers’ compensation market, which pays TENS claims at levels far above average. We think Sandgaard was also referring to patients insured by UnitedHealthcare (UHC) which we believe has been Zynex’s largest single source of high margin revenue since the turnaround in 2017.

We think Zynex’s unexpected “hockey stick” growth in 2017 was due to 1) an increased share of workers’ compensation patients and, 2) the exploitation of reimbursement policy weakness at UnitedHealthcare.

The workers’ compensation market might be the last area where the TENS business is feasible, due to an arcane and poorly controlled reimbursement and coding framework. While our checks with workers’ comp investigators indicate the industry is tamping down on Zynex’s abusive billing tactics, our focus here is on UHC and its new policy which we think will render the business unviable in its current form.

UnitedHealthcare Closes Reimbursement Policy Weakness

UHC did not have an official TENS coverage policy until recently. Instead, the insurer negotiated reimbursement rates and allowable supplies with manufacturers ad hoc. Sometime in 2017 it appears Zynex was able to negotiate a nonsensical quantity of electrodes per patient – 64 pairs per month, a figure we confirmed with UHC employees and patient claim forms.

Exhibit 1 – Supplies as percentage of revenue jumps in 2017

Sandgaard hinted at this during the Q4 2017 call in response to a question about the increase in supplies revenue (bold emphasis added):

“And then we have also seen that there are some insurance plans that actually allow for more supplies than we have, we’ve been able to negotiate in the past. That’s very much a negotiating item and by being able to negotiate well and make sure that the patients get the supplies that they actually need.”

An increased share of workers’ comp patients and the new opportunity to dump massive quantities of electrodes on UHC patients led to major shifts in the company’s financials: supplies rose to 79% of revenue in 2017 after averaging 39% between 2009 and 2016 (Zynex breaks out revenue for devices and supplies). Revenue per order increased 160% Y/Y in 2017 – while device revenue per order decreased. Operating margins, negative to slightly better than flat in the years prior, jumped to 38%. UHC and workers’ comp propped up an otherwise limp, money losing business.

Exhibit 2 – Zynex suddenly profitable in 2017

Zynex exploited UHC’s reimbursement vulnerability through 2020, and concurrently grew its salesforce by roughly 5x which naturally led to order and revenue growth. Retail investors saw a rapidly expanding, profitable company with no significant competition. Sandgaard meanwhile was making reckless projections – at a time when the average sale rep was generating just above $200K in annual sales, he touted plans of an 800-person salesforce generating $800m in sales, utterly ludicrous figures for the TENS market. Zynex stock went from $0.10 in 2016 to nearly $30 in 2020.

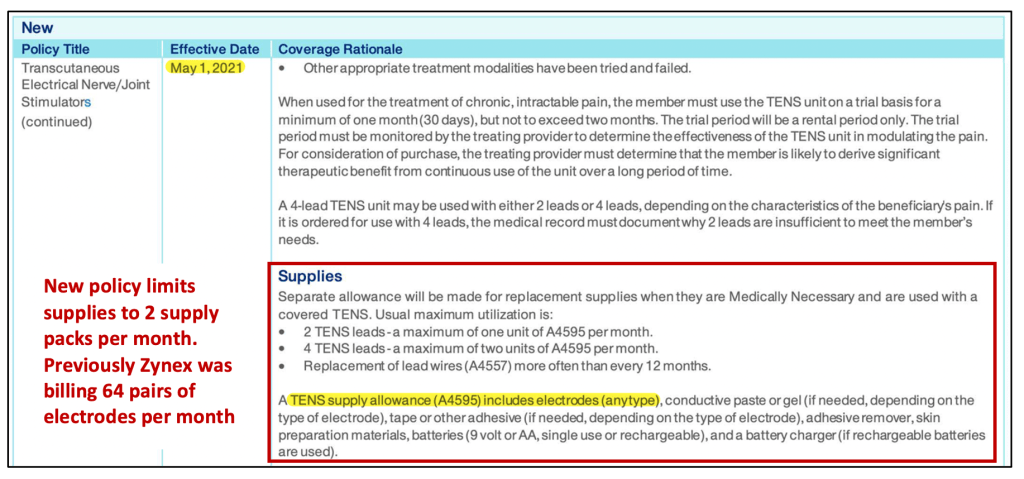

Unfortunately for Zynex, UHC eventually woke up. In February 2021, UHC announced a new coverage policy for TENS effective May 2021 which specifies the quantity of supplies allowed per prescription. The policy stipulates “usual maximum utilization” is one or two units of a monthly supply pack which includes electrodes, batteries, and conductive gel.

