- We uncover evidence that UnitedHealthcare will remove Zynex from its network effective February 15, a seemingly material event undisclosed to investors

- Zynex will lose its largest payor and only national commercial network, a critical relationship which represented high margin revenue worth 50-100% of EBITDA

- UHC’s aggressive decision signals major billing abuses and a high probability it pursues Zynex for overpayments (potential liability of ~$40m), introducing profound downside for the stock

- Considering the damage to cash flow, profitability, and impact on 2022 earnings which will likely fall short of consensus estimates – we believe the stock is uninvestible

Disclosure: We are short ZYXI. Please see full disclaimer at bottom of report.

February 17, 2022 – We’ve long suspected Zynex was reliant on billing UnitedHealthcare (NYSE: UNH) for excessive quantities of electrodes. When UHC recently introduced a new TENS coverage policy it appeared the insurer finally detected the impropriety but might continue to pay Zynex claims if at reduced rates. However, it appears UHC has taken decisive action to put an end to Zynex’s abusive tactics. See below:

Exhibit 1 – UnitedHealthcare January 11 letter

This letter, sent to us by a patient concerned about Zynex’s billing, indicates UHC is removing Zynex from its network effective February 15. The decision – which Zynex has not disclosed to investors – would end a ten-year relationship with its largest payor and only national commercial network contract.

We estimate the expulsion will immediately cost Zynex nearly all its UHC business which for several years has represented 15-25% of high margin revenue equal to 50-100% of EBITDA. UHC revenue was critical to Zynex as it offset negative margin orders from most other public and commercial insurers. We find it hard to see how Zynex grows from here. The more relevant debate at this point is the degree to which Zynex shrinks.

Exhibit 2 – 2022E NMR vs Consensus

Moreover, the decision signals a high likelihood UHC pursues recovery of past payments which total an estimated $45m to $80m since 2017. We highlighted this risk in our last report, presenting the case of a competitor whom UHC found was using the same improper tactics as Zynex – although far less abusively. In that case UHC attempted to recover nearly four years of overpaid claims and used the threat of network removal as leverage, but never dropped the competitor from its network. That Zynex was dropped indicates a relatively offensive posture at UHC, and we expect the insurer to make repayment demands.

Network Expulsion Cuts Off Zynex’s Largest and Most Important Source of Revenue

We called Zynex customer service representatives on two occasions in late January as patients inquiring about insurance coverage. The representatives confirmed the network loss and noted the company was unaware of the cause.

On January 27 we asked UHC Consumer Affairs to comment on its network contract with Zynex. The UHC representative confirmed Zynex’s removal adding that it was UHC’s decision to terminate the relationship:

NMR: “Can UnitedHealthcare comment on its network agreement with Zynex Medical?“

UHC Consumer Affairs: “UnitedHealthcare made the decision to opt out of the contract. Due to confidentiality concerns, we cannot disclose more information at this time.”

The loss of network status will effectively close UHC as a significant source of revenue. We previously estimated UHC’s new TENS coverage policy could cut its reimbursement to Zynex by 80%. With the loss of network status, the damage will be even worse due to limited coverage and patients reluctant to bear out-of-pocket costs. As a result, we think Zynex’s UHC revenues will be cut by at least 90%.

UnitedHealthcare Business Enabled Zynex Profitability and Growth

The prescription TENS business is based on the razor-razorblade model: place TENS units and collect recurring higher-margin revenue from monthly supplies. But due to Medicare reimbursement cuts, the model is barely profitable if at all under standard reimbursement levels, especially at large scale.

In our last report we used processed claim forms to show Zynex has been sending UHC commercial patients 64 pairs of electrodes per month, an absurd number exceeding any reasonable usage assumption (Medicare and most commercial insurers only allow 4 to 8 pairs per month if they cover TENS units). Making matters worse, Zynex was using an improper billing code.

Exhibit 3 – 640 pairs of electrodes received by UHC patient over 10 months

We think Zynex began flooding UHC patients with electrodes in 2017. That year revenue per prescription increased nearly three-fold and margins turned positive (despite no change in public TENS reimbursement policy), pushing Zynex stock over $1 for the first time since 2009. As a captive source of demand for excessive electrodes, UHC enabled Zynex’s previously floundering razor-razorblade model.

Exhibit 4 – Revenue growth and profitability begins after Zynex floods UHC patients in 2017

We estimate UHC was paying ~7x more per prescription relative to other commercial insurers.

Zynex’s reliance on UHC is magnified by the fact that it’s the company’s only national commercial network agreement. After February 15, Zynex will only have network agreements with BlueCross BlueShield in six states: Hawaii, Louisiana, Minnesota, Pennsylvania, Colorado, and West Virginia. Based on our research and conversations with Zynex employees, BCBS TENS policies are near industry standards.

UHC Likely to Pursue Zynex for Past Reimbursements

Equally concerning is that the decision signals a high probability that UHC will pursue recovery of past payments. The insurer did so against EMSI, a competitor less than half the size of Zynex.

After a 2018 audit, UHC alleged EMSI was submitting claims for excessive electrodes using the same improper billing code that Zynex has been using. UHC demanded repayment of $5m out of a total of $16m paid. Interestingly, UHC used the threat of network removal as leverage, but never dropped EMSI.

Exhibit 5 – Excerpt of EMSI vs UHC lawsuit

The case went to arbitration and in February 2022 EMSI was awarded $1.7m in attorney’s fees and arbitration costs. While the outcome was positive for EMSI, we still believe the case is relevant and cautionary for Zynex since UHC pursued EMSI for what appears to be similar billing methods. Moreover, UHC never removed EMSI from its network hinting that Zynex billing was worse.