Exhibit 3 – UHC’s new coverage policy severely limits TENS supplies

Instead of being reimbursed for 64 pairs of electrodes per patient every month, Zynex is limited to at most two units of a supply pack.

Processed Claims Show Policy Effect and Damage to Zynex

Our prior work on Zynex, which included interviewing former senior employees and reviewing the reimbursement policies of numerous commercial insurers, led us to suspect UHC was reimbursing Zynex abnormally. This was confirmed when a UHC insured patient sent us Zynex claims information.

Zynex’s standard monthly claim was for lead wires, 2 batteries, and 64 pairs of electrodes. For the electrodes, Zynex was billing an “MSRP rate” of $49.50 per pair for a total of $3,168 per month. Over 10 months, the patient received 640 pairs of electrodes.

Exhibit 4 – 640 pairs of electrodes received by UHC patient over 10 months

When UHC approved the claims, it allowed $0 for the batteries, $14 for lead wires and almost $520 for the electrodes (UHC pays Zynex the total allowable minus the patient’s copay). Including $250 for the device, Zynex was collecting nearly $5,600 for patients with UHC commercial health plans over the average 10-month prescription.

Exhibit 5 – UHC patient claim before policy change: 64 pairs of electrodes covered

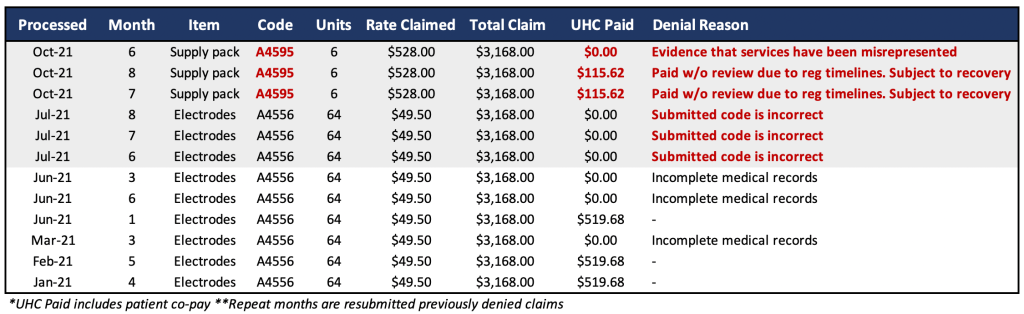

After two months, concerned about their potential co-pay obligations the patient reported the excessive quantities to UHC which flagged the patient’s file and led to denials of 4 of 8 submitted claims. Relevant for Zynex investors is the change in denial reasons.

Exhibit 6 – UHC policy change prohibits abusive coding by Zynex

As shown in Exhibit 6, UHC had been denying claims due to “incomplete medical records”, meaning Zynex did not provide documentation to support the medical necessity of 64 pairs of electrodes (note UHC would have paid these claims had the patient not complained). Two months after the new TENS policy went into effect in May 2021, UHC began denying the claims for improper coding as Zynex was still billing with the “unbundled” electrodes HCPCS code A4556 rather than one or two units of the supply pack using the “bundled” code A4595. The use of “unbundled” codes is a common method of fraud and abuse in healthcare billing.

Two claims were approved for $115.62 without being reviewed to meet regulatory compliance timelines. Although both are subject to review and recovery, the $115.62 for 6 units of A4595 ($19.27 each) is the best case for Zynex going forward – an 80% reduction in the rare case UHC pays a claim without review. But the likely outcome is that both claims will be denied upon review and Zynex will be left with $38.54 for two units of A4595.

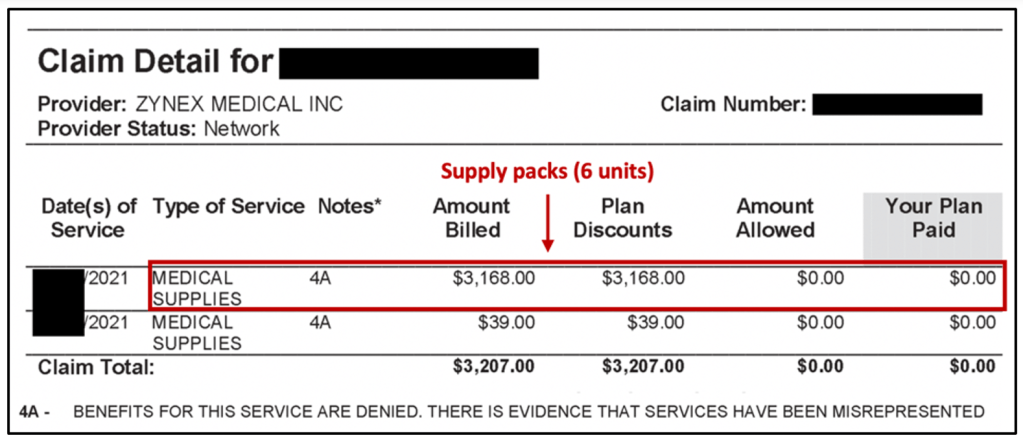

The most recent claim was denied due to “evidence that services have been misrepresented”. Here, UHC reviewed the claim and determined that 6 units of the supply pack, instead of 1 or 2, was a misrepresentation of provided services.

Exhibit 7 – UHC patient claim post new policy: Electrodes not covered

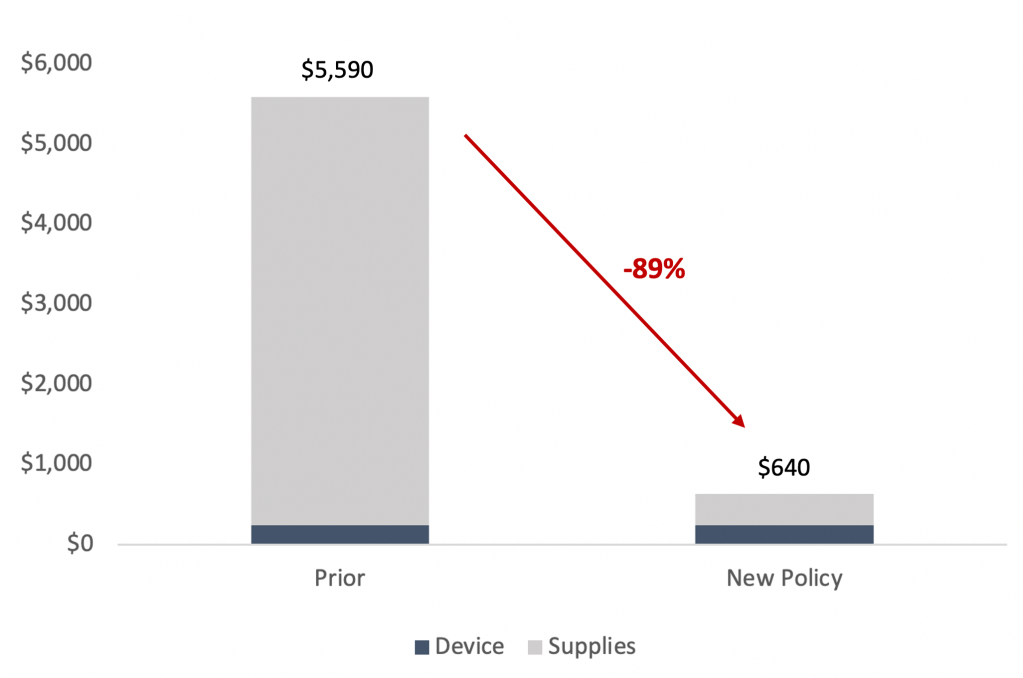

Using Zynex’s stated average reimbursement duration per device of 10 months, we estimate that UHC’s new policy could reduce its payments to Zynex by ~90%.