In gauging potential repayment liability, consider that Zynex was billing for 8x the number of electrodes (64) per commercial patient per month. Multiplying $5m by 8x produces a potential UHC recovery demand of $40m. Alternatively, UHC’s demand of $5m was 30% of total payments. A proportional demand from UHC (an estimated $45m to $80m of Zynex revenue since 2017) at Zynex equates to $14m to $24m. For reference, we estimate Zynex’s current cash balance is approximately $20m, accounting for the recent acquisition and dividend.

We also expect UHC to refuse to pay outstanding payables recorded by Zynex which are ~25% of accounts receivable or $6m. Zynex encountered a similar issue in 2009 when management underestimated payor discounts requiring it to write down accounts receivable and restate revenue and net income lower for the year prior by approximately 25% and 95% [Pg. 41].

Zynex is Uninvestible

Zynex stock is extremely vulnerable here. While it screens “cheap”, consensus 2022 estimates of 30% and 40% revenue and EBITDA growth respectively, are based on incomplete information.

Since the network loss is effective February 15, we expect 2021 results to come in largely in-line with guidance. UHC’s loss will be felt beginning in Q1 2022 and if Zynex is fully transparent, we expect full year guidance to come in significantly below consensus (Exhibit 2).

We assume Zynex achieves a 2022 order total based on 95% of the Q4 2021 run-rate (second highest quarter ever), and that revenue per order will decline to $800 vs $1100 in Q4 and $850 for the full year 2021. We think margins could be cut in half relative to 2021 based on our estimate that UHC was a huge contributor to margins. Our annual revenue and EBITDA estimates of $120m and $12m are 31% and 66% below street consensus respectively. We believe our estimates are optimistic/conservative and err to the upside.

Considering the potential effects of the network loss on the viability of Zynex’s business, we believe the stock will be significantly re-rated. The lost UHC revenue will have a disproportionate effect on margins, forcing the company to shrink considerably, in our view. Moreover, the potential liability for past payments introduces extreme downside scenarios and existential questions.

Appendix: Recent Acquisition Utilized Toxic Financing

Recent announcements hint at the anticipated damage of UHC’s new TENS coverage policy. The sales force shrank from over 500 at the beginning of the 2021 to 430 as of Q3. Management issued press releases announcing a patent application and enrollment in a clinical trial for a zero-revenue product approved two years ago.

Zynex also announced the acquisition of Kestrel Labs, a Colorado-based developer of patient monitoring devices. Kestrel, a small company with three employees on LinkedIn, hopes to submit its two devices for FDA clearance in 2023 with marketing potentially beginning in 2024.

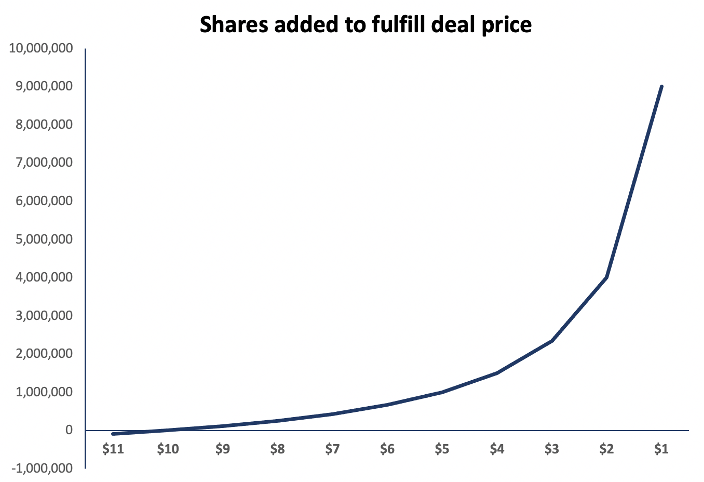

Kestrel was acquired with $16m in cash and $15m in stock. $10m of the stock portion, priced at approximately $10.12 post-split, will be held in escrow and repriced to the 30-day volume weighted average one year from the closing date. Thus, as the stock moves lower an increasing number of shares are required to fulfill the deal price. The 30% move lower in Zynex shares since the announcement has already added 360k shares. If Zynex is as impaired as we believe, the Kestrel equity financing exacerbates downside.

Exhibit 6 – Kestrel acquired with toxic-priced equity

Disclaimer

As of the publication date of this report, Night Market Research (NMR) and Connected Persons (as defined hereunder), along with or through its members, partners, affiliates, employees, clients, and investors, and/or their clients and investors have a short position in the securities covered herein (and options, swaps, and other derivatives related to these securities), and therefore will realize significant gains in the event that the price of any stock covered herein declines. NMR and NMR Connected Persons are likely to continue to transact in the securities covered herein for an indefinite period after an initial report, and such position(s) may be long, short, or neutral at any time hereafter regardless of their initial position(s) and views as stated in NMR’s research.

Use of NMR’s research is at your own risk. In no event shall NMR or any NMR Connected Person be liable for any direct or indirect trading losses caused by any information in this report. You further agree to do your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities covered herein.

This is not an offer to sell or a solicitation of an offer to buy any security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. NMR is not registered as an investment advisor in the United States, nor does NMR have similar registration in any other jurisdiction. To the best of NMR ‘s ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources NMR believes to be accurate and reliable, and who are not insiders or connected persons of the issuer covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind – whether express or implied. NMR makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and NMR does not undertake to update or supplement this report or any of the information contained herein.

NMR Connected Person is defined as: NMR and its affiliates and related parties, including, but not limited to any principals, officers, directors, employees, members, clients, investors, and agents. One or more NMR Connected Persons may have provided NMR with publicly available information that NMR has included in this report, following NMR’s independent due diligence.