Exhibit 8 – Severe reduction in UHC reimbursement per NexWave order

The Ugly Math: Revenue Loss Equivalent to 40-110% 2021E EBITDA

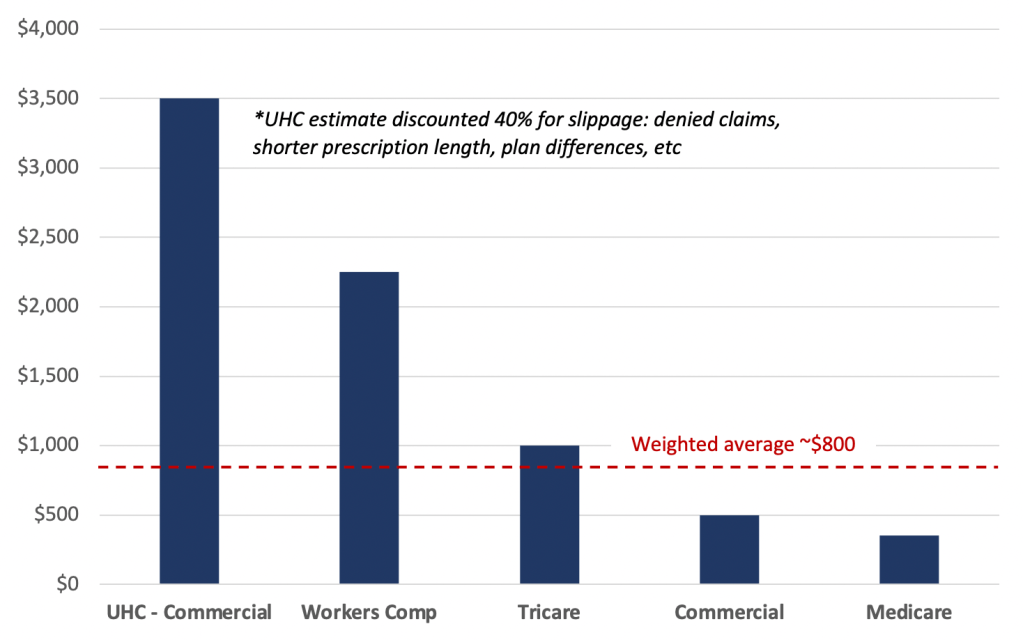

Not only will Zynex lose revenue – it’s margins will be materially impacted. We estimate the average reimbursement per UHC order was ~5x the ex-UHC average, skewing the overall average higher and making a big contribution to margins. Using Medicare’s fee schedule, our estimate of commercial insurance reimbursement and our work on UHC, we estimate reimbursement by payor and worker’s comp orders which we think lie somewhere in the middle:

Exhibit 9 – Estimated average reimbursement per order by payor

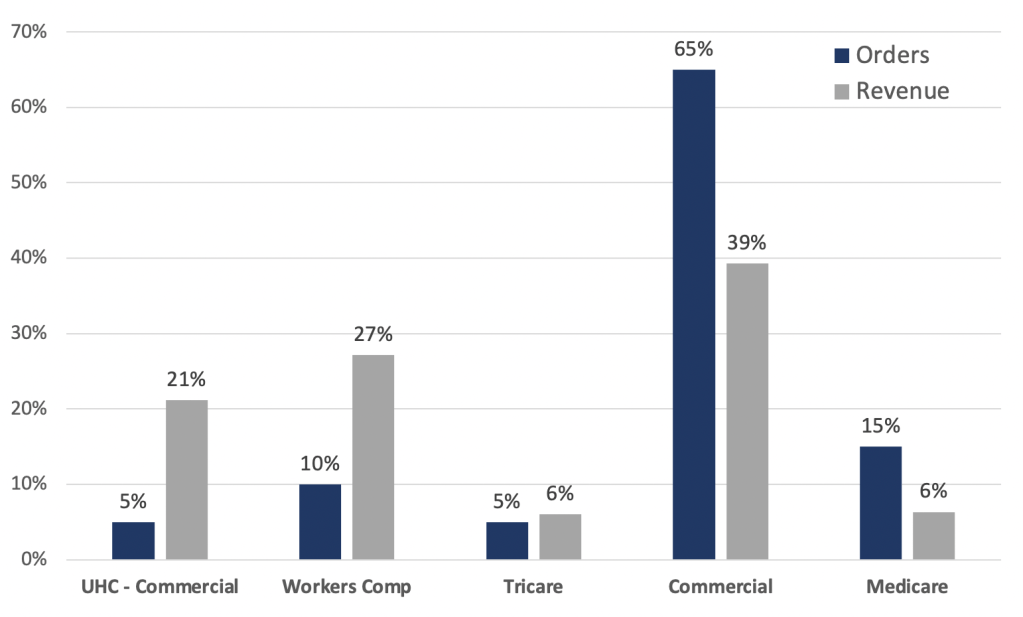

Based on discussions with CFO Dan Moorhead, who told us that UHC is Zynex’s largest source of revenue, and the company’s disclosures which note that two payors make up 37% of accounts receivable [Pg. 16], we think UHC may account for only 2-5% of orders, but 10-25% of revenue. As such, the UHC orders are highly capital efficient – Zynex won’t be able to simply reduce expenses to offset the lost revenue.

Exhibit 10 – We think UHC is a small part of orders but larger part of revenue

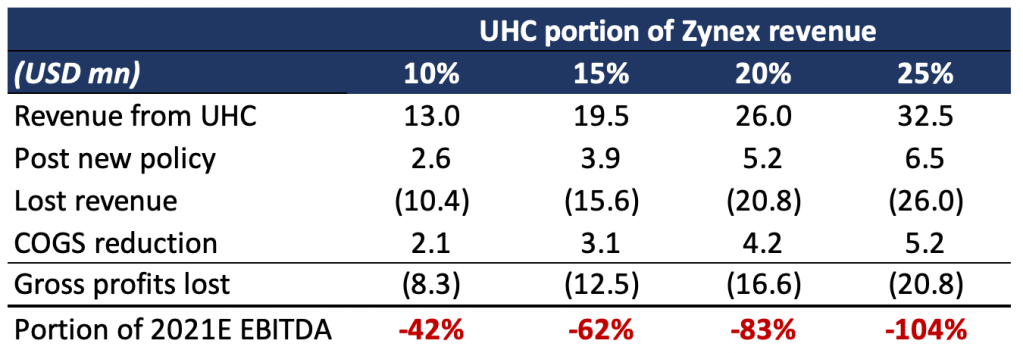

Exhibit 11 – Equivalent loss estimate for 2021E earnings

If we assume the new policy will cut UHC reimbursement per order by 80%, depending on how much UHC makes up of current revenue, it’s possible Zynex will be left unprofitable going forward (Exhibit 11).

Early effects of the new policy are evident in Q3 accounts receivable which rose by $5.9m Q/Q vs an increase in revenue of $3.8m. Days sales outstanding (DSO) increased sequentially by 17% to over 60 days, its highest level in over four years.

We think the large receivables and DSO increases are at least partly due to lower collections from UHC, and that Zynex hasn’t yet changed its revenue assumptions to account for the policy. As a result, most of the receivables attributed to UHC in Q3 and on may not be collectable. If so, Zynex will eventually have to write-down accounts receivable and restate earnings. Precedent occurred in 2009 when Zynex underestimated payor discounts forcing it to restate receivables and net income lower for the year prior by ~50% and 95% respectively [Pg. 41].

While Zynex may not be accounting for the policy in its financials, we think it’s reducing its salesforce and adjusting investor communications in response to the change at UHC and for what we think is a workers’ compensation industry stiffening its reimbursement protocol.

Consider the narrative shift – coming into 2021 Zynex had over 500 sales reps, the story was aggressive growth into untapped market share and over 600 reps by end of the year. At Q1, Zynex reduced its salesforce to under 500, but still expected 600 by year-end. By Q2, rep headcount was reduced to 450 and year-end guidance was lowered to 550 (Sandgaard attributed the reduction to a “competitive job market” and a “focus on productivity”). By the end of Q3 the salesforce shrank to 430 and Zynex no longer planned to make any net additions before year-end.

Also noteworthy was the abnormal amount of discussion on the Q3 call devoted to the so-called Blood Volume Monitor, a product that received FDA clearance in February 2020 yet has generated zero sales. The increased messaging around this failed device is an attempt to mitigate the reimbursement cliff by inserting “product diversification” into the story, in our view.

It Could Get Worse: UHC May Attempt to Recoup Millions in Overpayments from Zynex

UHC’s change of policy was overdue. It’s surprising that it took so long since UHC acted against a Zynex competitor for billing in the same manner, although less egregiously. We became aware of the situation through a lawsuit filed by the competitor.

Tampa-based EMSI, a private TENS manufacturer, is Zynex’s largest competitor and the only other TENS company in UHC’s network. In September 2018, after conducting an audit of EMSI claims, UHC demanded EMSI stop billing for individual pairs of electrodes and to instead use the bundled supply pack code. In addition, UHC reduced the allowable quantity of electrodes per patient from 8 pairs to 4 pairs per month (2 supply packs).

Exhibit 12 – Excerpt of EMSI vs UHC lawsuit

In October 2018, only one month after UHC demanded the coding change, EMSI “succumbed to the pressure” and began billing only two units of the supply pack. EMSI has billed with this code ever since, according to an EMSI representative we spoke with.

In July 2019, UHC demanded EMSI repay $5m for almost four years of paid claims with the unbundled electrode code (A4556, the same code Zynex has been using) or UHC would “offset” future EMSI claims against this amount. Last year EMSI filed a lawsuit against UHC seeking an injunction to block the $5m repayment demand (the case went to arbitration).

Exhibit 13 – Excerpt of EMSI vs UHC lawsuit

Several elements of the EMSI case are relevant to Zynex shareholders:

- UHC will attempt to recoup payments from a TENS manufacturer billing improperly

- Not only can UHC demand immediate repayment, it can also offset future claims against the amount owed

- EMSI was only billing for 8 pairs of electrodes per month per patient. Zynex was until recently (or may still be) billing for 8x this amount!

- If UHC were to conduct a similar audit of Zynex claims, any overpayment demand is likely a multiple of $5m considering the quantity difference and that Zynex is larger than EMSI

We don’t know why UHC initially only acted against EMSI and not Zynex even though it was sending patients 8x more electrodes. Even if Zynex and EMSI negotiated different contracts with UHC, why allow such wasteful supply quantities to persist? It doesn’t make sense. However, after following Zynex since 2019, we’ve learned that insurers move slowly, especially large ones like UHC. Whatever the reason, the EMSI case shows that once it identifies abusive billing, UHC will pursue the culprits and attempt to recoup overpayments. So, the penalty for Zynex could go beyond reduced future reimbursements and include liability for past profits.

The risk of a repayment demand makes the recent announcement of a 10% cash and stock dividend seem ill-advised. Rather than conserving cash or making the effort to move past a teetering business reliant on abusive medical billing by investing in new technology or M&A, Zynex is spending cash on a reckless attempt to, “counteract the short interest”, as CFO Moorhead told several investors during one-on-one calls. Moorhead also said Zynex wanted to reward shareholders – the largest of course being its own CEO.

Technical Pressure: CEO Forced to Sell Shares to Meet Personal Cashflow Needs

The fundamental blow couldn’t have come at a worse time for Zynex whose CEO is forced to sell shares to meet his significant personal cash flow needs.

Sandgaard bought the English football club Charlton Athletic in September 2020. To fund the purchase, he sold 1.25m Zynex shares two months prior. Charlton was nearly bankrupt or on the edge of “administration” before Sandgaard took over. At the time, the club required £1m in cash per month to operate and although the financial strain is currently lower with spectators once again allowed to attend games – operating a lower-tier team (Charlton is in League One, the third tier of the English Football League) is an unprofitable and expensive venture.

Exhibit 14 – Zynex CEO Thomas Sandgaard

This is especially so for Sandgaard who has advertised ambitious goals for Charlton, hoping to take the club to the Premier League within 5 years. Serious EFL fans scoff (the British press has referred to Sandgaard as a cross between Bon Jovi and the fictional character David Brent from the mockumentary The Office), but what’s important is that Sandgaard’s dreams will require a lot of money and most of his wealth is tied to his 43% stake in Zynex.

We’ve already seen Sandgaard’s Charlton endeavors leak into Zynex when he sold $2.7m worth of shares on August 6 as the league’s trade deadline was approaching. Also remarkable is that Zynex stock was supported by an active share buyback program at the time. Whether or not these discretionary, open market sales were appropriate is controversial, but Zynex stock is 20% lower since. Another trade window closes on January 31 and, if the curiously timed $0.10 dividend or $1.5m he is effectively paying himself on January 21 is insufficient, we expect Sandgaard to tap his shares again.

Growth Topped Out, Reimbursement Risk in Focus: 75%+ Downside

Consensus revenue and EBITDA estimates for 2022 are $181m (+38% Y/Y) and $38m (+65% Y/Y), respectively – the street is modeling growth, yet Zynex has stopped adding sales reps and likely lost its largest source of revenue. We believe both numbers will be materially cut next year when Zynex is forced to lower guidance and/or disclose repayment demands. We think the EBITDA figure could be cut by 40% or more based on our view that UHC accounts for a large part of Zynex’s profitability (Exhibit 11). To stem losses Zynex will be forced to cut staff significantly and reduce non-profitable orders from Medicare and most commercial health insurers. Private competitor EMSI, roughly half the size of Zynex in terms of employees and revenue, is a model of where Zynex potentially goes from here.

Where should a structurally unprofitable, one product, no (meaningful) pipeline, growth challenged company trade?

Exhibit 15 – Consensus too high in 2022

For illustrative purposes, if we assume UHC accounts for 15% of Zynex revenue, an 80% reduction in UHC reimbursement, and that ex-UHC 2021 revenue of $110m grows 10% next year (fair to optimistic considering the company is no longer making net additions to its salesforce), a 0.5-1.0x multiple on $126m revenue equates to ~$1.60-$3.30 per share (post stock dividend share count of 38.5m). We think the multiple range is appropriate considering our stalled growth forecast, remaining reimbursement risk, and possibility of UHC overpayment clawbacks and accounts receivable write-downs.